|

市场调查报告书

商品编码

1959641

工业通讯市场机会、成长要素、产业趋势分析及2026年至2035年预测。Industrial Communication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

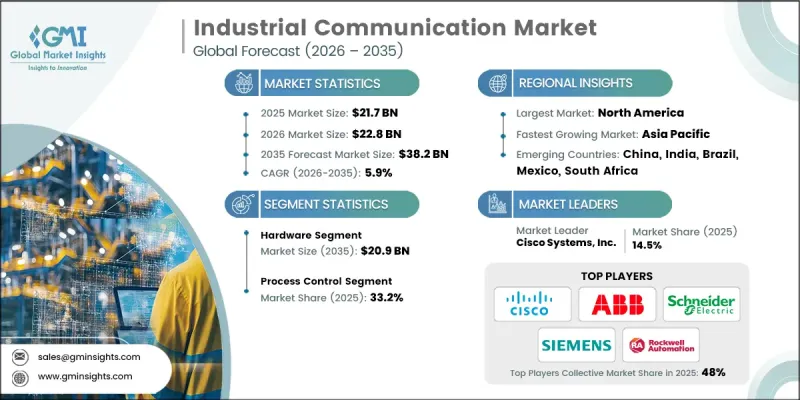

2025 年全球工业通讯市场价值 217 亿美元,预计到 2035 年将达到 382 亿美元,年复合成长率为 5.9%。

机器人、人工智慧数位双胞胎等先进技术的普及推动了这个市场的发展。这些技术需要高速、可靠且可互通的通讯网路才能有效运作。随着工业基础设施连接性的增强,网路安全、网路可用性和确定性效能的重要性显着提升。互联设备、云端系统和边缘运算的增加,使得网路威胁、资料外洩和营运中断的风险日益加剧。这促使製造商投资建置具有加密、认证、冗余和网路分段等安全通讯网络,以确保不间断且安全的运作。工业乙太网凭藉其更高的频宽和对资料密集应用的即时控制能力,正在广泛取代传统的现场汇流排系统。同时,工业Wi-Fi和专用5G网路等无线通讯技术因其柔软性、更低的布线成本以及在复杂生产环境中的快速部署能力而备受关注,使其成为现代自适应製造系统不可或缺的一部分。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 217亿美元 |

| 预测金额 | 382亿美元 |

| 复合年增长率 | 5.9% |

预计到2035年,硬体市场规模将达到209亿美元,这主要得益于市场对能够在高温、振动和电磁干扰等严苛工业环境下可靠运作的坚固耐用组件的需求。边缘设备和嵌入式连接模组的整合正在加速,从而实现低延迟即时数据处理和高效的网路管理。

预计到2025年,製程控制领域将占据33.2%的市场。工业通讯网路与分散式控制系统和可程式逻辑控制器(PLC)的整合度日益提高,从而提升了自动化操作的精度、扩充性和同步性。高速、确定性网路能够实现即时过程监控,优化整体运作效率。

预计到2025年,北美工业通讯市占率将达到31.2%。这一区域成长主要得益于製造业和能源产业的大规模位转型倡议,以及工业乙太网和工业物联网(IIoT)技术的快速普及。北美製造商优先考虑自动化、专用无线网路和安全的网路架构,以支援稳健且有效率的工业营运。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 工业物联网(IIoT)生态系的扩展

- 互联自主工业设备的成长

- 先进技术(机器人、人工智慧、数位双胞胎)的集成

- 工业设施对无缝IT-OT整合的需求

- 工业网路安全和网路弹性日益受到关注

- 产业潜在风险与挑战

- 实施和整合的初始成本较高

- 跨多种通讯协定的互通性挑战

- 市场机会

- 私有工业5G和时间敏感网络(TSN)的兴起

- 中小製造工厂工业通讯的扩展

- 促进因素

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域分布比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2022-2025 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 硬体

- 工业开关

- 网关和通讯协定转换器

- 路由器和无线网路基地台

- 控制器和连接器

- 通讯介面和转换器

- 电源

- 其他部件

- 软体

- 通讯协定堆迭和韧体

- 网路管理与监控工具

- 工业IoT整合软体

- 设定和诊断软体

- 服务

- 系统整合与咨询

- 网路部署与试运行

- 维护和支援服务

第六章 市场估算与预测:依通讯协定,2022-2035年

- 现场汇流排通讯协定

- PROFIBUS

- MODBUS RTU

- CAN

- DeviceNet

- CANopen

- 其他现场汇流排

- 工业乙太网通讯协定

- PROFINET

- 乙太网路/IP

- EtherCAT

- MODBUS-TCP

- POWERLINK

- SERCOS III

- CC-Link IE

- 时间敏感网路(TSN)

- 其他工业乙太网

- 无线工业通讯协定

- 工业无线区域网路(Wi-Fi 6/6E)

- 5G/专用LTE

- Bluetooth Industrial

- ISA100.11a

- WirelessHART

- Zigbee

- 其他无线设备

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 过程控制

- 机器对机器(M2M)通信

- 远端监测和诊断

- 预测性维护和状态监测

- 安全系统

- 其他的

第八章 市场估算与预测:依最终用途产业划分,2022-2035年

- 製造部门

- 车

- 航太/国防

- 食品/饮料

- 药品和医疗设备

- 电子和半导体

- 金属和采矿

- 机械设备

- 纺织服装

- 纸浆、纸张和包装

- 其他的

- 工艺及公用设施部

- 石油和天然气

- 能源和发电

- 用水和污水管理

- 可再生能源

- 其他的

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 主要企业

- Cisco Systems

- Siemens

- ABB

- Huawei

- 按地区分類的主要企业

- 北美洲

- Rockwell Automation

- Emerson Electric

- Belden

- 欧洲

- Schneider Electric

- Phoenix Contact

- HMS Networks

- 亚太地区

- Omron

- Mitsubishi Electric

- Yokogawa Electric

- 北美洲

- 特殊玩家/干扰者

- Advantech

- Moxa

The Global Industrial Communication Market was valued at USD 21.7 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 38.2 billion by 2035.

The market is driven by the widespread adoption of advanced technologies, including robotics, artificial intelligence, and digital twins, which require fast, reliable, and interoperable communication networks to operate efficiently. As industrial infrastructures become more connected, the importance of cybersecurity, network availability, and deterministic performance has grown significantly. The proliferation of connected devices, cloud systems, and edge computing increases exposure to cyber threats, data breaches, and operational downtime. This has led manufacturers to invest in secure communication networks equipped with encryption, authentication, redundancy, and network segmentation to ensure uninterrupted and protected operations. Industrial Ethernet has largely replaced traditional fieldbus systems due to its higher bandwidth, enabling real-time control for data-intensive applications. Simultaneously, wireless communication technologies, such as industrial Wi-Fi and private 5G networks, are gaining traction for their flexibility, reduced cabling costs, and faster deployment in complex production environments, making them essential for modern, adaptive manufacturing systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.7 Billion |

| Forecast Value | $38.2 Billion |

| CAGR | 5.9% |

The hardware segment is expected to reach USD 20.9 billion by 2035, driven by the demand for ruggedized components capable of operating reliably under extreme industrial conditions, including high temperatures, vibration, and electromagnetic interference. Integration of edge devices and embedded connectivity modules is accelerating, enabling low-latency, real-time data processing and efficient network management.

The process control segment held 33.2% share in 2025. Industrial communication networks are increasingly integrated with distributed control systems and programmable logic controllers, enhancing precision, scalability, and synchronization in automated operations. High-speed, deterministic networks allow real-time process monitoring and control, optimizing overall operational efficiency.

North America Industrial Communication Market accounted for a 31.2% share in 2025. The region's growth is fueled by large-scale digital transformation initiatives in manufacturing and energy sectors, coupled with the rapid adoption of industrial Ethernet and IIoT technologies. North American manufacturers are prioritizing automation, private wireless networks, and secure network architectures, supporting resilient and efficient industrial operations.

Key players in the Global Industrial Communication Market include Rockwell Automation, Siemens, Cisco Systems, ABB, Omron, Schneider Electric, and Huawei. Companies are strengthening their Industrial Communication Market position by investing heavily in R&D to develop high-speed, secure, and interoperable communication solutions. They are forming strategic partnerships with technology providers, industrial manufacturers, and automation integrators to expand adoption and deployment. Firms are focusing on edge connectivity, private 5G, and IIoT-enabled devices to support digital transformation initiatives across industries. Additionally, players are offering scalable, modular hardware and software systems to cater to small and large-scale industrial operations while providing services for cybersecurity, predictive maintenance, and real-time analytics. Market expansion into emerging regions, flexible pricing models, and comprehensive customer support strategies further reinforce their presence and enhance competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Communication protocol trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of industrial internet of things (IIoT) ecosystems

- 3.2.1.2 Growth in connected and autonomous industrial equipment

- 3.2.1.3 Integration of advanced technologies (robotics, AI, digital twins)

- 3.2.1.4 Demand for seamless IT-OT convergence across industrial facilities

- 3.2.1.5 Growing emphasis on industrial cybersecurity and network resilience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial deployment and integration costs

- 3.2.2.2 Interoperability challenges across multiple communication protocols

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of private industrial 5G and time-sensitive networking (TSN)

- 3.2.3.2 Expansion of industrial communication in small and mid-sized manufacturing facilities

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Industrial switches

- 5.2.2 Gateways & protocol converters

- 5.2.3 Routers & wireless access points

- 5.2.4 Controllers & connectors

- 5.2.5 Communication interfaces & converters

- 5.2.6 Power supply devices

- 5.2.7 Other components

- 5.3 Software

- 5.3.1 Protocol stacks & firmware

- 5.3.2 Network management & monitoring tools

- 5.3.3 Industrial iot integration software

- 5.3.4 Configuration & diagnostic software

- 5.4 Services

- 5.4.1 System integration & consulting

- 5.4.2 Network deployment & commissioning

- 5.4.3 Maintenance & support services

Chapter 6 Market Estimates and Forecast, By Communication Protocol, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Fieldbus protocols

- 6.2.1 PROFIBUS

- 6.2.2 MODBUS RTU

- 6.2.3 CAN

- 6.2.4 DeviceNet

- 6.2.5 CANopen

- 6.2.6 Other Fieldbus

- 6.3 Industrial ethernet protocols

- 6.3.1 PROFINET

- 6.3.2 EtherNet/IP

- 6.3.3 EtherCAT

- 6.3.4 MODBUS-TCP

- 6.3.5 POWERLINK

- 6.3.6 SERCOS III

- 6.3.7 CC-Link IE

- 6.3.8 Time-sensitive networking (TSN)

- 6.3.9 Other industrial ethernet

- 6.4 Wireless Industrial Protocols

- 6.4.1 Industrial WLAN (Wi-Fi 6/6E)

- 6.4.2 5G / Private LTE

- 6.4.3 Bluetooth Industrial

- 6.4.4 ISA100.11a

- 6.4.5 WirelessHART

- 6.4.6 Zigbee

- 6.4.7 Other Wireless

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Process control

- 7.3 Machine-to-machine (M2M) communication

- 7.4 Remote monitoring & diagnostics

- 7.5 Predictive maintenance & condition monitoring

- 7.6 Safety & security systems

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Manufacturing sectors

- 8.2.1 Automotive

- 8.2.2 Aerospace & defense

- 8.2.3 Food & beverage

- 8.2.4 Pharmaceutical & medical devices

- 8.2.5 Electronics & semiconductor

- 8.2.6 Metals & mining

- 8.2.7 Machinery & equipment

- 8.2.8 Textile & apparel

- 8.2.9 Pulp, paper & packaging

- 8.2.10 Others

- 8.3 Process & utilities sectors

- 8.3.1 Oil & gas

- 8.3.2 Energy & power generation

- 8.3.3 Water & wastewater management

- 8.3.4 Renewable energy

- 8.3.5 Others

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Cisco Systems

- 10.1.2 Siemens

- 10.1.3 ABB

- 10.1.4 Huawei

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Rockwell Automation

- 10.2.1.2 Emerson Electric

- 10.2.1.3 Belden

- 10.2.2 Europe

- 10.2.2.1 Schneider Electric

- 10.2.2.2 Phoenix Contact

- 10.2.2.3 HMS Networks

- 10.2.3 APAC

- 10.2.3.1 Omron

- 10.2.3.2 Mitsubishi Electric

- 10.2.3.3 Yokogawa Electric

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Advantech

- 10.3.2 Moxa

工业通讯市场:按通讯方式、组件和最终用户划分 - 2026-2032年全球市场预测工业通讯闸道市场:按组件、通讯协定、连接方式、部署模式、应用和产业划分-2026-2032年全球市场预测

工业通讯市场:按通讯方式、组件和最终用户划分 - 2026-2032年全球市场预测工业通讯闸道市场:按组件、通讯协定、连接方式、部署模式、应用和产业划分-2026-2032年全球市场预测 工业通讯市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型、最终用户及解决方案划分

工业通讯市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型、最终用户及解决方案划分 全球工业通讯市场规模、份额、趋势和成长分析报告(2026-2034)

全球工业通讯市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球工业通讯市场报告

2026年全球工业通讯市场报告 工业通讯市场按组件、通讯协定、最终用户和地区划分

工业通讯市场按组件、通讯协定、最终用户和地区划分 工业通讯市场-全球产业规模、份额、趋势、机会和预测。按产品、通讯协定、最终用户、地区和竞争格局划分,2021-2031年预测

工业通讯市场-全球产业规模、份额、趋势、机会和预测。按产品、通讯协定、最终用户、地区和竞争格局划分,2021-2031年预测 工业通讯市场规模、份额和成长分析(按产品、通讯协定、垂直产业和地区划分)-2026年至2033年产业预测

工业通讯市场规模、份额和成长分析(按产品、通讯协定、垂直产业和地区划分)-2026年至2033年产业预测 工业通讯市场(按产品、通讯协定、垂直产业和地区划分)- 2030 年预测

工业通讯市场(按产品、通讯协定、垂直产业和地区划分)- 2030 年预测 全球石油与天然气区块链市场

全球石油与天然气区块链市场