|

市场调查报告书

商品编码

1959664

医疗旅游市场机会、成长要素、产业趋势分析及2026年至2035年预测Medical Tourism Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

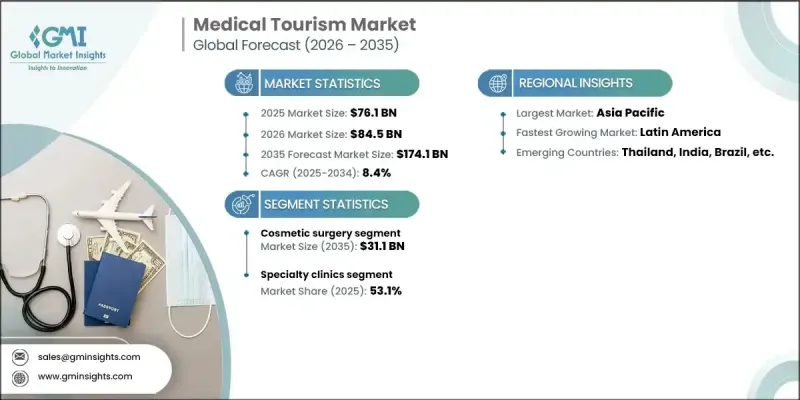

2025 年全球医疗旅游市场价值 761 亿美元,预计到 2035 年将达到 1,741 亿美元,年复合成长率为 8.4%。

推动这一增长的因素有很多,包括慢性病患病率上升、开发中国家医疗成本降低以及外科手术程序对国际标准的遵守程度提高。数位化术前术后护理、目的地专属的专业知识以及综合服务模式正在降低患者的出行风险并加速其普及。已开发国家高昂的医疗成本、高额的自付费用以及庞大的医疗支出,持续促使病患寻求出国就医。远距远端医疗的整合加强了当地专家与家庭医生之间的协作,同时减少了患者多次就诊的需求。后疫情时代远端医疗的成熟使其角色从便利转变为必需,预计未来将增加对远端监测和安全数据共用的投资。医疗旅游涵盖预防保健、择期手术、复杂手术和远距康復,能够以更低的成本和更短的等待时间,为患者提供高品质的医疗保健服务。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 761亿美元 |

| 预测金额 | 1741亿美元 |

| 复合年增长率 | 8.4% |

预计到2025年,整形外科产业将占据17.1%的市场。在植髮、塑形和脸部整形等项目的推动下,全球对整形手术的需求仍然强劲。透明的价格、较短的恢復时间和高性价比的方案对患者,尤其是自费患者,极具吸引力。社群媒体的影响以及人们对自身外观日益增长的关注,持续推动着整形手术的普及,使其成为医疗旅游的重要组成部分。

预计到2025年,专科诊所将占据53.1%的市场。这些诊所提供特定治疗领域的专业技术,例如生育、心臟病、肿瘤、牙科、整形外科和美容医学。由于其个人化的照护、较短的等待时间和经济实惠的治疗方案,专科诊所深受医疗旅客的青睐。许多诊所正在投资最尖端科技、微创手术和国际培训的专家。他们还透过为国际患者提供高效的流程来改善整体就医体验,包括配备专门的协调员来管理后勤、预约和后续事宜。

预计到2025年,亚太地区医疗旅游市场规模将达337亿美元,在病患数量和专科医疗服务方面均位居世界前列。印度、泰国、新加坡、马来西亚和韩国等国家拥有完善的医院网路、多语言医护人员以及在心臟病学、整形外科、肿瘤学和美容医学等领域的区域特色专科。公共和私人机构对数位医疗和智慧旅游基础设施的投资正在提升病患体验,而利用远端医疗医疗的治疗前后照护计画则进一步提高了医疗服务的可近性。医疗机构认证和健康服务的整合确保了该地区对寻求价格合理、高品质医疗服务的国际患者保持极高的吸引力。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 发展中国家医疗保健成本低廉

- 外科手术程序越来越符合国际标准。

- 慢性病发生率呈上升趋势

- 产业潜在风险与挑战

- 某些医疗程序的等待时间过长

- 与患者后续观察和术后併发症相关的挑战

- 机会

- 远端医疗

- 个人化治疗方案

- 美容手术和择期手术的成长

- 促进因素

- 成长潜力分析

- 监管环境

- 科技与创新趋势

- 当前技术趋势

- 人工智慧翻译工具

- 数位健康平台

- 电子健康记录(EMR)的整合

- 新兴技术

- 基于区块链的健康资料安全

- AR/VR在医疗旅游中的应用

- 当前技术趋势

- 目前医疗保险覆盖状况

- 消费者洞察

- 按地区分類的医院数量

- 各国具体趋势与倡议

- 患者和游客人口统计数据

- 投资环境

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章 竞争情势

- 介绍

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估计与预测:依应用领域划分,2022-2035年

- 整形手术

- 植髮

- 隆乳手术

- 其他美容手术

- 心血管外科

- 整形外科手术

- 全膝关节关节重建

- 全髋关节置换术

- 脊椎手术

- 肩关节关节重建

- 踝置换术

- 其他整形外科手术

- 肿瘤治疗

- 外科手术

- 放射治疗

- 化疗

- 其他治疗方法

- 牙科手术

- 人工植牙

- 正畸

- 美容牙科治疗

- 牙科修补

- 其他牙科服务

- 减重手术

- 不孕症治疗

- 其他用途

第六章 市场估算与预测:依最终用途划分,2022-2035年

- 专科诊所

- 医院

- 其他用途

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 西班牙

- 波兰

- 土耳其

- 匈牙利

- 捷克共和国

- 亚太地区

- 中国

- 日本

- 印度

- 泰国

- 韩国

- 新加坡

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 哥伦比亚

- 哥斯大黎加

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

第八章:公司简介

- Anadolu Medical Center

- Apollo Hospitals Group

- Asklepios Kliniken GmbH &Co. KGaA

- Bumrungrad International Hospital

- Clemenceau Medical Center

- Cleveland Clinic

- Fortis Healthcare Limited

- Gleneagles Hospital

- Johns Hopkins Hospital

- Karolinska University Hospital

- KPJ Healthcare Berhad

- Mahkota Medical Centre

- Makati Medical Center

- MANIPAL HEALTH ENTERPRISES PVT LTD

- Max Healthcare

- Mayo Clinic

- Mount Elizabeth Hospitals

- Narayana Health

- Proton Therapy Center

- Raffles Medical Group

- Samitivej Hospital

- Shouldice Hospital

- St. Luke's Medical Center

- Vera Smile

- Vera Clinic

The Global Medical Tourism Market was valued at USD 76.1 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 174.1 billion by 2035.

The growth is driven by multiple factors, including rising prevalence of chronic diseases, lower treatment costs in developing nations, and increasing compliance with international standards for surgical procedures. Digital pre- and post-treatment care, destination specialization, and bundled service models are making travel for patients less risky, accelerating adoption. High healthcare costs, larger deductibles, and significant out-of-pocket expenses in developed economies continue to push patients to seek care abroad. Telemedicine integration is reducing the need for multiple physical visits while improving continuity between destination specialists and home-based physicians. The post-COVID maturity of telehealth has shifted it from convenience to necessity, with further investments in remote monitoring and secure data sharing expected. Medical tourism spans preventive treatments, elective surgeries, complex procedures, and remote rehabilitation, providing patients with high-quality care at lower costs and reduced wait times.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $76.1 Billion |

| Forecast Value | $174.1 Billion |

| CAGR | 8.4% |

In 2025, the cosmetic surgery segment held a 17.1% share. Global demand for cosmetic procedures remains strong, fueled by procedures such as hair restoration, body contouring, and facial enhancements. Patients are drawn to destinations offering transparent pricing, shorter recovery times, and high perceived value, particularly among self-paying clients. Social media influence and growing awareness of personal appearance continue to drive the popularity of cosmetic surgery, making it a critical component of medical tourism.

The specialty clinics segment accounted for 53.1% share in 2025. These clinics provide focused expertise across therapeutic areas such as fertility, cardiology, oncology, dentistry, orthopedics, and aesthetics. Specialty clinics appeal to medical tourists due to personalized care, shorter wait times, and cost-effective treatment options. Many clinics invest in state-of-the-art technology, minimally invasive procedures, and internationally trained specialists. They offer streamlined processes for international patients, including dedicated coordinators to manage logistics, appointments, and follow-ups, enhancing the overall patient experience.

Asia Pacific Medical Tourism Market reached USD 33.7 billion in 2025, leading in both volume and specialized offerings. Countries in the region, including India, Thailand, Singapore, Malaysia, and South Korea, offer extensive hospital networks, multilingual staff, and destination-specific expertise spanning cardiac, orthopedic, oncology, and aesthetic procedures. Public-private investment in digital health and smart tourism infrastructure has strengthened patient experiences, while telehealth-enabled pre- and post-treatment care programs further enhance accessibility. Accreditation of facilities and integration of wellness services continue to make the region highly attractive for international patients seeking high-quality care at lower costs.

Prominent players in the Global Medical Tourism Market include Bumrungrad International Hospital, Cleveland Clinic, Max Healthcare, St. Luke's Medical Center, Vera Clinic, Fortis Healthcare Limited, Asklepios Kliniken GmbH & Co. KGaA, Raffles Medical Group, Karolinska University Hospital, Apollo Hospitals Group, MANIPAL HEALTH ENTERPRISES PVT LTD, Johns Hopkins Hospital, Mount Elizabeth Hospitals, Mahkota Medical Centre, Shouldice Hospital, Proton Therapy Center, Makati Medical Center, Gleneagles Hospital, Clemenceau Medical Center, and Anadolu Medical Center. Key strategies adopted by companies in the medical tourism market focus on enhancing patient experience, expanding global reach, and maintaining competitive advantages. Providers invest heavily in cutting-edge technology, telemedicine solutions, and digital care platforms to streamline pre- and post-treatment processes. Strategic partnerships with travel agencies, insurance companies, and international facilitators allow for bundled offerings and smoother logistics. Clinics emphasize personalized care, multilingual staff, and international accreditation to build trust. Marketing campaigns highlight affordability, quality, and reduced waiting times, while continuous staff training ensures adherence to global healthcare standards. Expanding specialty services and wellness programs further strengthen market positioning and foster long-term patient loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Low cost of medical treatment in developing countries

- 3.2.1.2 Growing compliance towards international standards for surgical procedures

- 3.2.1.3 Increasing prevalence of chronic diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long wait time for certain medical procedures

- 3.2.2.2 Issue with patient follow-up and post-surgery complications

- 3.2.3 Opportunities

- 3.2.3.1 Rise of telemedicine

- 3.2.3.2 Personalized treatment packages

- 3.2.3.3 Growth in cosmetic and elective surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.1.1 AI-powered translation tools

- 3.5.1.2 Digital wellness platforms

- 3.5.1.3 Electronic medical records (EMR) integration

- 3.5.2 Emerging technologies

- 3.5.2.1 Blockchain-based health data security

- 3.5.2.2 AR/VR for medical tourism

- 3.5.1 Current technological trends

- 3.6 Medical coverage scenario

- 3.7 Consumer insights

- 3.8 Number of hospitals by region

- 3.9 Developments and initiatives by country

- 3.10 Demographics of patients/tourists

- 3.11 Investment landscape

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cosmetic surgery

- 5.2.1 Hair transplant

- 5.2.2 Breast augmentation

- 5.2.3 Other cosmetic surgeries

- 5.3 Cardiovascular surgery

- 5.4 Orthopedic surgery

- 5.4.1 Knee replacement

- 5.4.2 Hip replacement

- 5.4.3 Spinal surgeries

- 5.4.4 Shoulder replacement

- 5.4.5 Ankle replacement

- 5.4.6 Other orthopedic surgeries

- 5.5 Oncology treatment

- 5.5.1 Surgery

- 5.5.2 Radiation therapy

- 5.5.3 Chemotherapy

- 5.5.4 Other therapies

- 5.6 Dental surgery

- 5.6.1 Dental implants

- 5.6.2 Orthodontics

- 5.6.3 Dental cosmetics

- 5.6.4 Dental prosthetics

- 5.6.5 Other dental services

- 5.7 Bariatric surgery

- 5.8 Fertility treatment

- 5.9 Other applications

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Specialty clinics

- 6.3 Hospitals

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Spain

- 7.3.4 Poland

- 7.3.5 Turkey

- 7.3.6 Hungary

- 7.3.7 Czech Republic

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Thailand

- 7.4.5 South Korea

- 7.4.6 Singapore

- 7.4.7 Malaysia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Columbia

- 7.5.4 Costa Rica

- 7.6 MEA

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 Egypt

Chapter 8 Company Profiles

- 8.1 Anadolu Medical Center

- 8.2 Apollo Hospitals Group

- 8.3 Asklepios Kliniken GmbH & Co. KGaA

- 8.4 Bumrungrad International Hospital

- 8.5 Clemenceau Medical Center

- 8.6 Cleveland Clinic

- 8.7 Fortis Healthcare Limited

- 8.8 Gleneagles Hospital

- 8.9 Johns Hopkins Hospital

- 8.10 Karolinska University Hospital

- 8.11 KPJ Healthcare Berhad

- 8.12 Mahkota Medical Centre

- 8.13 Makati Medical Center

- 8.14 MANIPAL HEALTH ENTERPRISES PVT LTD

- 8.15 Max Healthcare

- 8.16 Mayo Clinic

- 8.17 Mount Elizabeth Hospitals

- 8.18 Narayana Health

- 8.19 Proton Therapy Center

- 8.20 Raffles Medical Group

- 8.21 Samitivej Hospital

- 8.22 Shouldice Hospital

- 8.23 St. Luke's Medical Center

- 8.24 Vera Smile

- 8.25 Vera Clinic

全球医疗旅游市场规模、份额、趋势和成长分析报告(2026-2034)

全球医疗旅游市场规模、份额、趋势和成长分析报告(2026-2034) 医疗旅游市场规模、份额、趋势和预测:按治疗类型和地区划分,2026-2034 年

医疗旅游市场规模、份额、趋势和预测:按治疗类型和地区划分,2026-2034 年 全球医疗旅游市场:按治疗类型、服务提供者和地区划分-市场动态、市场规模、机会和预测(2026-2035 年)

全球医疗旅游市场:按治疗类型、服务提供者和地区划分-市场动态、市场规模、机会和预测(2026-2035 年) 医疗旅游服务市场:依治疗类型、服务类型、设施类型、套装类型、性别和年龄组别划分-2026年至2032年全球预测医疗旅游市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2025年至2034年的预测医疗旅游市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032)

医疗旅游服务市场:依治疗类型、服务类型、设施类型、套装类型、性别和年龄组别划分-2026年至2032年全球预测医疗旅游市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2025年至2034年的预测医疗旅游市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032) 医疗旅游市场:全球产业分析、规模、份额、成长、趋势与预测(2025-2032)

医疗旅游市场:全球产业分析、规模、份额、成长、趋势与预测(2025-2032) 2032 年医疗旅游市场预测:按治疗类型、旅客类型、服务提供者、预订管道和地区进行的全球分析医疗旅游市场-2025年至2030年的预测

2032 年医疗旅游市场预测:按治疗类型、旅客类型、服务提供者、预订管道和地区进行的全球分析医疗旅游市场-2025年至2030年的预测 全球生育旅游市场

全球生育旅游市场