|

市场调查报告书

商品编码

1959665

太空网路安全市场机会、成长要素、产业趋势分析及2026年至2035年预测Space Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球太空网路安全市场价值 49 亿美元,预计到 2035 年将达到 126 亿美元,年复合成长率为 10.3%。

市场扩张的驱动力来自于针对卫星指挥控制系统的网路攻击日益增多,以及国防机构对太空基础设施在情报、监视和侦察方面日益增长的依赖。向软体定义卫星和云端赋能地面基础设施的转变,显着提高了商业、民用和军事航太专案的网路安全要求。随着在轨资产的互联互通程度和资料密集度不断提高,保护关键任务系统免受入侵、破坏和资料篡改已成为一项策略重点。低地球轨道卫星星系的快速部署正在重塑安全框架,因为监管机构和营运商都意识到网路拥塞和讯号干扰带来的风险日益增加。加强整个航太供应链的网路安全也在改变采购模式,尤其是在卫星软体、半导体组件和子系统外包日益增加的情况下。更高的合规标准和更严格的监管正在提高可靠性,最大限度地减少第三方漏洞,并增强系统应对新兴数位威胁的韧性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 49亿美元 |

| 预测金额 | 126亿美元 |

| 复合年增长率 | 10.3% |

到2025年,软体和平台领域将占据55.8%的市场份额,这反映了其在保护卫星任务和地面基础设施方面的核心作用。先进的网路安全平台支援加密管理、存取认证、异常检测以及对在轨和地面系统的持续监控。基于云端的架构、扩充性以及与软体定义卫星的兼容性,使得这些平台对于主动风险缓解至关重要。随着营运商将即时威胁情报和自动化回应机制置于优先地位,对安全数位平台的投资也持续成长。

受卫星对地通讯和星间通讯中讯号拦截、欺骗和干扰风险日益增加的驱动,通讯链路安全领域预计将在2026年至2035年间以11.3%的复合年增长率增长。卫星频宽的扩展和轨道上卫星的高密度部署,大大提高了对先进加密通讯协定、多层认证和抗干扰技术的需求。确保复杂空间通讯网路中的资料传输安全,是政府和相关人员都高度关注的领域。

预计2025年,北美空间网路安全市场占有率将达到48.3%。推动该地区成长的因素包括卫星基础设施面临的威胁日益增加、对太空通讯的依赖性不断增强,以及用于国防和商业用途的先进卫星星系的快速部署。软体定义卫星系统和云端整合地面站的广泛应用加剧了网路风险,促使企业加大对零信任架构、人工智慧驱动的威胁分析以及改进型卫星设计的投资。网路安全领域的公私合营进一步巩固了该地区在这一新兴市场的领先地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 针对卫星指挥控制系统的网路攻击日益增多

- 低地球轨道卫星卫星群的激增

- 军事力量对天基情报、监视和侦察资产的依赖日益增强

- 整合基于云端的地面站架构

- 卫星通讯和资讯服务的商业化

- 产业潜在风险与挑战

- 针对航太系统的网路安全标准有限

- 不具备机载安全升级能力的传统卫星

- 市场机会

- 卫星到地面通讯中的零信任架构

- 面向空间任务网路的AI驱动异常检测

- 促进因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 依交付方式分類的市场估算与预测,2022-2035年

- 硬体

- 加密模组

- 安全启动和可信任执行

- 针对干扰和安全通讯的对策

- 软体和平台

- 加密/加密技术

- 存取控制和身份验证

- 威胁侦测与监控

- 指挥与控制(C2)安全

- 网路弹性与復原平台

- 服务

- 託管服务

- 专业服务及咨询服务

第六章 市场估计与预测:依发展阶段划分,2022-2035年

- 空间段(在轨)安全

- 地面段安全

- 链路段(通讯)安全

- 用户段安全

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 卫星通讯

- 地球观测与遥感探测

- 导航与定位(PNT)

- 太空探勘与科学任务

- 其他的

第八章 市场估算与预测:依最终用途产业划分,2022-2035年

- 国防和国家安全机构

- 私人政府航太机构和研究机构

- 商业航太资产营运商

- 下游服务供应商和系统整合商

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 主要企业

- Airbus SE

- RTX Corporation

- BAE Systems Plc

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Thales Group

- Leonardo SpA

- 按地区分類的主要企业

- 北美洲

- Booz Allen Hamilton

- General Dynamics Corporation

- L3Harris Technologies, Inc.

- Leidos Holdings, Inc.

- CGI Group

- 亚太地区

- Cisco Systems, Inc.

- 欧洲

- Check Point Software Technologies

- 北美洲

- 特殊玩家/干扰者

- Anduril Industries, Inc.

- CrowdStrike Holdings, Inc.

- Fortinet, Inc.

- Nightwing Technologies

- Xage Security, Inc.

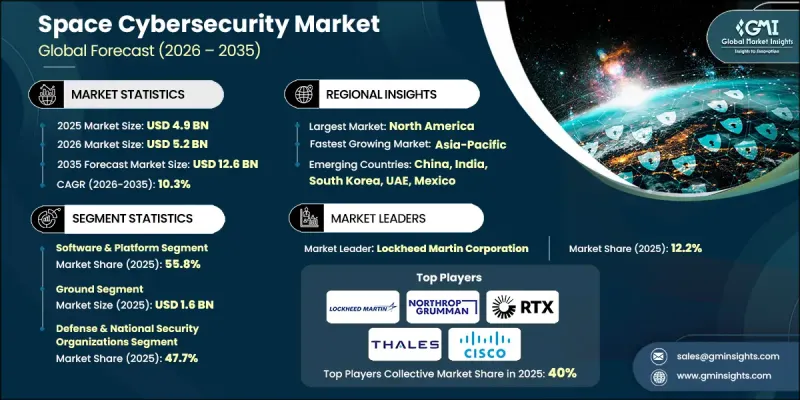

The Global Space Cybersecurity Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 12.6 billion by 2035.

Market expansion is driven by the growing number of cyberattacks targeting satellite command-and-control systems and the increasing reliance of defense organizations on space-based intelligence, surveillance, and reconnaissance capabilities. The transition toward software-defined satellites and cloud-enabled ground infrastructure is significantly elevating cybersecurity requirements across commercial, civil, and military space programs. As orbital assets become more interconnected and data-intensive, protecting mission-critical systems from intrusion, disruption, and data manipulation has become a strategic priority. The rapid deployment of low-earth orbit satellite constellations is reshaping security frameworks, as regulators and operators recognize heightened risks associated with network congestion and signal interference. Strengthening cybersecurity across the space supply chain is also transforming procurement models, particularly as outsourcing of satellite software, semiconductor components, and subsystems increases. Enhanced compliance standards and stricter oversight are improving trust, minimizing third-party vulnerabilities, and reinforcing system resilience against emerging digital threats.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 10.3% |

The software and platform segment accounted for 55.8% share in 2025, reflecting its central role in safeguarding satellite missions and ground-based infrastructure. Advanced cybersecurity platforms support encryption management, access authentication, anomaly detection, and continuous monitoring of orbital and terrestrial systems. Their scalability and compatibility with cloud-based architectures and software-defined satellites make them indispensable for proactive risk mitigation. As operators prioritize real-time threat intelligence and automated response mechanisms, investment in secure digital platforms continues to rise.

The communication link security segment is projected to grow at a CAGR of 11.3% during 2026-2035, fueled by increasing risks of signal interception, spoofing, and jamming across satellite-to-ground and inter-satellite connections. Expanding satellite bandwidth capabilities and dense orbital deployments are intensifying the need for advanced encryption protocols, multi-layer authentication, and anti-interference technologies. Ensuring secure data transmission across complex space communication networks has become a high-growth focus area for both government and commercial stakeholders.

North America Space Cybersecurity Market held a 48.3% share in 2025. Regional growth is supported by rising threats to satellite infrastructure, expanding dependence on space-based communications, and rapid deployment of advanced satellite constellations for defense and commercial purposes. Strong adoption of software-defined satellite systems and cloud-integrated ground stations is increasing exposure to cyber risks, prompting investment in zero-trust architectures, AI-driven threat analytics, and hardened satellite designs. Public and private sector collaboration in cybersecurity innovation further reinforces the region's leadership in this evolving market.

Key companies operating in the Global Space Cybersecurity Market include Lockheed Martin Corporation, Thales Group, Northrop Grumman Corporation, Airbus SE, L3Harris Technologies, Inc., RTX Corporation, Leonardo S.p.A., Booz Allen Hamilton, General Dynamics Corporation, Leidos Holdings, Inc., BAE Systems Plc, Cisco Systems, Inc., Fortinet, Inc., Check Point Software Technologies, CrowdStrike Holdings, Inc., CGI Group, Anduril Industries, Inc., Xage Security, Inc., and Nightwing Technologies. Companies in the Space Cybersecurity Market are strengthening their competitive positions by investing heavily in advanced encryption technologies, AI-powered threat detection, and post-quantum cryptography research to address future risks. Strategic partnerships with satellite manufacturers, defense agencies, and cloud service providers enable integrated security frameworks across orbital and ground systems. Firms are expanding managed security services and offering end-to-end cybersecurity platforms tailored for space missions. They are also focusing on compliance-driven solutions aligned with evolving regulatory mandates, while enhancing supply chain transparency to mitigate third-party risks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering type trends

- 2.2.2 Deployment trends

- 2.2.3 Application trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cyberattacks on satellite command-and-control systems

- 3.2.1.2 Proliferation of LEO satellite mega-constellations

- 3.2.1.3 Increased military reliance on space-based ISR assets

- 3.2.1.4 Integration of cloud-based ground station architectures

- 3.2.1.5 Commercialization of satellite communications and data services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited cybersecurity standards specific to space systems

- 3.2.2.2 Legacy satellites lacking onboard security upgrade capabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Zero-trust architectures for satellite-ground communications

- 3.2.3.2 AI-driven anomaly detection for space mission networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cryptographic modules

- 5.2.2 Secure boot & trusted execution

- 5.2.3 Anti-jamming & secure communication

- 5.3 Software & platform

- 5.3.1 Encryption & cryptography

- 5.3.2 Access control & authentication

- 5.3.3 Threat detection & monitoring

- 5.3.4 Command & control (C2) security

- 5.3.5 Cyber resilience & recovery platforms

- 5.4 Services

- 5.4.1 Managed services

- 5.4.2 Professional & consulting services

Chapter 6 Market Estimates and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Space segment (on-orbit) security

- 6.3 Ground segment security

- 6.4 Link segment (communication) security

- 6.5 User segment security

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Satellite communications

- 7.3 Earth observation & remote sensing

- 7.4 Navigation & positioning (PNT)

- 7.5 Space exploration & scientific missions

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Defense & national security organizations

- 8.3 Civil government space agencies & research institutions

- 8.4 Commercial space asset operators

- 8.5 Downstream service providers & system integrators

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Airbus SE

- 10.1.2 RTX Corporation

- 10.1.3 BAE Systems Plc

- 10.1.4 Lockheed Martin Corporation

- 10.1.5 Northrop Grumman Corporation

- 10.1.6 Thales Group

- 10.1.7 Leonardo S.p.A.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Booz Allen Hamilton

- 10.2.1.2 General Dynamics Corporation

- 10.2.1.3 L3Harris Technologies, Inc.

- 10.2.1.4 Leidos Holdings, Inc.

- 10.2.1.5 CGI Group

- 10.2.2 Asia Pacific

- 10.2.2.1 Cisco Systems, Inc.

- 10.2.3 Europe

- 10.2.3.1 Check Point Software Technologies

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Anduril Industries, Inc.

- 10.3.2 CrowdStrike Holdings, Inc.

- 10.3.3 Fortinet, Inc.

- 10.3.4 Nightwing Technologies

- 10.3.5 Xage Security, Inc.

2026年全球空间网路安全市场报告

2026年全球空间网路安全市场报告 国防网路安全市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测太空网路安全市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球国防网路安全市场规模、份额、趋势和成长分析报告(2026-2034)

国防网路安全市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测太空网路安全市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球国防网路安全市场规模、份额、趋势和成长分析报告(2026-2034) 国防网路安全市场-全球产业规模、份额、趋势、机会及按解决方案、地区和竞争格局分類的预测(2021-2031年)

国防网路安全市场-全球产业规模、份额、趋势、机会及按解决方案、地区和竞争格局分類的预测(2021-2031年) 宇宙网路安全的全球市场,报价环,各平台,各最终用途,各地区,机会,预测,2018年~2032年

宇宙网路安全的全球市场,报价环,各平台,各最终用途,各地区,机会,预测,2018年~2032年 宇宙网路安全市场,规模,占有率,趋势,产业分析报告:报价环,各平台,各终端用户,各地区-2025~2034年市场预测

宇宙网路安全市场,规模,占有率,趋势,产业分析报告:报价环,各平台,各终端用户,各地区-2025~2034年市场预测 空间网路安全市场规模、份额、趋势分析报告:按产品、平台、最终用途、地区、细分市场预测,2025-2033 年美国太空网路安全市场规模、份额、趋势分析报告:按产品、平台、最终用途、细分市场预测,2025-2033 年

空间网路安全市场规模、份额、趋势分析报告:按产品、平台、最终用途、地区、细分市场预测,2025-2033 年美国太空网路安全市场规模、份额、趋势分析报告:按产品、平台、最终用途、细分市场预测,2025-2033 年 国防网路安全市场:按平台、按解决方案、按类型、按最终用户、按地区

国防网路安全市场:按平台、按解决方案、按类型、按最终用户、按地区