|

市场调查报告书

商品编码

1982275

商用车及车队数位双胞胎市场:成长机会、成长要素、产业趋势分析及2026-2035年预测Commercial Vehicle and Fleet Digital Twin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

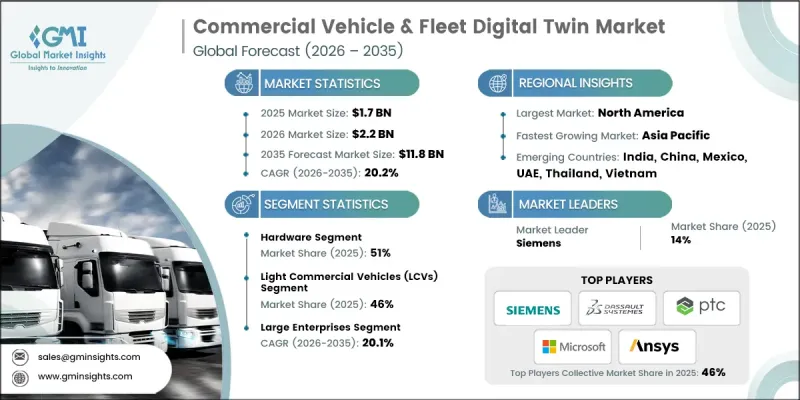

2025 年全球商用车和车队数位双胞胎市场价值 17 亿美元,预计到 2035 年将以 20.2% 的复合年增长率增长至 118 亿美元。

该市场专注于建立基于互联感测器、人工智慧、高级分析和可扩展云端环境的整个商用车和车队生态系统的动态虚拟副本。这些数位化框架使原始设备製造商 (OEM)、车队所有者和承运商能够即时监控资产状态、提升生命週期性能并优化营运效率。最初只是一个简单的车辆资料监控平台,如今已发展成为一个智慧的、模拟主导的系统,能够支援预测性维护、运转率预测和成本管理策略。物流网路日益数位化、合规要求日益严格以及车队营运日益复杂化,都推动了市场需求的成长。企业正在大力投资云端架构,以确保集中化的可视性、最大限度地减少停机时间并提高资产可靠性。随着车队现代化和先进技术的应用,数位双胞胎平台正成为全球运输网路中风险缓解、永续性评估和长期资本规划的关键工具。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 17亿美元 |

| 预计金额 | 118亿美元 |

| 复合年增长率 | 20.2% |

现代数位双胞胎平台的功能远远超过基础监控,提供人工智慧驱动的建模环境,能够模拟大规模运行工况和效能变数。车队营运商利用这些系统制定效率提升策略、分析资产利用模式、预测长期维护需求,并比较不同动力传动系统配置的总成本。先进的分析引擎还支援基于场景的路线优化、负载容量分布建模、排放气体分析和法规文件管理。与联网汽车技术的整合进一步增强了安全检验流程,并提升了各种运行工况下的效能基准测试。由于法规结构的不断改进和对营运透明度日益增长的期望,市场应用正在加速推进。美国国家公路交通安全管理局 (NHTSA) 正在扩大采用先进技术的商用车队的安全监控和数据报告标准,从而推动对支持即时合规性追踪、车辆诊断和营运风险评估的数位基础设施的投资增加。

预计到2025年,轻型商用车市占率将达到46%,复合年增长率(CAGR)为20.2%。总吨位在3.5吨至7.5吨之间的车辆因其高运转率和高营运负载而成为市场成长的主要驱动力。随着车队营运商寻求更高的调度精度、更精准的配送绩效追踪、更全面的驾驶员分析以及更优化的资产配置策略,该细分市场的需求正在迅速增长。数位双胞胎解决方案能够增强协调性、减少停机时间,并提高高密度配送环境中的路线效率。

预计到2025年,大型企业市占率将达到66%,并在2026年至2035年间以20.1%的复合年增长率成长。这些大型企业正在其庞大的车队中部署数位双胞胎孪生生态系统,并将其与企业平台集成,用于资源规划、运输管理、仓库协调和劳动力管理。混合云端和边缘运算模型支援进阶分析处理,而集中式营运框架则提供了跨地理分布网路的标准化视觉性。这些组织依靠预测智慧进行网路优化、监管报告和永续性评估,旨在降低碳排放强度并增强环境课责。

美国商用车和车队数位双胞胎市场预计到2025年将达到4.7亿美元,并在2026年至2035年间以19.5%的复合年增长率成长。美国凭藉严格的排放气体法规、加速推进的车队现代化计划以及人工智慧驱动的车队分析技术的广泛应用,保持其全球领先地位。对长途运输和基础设施现代化的需求正推动营运商和原始设备製造商(OEM)部署先进的数位双胞胎系统,以实现持续的性能监控和预测性维护。在不断扩展的联网汽车基础设施、有利于试点项目的法规结构以及集中的工程投资的支持下,德克萨斯州和亚利桑那州等州正在崛起为创新中心。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 物联网和联网汽车技术的广泛应用。

- 对预测性维护解决方案的需求日益增长

- 推动旨在提高车辆安全性和减少排放气体的法规

- 人们越来越关注车队的营运效率。

- 加速推广电动汽车车队

- 产业潜在风险与挑战

- 较高的初始设定成本

- 资料隐私和安全问题

- 缺乏标准化和互通性

- 熟练人员短缺

- 市场机会

- 新兴市场的扩张

- 与自动驾驶汽车开发结合

- 车辆电气化情境规划

- 开发产业专用的解决方案

- 车队数据分析的商业化

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国联邦政府关于数位双胞胎和车队管理的法规

- 加拿大 - 连网和自动驾驶汽车安全框架 (CASF)

- 欧洲

- 德国 - 欧盟智慧交通系统和国家数位双胞胎计划

- 英国:脱欧后车队ADAS与数位双胞胎技术指南

- 法国——国家ADAS测试和智慧交通系统战略

- 义大利——智慧交通系统试点计画和智慧基础设施

- 亚太地区

- 中国——工信部关于C-V2X的法规和标准

- 印度—ADAS和汽车互联的新法规

- 日本——智慧交通系统连结性与频率政策

- 澳洲—技术中立的智慧交通系统政策

- 拉丁美洲

- 墨西哥 - NOM 汽车安全标准

- 阿根廷 - 交通法第 24.449 号

- 中东和非洲

- 南非 - 道路交通法(1996 年)

- 沙乌地阿拉伯—2030愿景的交通运输法律与交通运输倡议

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 物联网和感测器技术

- 边缘运算基础设施

- 云端运算平台

- 人工智慧和机器学习演算法

- 新兴技术

- 5G和V2X集成

- 数位线程架构

- 区块链保障资料完整性

- 扩增实境(AR)介面

- 当前技术趋势

- 专利分析

- 专利申请趋势(2021-2025)

- 专利的地理分布

- 主要专利拥有者

- 主要技术丛集

- 价格分析

- 每辆车的订阅模式

- 每项功能的定价

- 付费使用制

- 企业授权合约

- 不同地区的价格差异

- 价格趋势和预测

- 使用案例和成功案例

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 数位双胞胎成熟度模型

- 一级:基本连接和数据采集

- 二级:即时监控和视觉化

- 第三级:预测分析与模拟

- 第四级:自主优化与控制

- 第五级:生态系整合与认知孪生

- 区域产业成熟度评估

- 互通性和整合挑战

- 旧有系统集成

- 多厂商平台相容性

- 数据标准化的挑战

- API 和中间件要求

- 制定互通性标准

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依组件划分,2022-2035年

- 硬体

- 物联网感测器和远端资讯处理设备

- 车载计算单元

- GPS和连接模组

- 软体

- 数位双胞胎平台与模拟软体

- 车队管理和分析软体

- 预测性维护和营运优化软体

- 服务

- 专业服务

- 託管服务

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第七章 市场估计与预测:依公司规模划分,2022-2035年

- 大公司

- 中小企业

第八章 市场估算与预测:依部署类型划分,2022-2035年

- 现场

- 基于云端的

- 杂交种

第九章 市场估计与预测:依最终用途划分,2022-2035年

- OEM

- 车辆所有者和物流公司

- 一级和二级供应商

- 汽车软体和技术供应商

- 售后市场及服务中心

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 瑞典

- 丹麦

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

第十一章:公司简介

- 世界公司

- ANSYS

- Dassault Systemes

- General Electric(GE Digital)

- Hexagon

- IBM

- Microsoft

- PTC

- Siemens

- 当地公司

- Descartes Systems

- Daimler Truck

- Geotab

- NVIDIA

- Robert Bosch

- Motive(KeepTruckin)

- Samsara

- SAP

- Tata Consultancy Services

- Trimble

- Volvo

- 新兴企业

- Altair Engineering

- Intangles

The Global Commercial Vehicle & Fleet Digital Twin Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 20.2% to reach USD 11.8 billion by 2035.

The market focuses on creating dynamic virtual replicas of commercial vehicles and entire fleet ecosystems, powered by connected sensors, artificial intelligence, advanced analytics, and scalable cloud environments. These digital frameworks allow OEMs, fleet owners, and transportation companies to monitor asset health in real time, improve lifecycle performance, and streamline operational efficiency. What began as simple vehicle data monitoring platforms has transformed into intelligent, simulation-driven systems capable of supporting predictive maintenance, utilization forecasting, and cost control strategies. Growing demand is being fueled by increasing digitization across logistics networks, stronger compliance requirements, and the rising complexity of fleet operations. Companies are investing heavily in cloud-based architecture to gain centralized visibility, minimize downtime, and enhance asset reliability. As fleets modernize and incorporate advanced technologies, digital twin platforms are becoming essential tools for risk mitigation, sustainability measurement, and long-term capital planning across global transportation networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 20.2% |

Modern digital twin platforms now extend far beyond basic monitoring capabilities, offering AI-enabled modeling environments that simulate large-scale operational conditions and performance variables. Fleet operators use these systems to evaluate efficiency strategies, asset utilization patterns, long-term maintenance forecasting, and total cost comparisons across diverse powertrain configurations. Advanced analytics engines also enable scenario-based route optimization, load distribution modeling, emissions analysis, and regulatory documentation management. Integration with connected vehicle technologies further strengthens safety validation processes and performance benchmarking under varied operating conditions. Market adoption continues to accelerate due to evolving regulatory frameworks and heightened expectations around operational transparency. The National Highway Traffic Safety Administration has expanded safety oversight and data reporting standards for commercial fleets deploying advanced technologies, prompting increased investment in digital infrastructure that supports real-time compliance tracking, vehicle diagnostics, and operational risk assessment.

The light commercial vehicles segment accounted for 46% share in 2025 and is forecast to grow at a CAGR of 20.2%. Vehicles within the gross weight range of 3.5 to 7.5 metric tons led adoption due to their high utilization rates and operational intensity. Demand within this segment is expanding rapidly as fleet operators seek enhanced scheduling precision, delivery performance tracking, driver analytics, and optimized asset deployment strategies. Digital twin solutions enable improved coordination, reduced downtime, and higher route efficiency within dense distribution environments.

The large enterprises segment held 66% share in 2025 and is projected to grow at a CAGR of 20.1% from 2026 to 2035. Major corporations are deploying digital twin ecosystems across extensive fleets while integrating them with enterprise platforms for resource planning, transportation management, warehouse coordination, and workforce administration. Hybrid cloud and edge computing models support advanced analytics processing, while centralized operational frameworks provide standardized visibility across geographically dispersed networks. These organizations rely on predictive intelligence for network optimization, regulatory reporting, and sustainability measurement initiatives aimed at reducing carbon intensity and strengthening environmental accountability.

United States Commercial Vehicle & Fleet Digital Twin Market generated USD 470 million in 2025 and is expected to grow at a CAGR of 19.5% between 2026 and 2035. The country maintains global leadership due to stringent emissions policies, accelerating fleet modernization programs, and widespread adoption of AI-driven fleet analytics. Long-haul transportation demand and infrastructure modernization are encouraging operators and OEMs to deploy advanced digital twin systems for continuous performance monitoring and predictive servicing. States such as Texas and Arizona are emerging as innovation corridors supported by expanding connected vehicle infrastructure, pilot-friendly regulatory frameworks, and concentrated engineering investments.

Key participants shaping the Global Commercial Vehicle & Fleet Digital Twin Market include Siemens, IBM, NVIDIA, Dassault Systems, ANSYS, Microsoft, Hexagon, PTC, General Electric, and Descartes Systems. These companies compete through advanced simulation platforms, cloud-native architectures, AI acceleration technologies, and deep integration capabilities tailored for fleet-scale deployments. Companies operating in the Commercial Vehicle & Fleet Digital Twin Market are strengthening their foothold through continuous platform innovation, ecosystem partnerships, and vertical integration strategies. Providers are enhancing AI-driven predictive analytics, expanding cloud interoperability, and investing in scalable digital architectures to accommodate growing fleet complexity. Strategic alliances with OEMs, telematics providers, and logistics platforms are enabling seamless data exchange and end-to-end visibility. Many vendors are also prioritizing cybersecurity, regulatory alignment, and sustainability reporting capabilities to meet enterprise requirements. Geographic expansion, targeted acquisitions, and industry-specific solution customization further reinforce competitive positioning.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Components

- 2.2.3 Vehicles

- 2.2.4 Enterprise Size

- 2.2.5 Deployment Mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of IoT & connected vehicle technology

- 3.2.1.2 Rising demand for predictive maintenance solutions

- 3.2.1.3 Regulatory push for fleet safety & emissions reduction

- 3.2.1.4 Growing focus on fleet operational efficiency

- 3.2.1.5 Accelerating electric vehicle fleet adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation costs

- 3.2.2.2 Data privacy & security concerns

- 3.2.2.3 Lack of standardization & interoperability

- 3.2.2.4 Limited availability of skilled workforce

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Integration with autonomous vehicle development

- 3.2.3.3 Scenario planning for fleet electrification

- 3.2.3.4 Development of industry-specific solutions

- 3.2.3.5 Monetization of fleet data analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal digital twin and fleet management regulations

- 3.4.1.2 Canada - Connected and autonomous fleet safety framework (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU ITS & national digital twin initiatives

- 3.4.2.2 UK- Post-Brexit ADAS and fleet digital twin guidance

- 3.4.2.3 France- National ADAS testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging ADAS & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 IoT & sensor technology

- 3.7.1.2 Edge computing infrastructure

- 3.7.1.3 Cloud computing platforms

- 3.7.1.4 AI & machine learning algorithms

- 3.7.2 Emerging technologies

- 3.7.2.1 5G & V2X integration

- 3.7.2.2 Digital thread architecture

- 3.7.2.3 Blockchain for data integrity

- 3.7.2.4 Augmented reality interfaces

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Patent filing trends (2021-2025)

- 3.8.2 Geographic distribution of patents

- 3.8.3 Top patent holders

- 3.8.4 Key technology clusters

- 3.9 Pricing analysis

- 3.9.1 Per-vehicle subscription model

- 3.9.2 Per-feature pricing

- 3.9.3 Usage-based pricing

- 3.9.4 Enterprise license agreements

- 3.9.5 Regional price variations

- 3.9.6 Price trends & forecasts

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Digital twin maturity model

- 3.12.1 Level 1: Basic connectivity & data collection

- 3.12.2 Level 2: Real-time monitoring & visualization

- 3.12.3 Level 3: Predictive analytics & simulation

- 3.12.4 Level 4: Autonomous optimization & control

- 3.12.5 Level 5: Ecosystem integration & cognitive twins

- 3.13 Industry maturity assessment by region

- 3.13.1 Interoperability & integration challenges

- 3.13.2 Legacy system integration

- 3.13.3 Multi-vendor platform compatibility

- 3.13.4 Data standardization issues

- 3.13.5 API & middleware requirements

- 3.13.6 Interoperability standards development

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Components, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 IoT sensors & telematics devices

- 5.2.2 Onboard computing units

- 5.2.3 GPS and connectivity modules

- 5.3 Software

- 5.3.1 Digital twin platform & simulation software

- 5.3.2 Fleet management and analytics software

- 5.3.3 Predictive maintenance & operational optimization software

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Light commercial vehicles (LCVs)

- 6.3 Medium commercial vehicles (MCVs)

- 6.4 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 Small & medium enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 On premises

- 8.3 Cloud-based

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Fleet operators & logistics companies

- 9.4 Tier 1 & Tier 2 suppliers

- 9.5 Automotive software & technology providers

- 9.6 Aftermarket & service centers

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ANSYS

- 11.1.2 Dassault Systemes

- 11.1.3 General Electric (GE Digital)

- 11.1.4 Hexagon

- 11.1.5 IBM

- 11.1.6 Microsoft

- 11.1.7 PTC

- 11.1.8 Siemens

- 11.2 Regional Players

- 11.2.1 Descartes Systems

- 11.2.2 Daimler Truck

- 11.2.3 Geotab

- 11.2.4 NVIDIA

- 11.2.5 Robert Bosch

- 11.2.6 Motive (KeepTruckin)

- 11.2.7 Samsara

- 11.2.8 SAP

- 11.2.9 Tata Consultancy Services

- 11.2.10 Trimble

- 11.2.11 Volvo

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 Altair Engineering

- 11.3.2 Intangles

2026年全球数位双胞胎隧道通风市场报告2026年航太与国防领域数位双胞胎全球市场报告

2026年全球数位双胞胎隧道通风市场报告2026年航太与国防领域数位双胞胎全球市场报告 2034年航太数位双胞胎市场预测:按组件、部署模式、类型、技术、应用、最终用户和地区分類的全球分析数位双胞胎市场预测:永续製造领域至2034年-全球分析(按孪生类型、组件、部署模式、应用、最终用户和地区划分)2026年全球数位双胞胎孪生即服务市场报告2026年全球数位双胞胎技术市场报告2026年全球物流数位双胞胎市场报告2026年全球人工智慧(AI)增强数位双胞胎品质指数市场报告2026年全球数位双胞胎市场报告

2034年航太数位双胞胎市场预测:按组件、部署模式、类型、技术、应用、最终用户和地区分類的全球分析数位双胞胎市场预测:永续製造领域至2034年-全球分析(按孪生类型、组件、部署模式、应用、最终用户和地区划分)2026年全球数位双胞胎孪生即服务市场报告2026年全球数位双胞胎技术市场报告2026年全球物流数位双胞胎市场报告2026年全球人工智慧(AI)增强数位双胞胎品质指数市场报告2026年全球数位双胞胎市场报告 全机械化采矿作业的数位双胞胎系统市场:按组件、部署类型、应用和最终用户划分——2026-2032年全球预测

全机械化采矿作业的数位双胞胎系统市场:按组件、部署类型、应用和最终用户划分——2026-2032年全球预测