|

市场调查报告书

商品编码

1982277

2026 年至 2035 年家用电子电器製造设备的市场机会、成长要素、产业趋势分析与预测。Consumer Electronics Manufacturing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

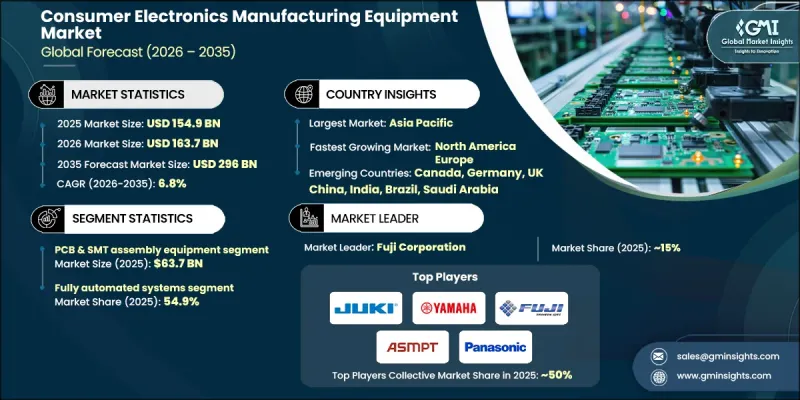

预计到 2025 年,全球家用电子电器製造设备市场规模将达到 1,549 亿美元,并预计以 6.8% 的复合年增长率成长,到 2035 年达到 2,960 亿美元。

市场成长的驱动力在于消费者对紧凑型、高性能电子产品日益增长的期望,而这些产品对生产能力的要求也越来越高。为了满足性能和设计要求,设备製造商正优先考虑精密工程、高密度整合和先进的製造流程。这种转变正在加速对下一代组装、检测和半导体生产系统的投资,这些系统能够处理复杂的架构和微型化的元件。不断扩展的连接趋势和下一代通讯技术也促进了产量的成长和对更复杂元件的需求。随着电子产品变得越来越复杂,製造商正在采用高吞吐量的自动化解决方案来维持品质、提高效率并扩大生产规模。向先进封装技术和基板设计的转变进一步推动了对尖端生产工具的需求。总而言之,製造流程的持续创新、全球电子产品消费量的成长以及整合系统日益复杂化,都为这个市场带来了益处。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 1549亿美元 |

| 预测金额 | 2960亿美元 |

| 复合年增长率 | 6.8% |

预计到2025年,PCB和SMT组装设备市场规模将达到637亿美元,并在2026年至2035年间以6.5%的复合年增长率成长。自动化、机器人技术的整合以及人工智慧检测技术的广泛应用,提高了生产效率和产量比率,从而推动了设备升级。製造商正在实施智慧缺陷检测、预测性维护模型、即时过程追踪和精密返工能力,以减少停机时间并提高营运效率。这些技术进步正在推动PCB和SMT生产线的持续现代化。

预计到2025年,全自动化系统市占率将达到54.9%,并在2026年至2035年间以7%的复合年增长率成长。各公司正在将人工智慧驱动的分析、机器人搬运系统、物联网监控设备、数位模拟工具和预测性维护平台整合到其製造环境中,以优化生产效率并最大限度地减少错误。日益激烈的全球竞争、不断上涨的人事费用以及小型化和复杂化电子组件带来的技术挑战,正在加速向全面自动化解决方案的转型。

美国家用电子电器製造设备市场预计到2025年将达到291亿美元,并在2026年至2035年间以6.2%的复合年增长率成长。由于对先进半导体技术、数据基础设施组件以及人工智慧专用硬体系统的需求不断增长,国内产能正在扩张。主要晶片製造商的大规模资本投资,以及支持国内製造业的公共倡议,正在加强区域供应链。全国各地的製造工厂越来越多地采用人工智慧驱动的品管系统、机器人、智慧工厂框架和预测分析平台,这推动了对先进SMT、半导体製造、测试和自动化设备的需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 对体积更小、性能更高的电子设备的需求日益增长。

- 物联网、5G和互联技术的扩展。

- 汽车电子和电气化(电动车)的成长

- 产业潜在风险与挑战

- 供应链中断和零件短缺

- 技术复杂性不断增加,产品週期不断缩短

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过装置

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依设备类型划分,2022-2035年

- PCB及SMT组装设备

- 测试和检验设备

- 零件运输和储存系统

- 组装和整合系统

- 涂层和点胶设备

- 清洁和表面处理设备

- 标记和贴标设备

- 切割/分离设备

第六章 市场估计与预测:依技术划分,2022-2035年

- 全自动系统

- 半自动系统

- 手动/基本系统

第七章 市场估价与预测:依驱动零件划分,2022-2035年

- 线性滑轨

- 伸缩式轨道

- 线性致动器

- 滚珠螺桿

- 整合运动系统

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 家用电子电器製造商

- OSAT(外包半导体组装和测试服务)供应商

- 通讯电子设备

- 汽车电子

- 工业和物联网电子产品

第九章 市场估价与预测:依通路划分,2022-2035年

- 直销

- 间接销售

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十一章:公司简介

- ABB Robotics

- Bosch Rexroth AG

- FANUC Corporation

- Fuji Corporation

- Hiwin Technologies Corporation

- JUKI Corporation

- KLA Corporation

- KUKA AG

- Mycronic AB

- Nordson Corporation

- NSK Ltd.

- Omron Corporation

- Saki Corporation

- The Timken Company

- THK Co., Ltd.

- Yamaha Motor Corporation

- Yaskawa Electric

The Global Consumer Electronics Manufacturing Equipment Market was valued at USD 154.9 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 296 billion by 2035.

Market growth is driven by rising expectations for compact, high-performance electronic products that require increasingly advanced production capabilities. Device manufacturers are prioritizing precision engineering, high-density integration, and advanced fabrication processes to meet performance and design demands. This shift is accelerating investments in next-generation assembly, inspection, and semiconductor production systems capable of handling complex architectures and miniaturized components. Growing connectivity trends and next-wave communication technologies are also contributing to higher production volumes and more intricate component requirements. As electronics become more sophisticated, manufacturers are deploying high-throughput, automated solutions to maintain quality, improve efficiency, and scale output. The transition toward advanced packaging techniques and multilayer board designs further supports demand for cutting-edge production tools. Overall, the market is benefiting from continuous innovation in manufacturing processes, rising global electronics consumption, and the increasing complexity of integrated systems."

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $154.9 Billion |

| Forecast Value | $296 Billion |

| CAGR | 6.8% |

The PCB and SMT assembly equipment segment generated USD 63.7 billion in 2025 and is forecast to grow at a CAGR of 6.5% from 2026 to 2035. Equipment upgrades are being fueled by widespread adoption of automation, robotics integration, and AI-powered inspection technologies that enhance productivity and improve yield rates. Manufacturers are implementing intelligent defect recognition, predictive servicing models, live process tracking, and precision rework capabilities to reduce downtime and improve operational efficiency. These advancements are encouraging the continuous modernization of PCB and SMT production lines.

The fully automated systems segment accounted for 54.9% share in 2025 and is projected to grow at a CAGR of 7% between 2026 and 2035. Companies are embedding AI-driven analytics, robotic handling systems, IoT-enabled monitoring devices, digital simulation tools, and predictive maintenance platforms into manufacturing environments to optimize throughput and minimize errors. Increasing global competition, higher labor expenses, and the technical challenges associated with miniaturized and complex electronic assemblies are accelerating the transition toward comprehensive automation solutions.

U.S. Consumer Electronics Manufacturing Equipment Market reached USD 29.1 billion in 2025 and is expected to grow at a CAGR of 6.2% from 2026 to 2035. Domestic production capacity is expanding due to heightened demand for advanced semiconductor technologies, data infrastructure components, and AI-focused hardware systems. Public policy initiatives supporting onshore manufacturing, along with large-scale capital investments by leading chip producers, are reinforcing local supply chains. Manufacturing facilities across the country are increasingly adopting AI-enabled quality systems, robotics, smart factory frameworks, and predictive analytics platforms, thereby strengthening demand for advanced SMT, semiconductor fabrication, testing, and automation equipment.

Key companies operating in the Global Consumer Electronics Manufacturing Equipment Market include KLA Corporation, FANUC Corporation, ABB Robotics, Yaskawa Electric, KUKA AG, Yamaha Motor Corporation, JUKI Corporation, Bosch Rexroth AG, Mycronic AB, Omron Corporation, Fuji Corporation, THK Co., Ltd., The Timken Company, Nordson Corporation, NSK Ltd., Saki Corporation, and Hiwin Technologies Corporation. Companies competing in the Global Consumer Electronics Manufacturing Equipment Market are reinforcing their position through continuous innovation and strategic investment. Many firms are expanding research and development capabilities to introduce high-precision, AI-integrated, and automation-centric equipment that enhances production scalability and reliability. Strategic partnerships with semiconductor manufacturers and electronics producers are strengthening long-term supply agreements and recurring revenue streams. Organizations are also focusing on geographic expansion, particularly in regions experiencing semiconductor capacity growth. Investments in digital manufacturing ecosystems, predictive maintenance platforms, and smart factory integration are improving customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Technology

- 2.2.4 Motion component

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for miniaturized and high-performance electronic devices

- 3.2.1.2 Expansion of IoT, 5G, and connected technologies

- 3.2.1.3 Growth of automotive electronics and electrification (EVs)

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions and component shortages

- 3.2.2.2 Increasing technological complexity and faster product cycles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 PCB & SMT assembly equipment

- 5.3 Testing & inspection equipment

- 5.4 Component handling & storage systems

- 5.5 Assembly & integration systems

- 5.6 Coating & dispensing equipment

- 5.7 Cleaning & surface preparation equipment

- 5.8 Marking & labelling equipment

- 5.9 Cutting & singulation equipment

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Fully automated systems

- 6.3 Semi-automated systems

- 6.4 Manual/basic systems

Chapter 7 Market Estimates & Forecast, By Motion component, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Linear guides

- 7.3 Telescopic rails

- 7.4 Linear actuators

- 7.5 Ball screws

- 7.6 Integrated motion systems

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Consumer electronics manufacturers

- 8.3 OSAT (outsourced semiconductor assembly & test) providers

- 8.4 Telecommunications electronics

- 8.5 Automotive electronics

- 8.6 Industrial and IoT electronics

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ABB Robotics

- 11.2 Bosch Rexroth AG

- 11.3 FANUC Corporation

- 11.4 Fuji Corporation

- 11.5 Hiwin Technologies Corporation

- 11.6 JUKI Corporation

- 11.7 KLA Corporation

- 11.8 KUKA AG

- 11.9 Mycronic AB

- 11.10 Nordson Corporation

- 11.11 NSK Ltd.

- 11.12 Omron Corporation

- 11.13 Saki Corporation

- 11.14 The Timken Company

- 11.15 THK Co., Ltd.

- 11.16 Yamaha Motor Corporation

- 11.17 Yaskawa Electric

电子受託製造服务 (EMS) 市场:2026-2032 年全球市场预测(按服务类型、技术、组件类型、应用、服务交付模式和客户规模划分)

电子受託製造服务 (EMS) 市场:2026-2032 年全球市场预测(按服务类型、技术、组件类型、应用、服务交付模式和客户规模划分) EMS和ODM-2026年至2032年全球市占率和排名、总收入和需求预测家用电子电器製造市场:2026-2032年全球市场预测(依产品类型、外形、模组、製造模式、材料、应用及通路划分)

EMS和ODM-2026年至2032年全球市占率和排名、总收入和需求预测家用电子电器製造市场:2026-2032年全球市场预测(依产品类型、外形、模组、製造模式、材料、应用及通路划分) 电子製造服务 (EMS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、零件、应用、製程、最终用户、解决方案和阶段划分

电子製造服务 (EMS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、零件、应用、製程、最终用户、解决方案和阶段划分 2026年全球通讯和电子製造服务市场报告

2026年全球通讯和电子製造服务市场报告 电子製造服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026年全球绿色电子製造市场报告

电子製造服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026年全球绿色电子製造市场报告 电子製造服务市场-全球产业规模、份额、趋势、机会、预测:按服务类型、产业、地区和竞争格局划分,2021-2031年绿色电子製造市场-全球产业规模、份额、趋势、机会及预测(依技术、服务、产业、地区及竞争格局划分,2021-2031年)

电子製造服务市场-全球产业规模、份额、趋势、机会、预测:按服务类型、产业、地区和竞争格局划分,2021-2031年绿色电子製造市场-全球产业规模、份额、趋势、机会及预测(依技术、服务、产业、地区及竞争格局划分,2021-2031年) 电子製造服务 (EMS) 市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测 (2026-2034)

电子製造服务 (EMS) 市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测 (2026-2034)