|

市场调查报告书

商品编码

1982287

2026 年至 2035 年含维生素 C护肤品的市场机会、成长要素、产业趋势与预测。Vitamin C Based Skincare Product Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

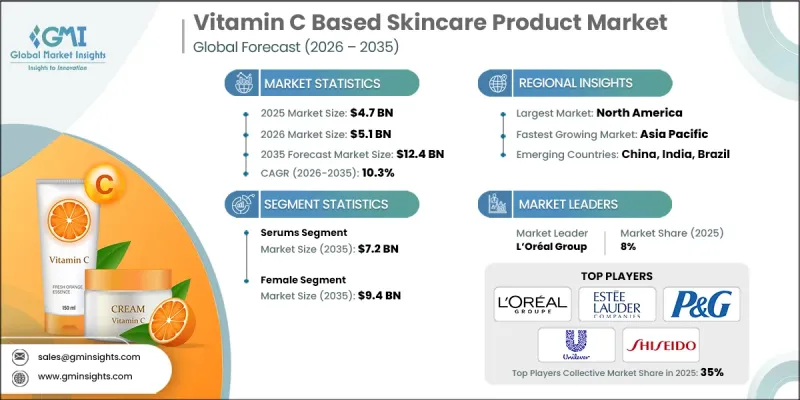

2025年全球含维生素C护肤品市场价值47亿美元,预计2035年将以10.3%的复合年增长率成长至124亿美元。

产业成长的驱动力在于消费者对兼具清洁形象和临床验证功效的高效配方产品的强烈偏好。消费者越来越重视经证实的亮白、均匀肤色和抗衰老功效,这推动了脸部保养品类的持续需求。社群媒体主导的产品发现通路的快速扩张、药妆店主导的皮肤护理产品分销管道的增长,以及老牌美容产品製造商不断丰富产品系列併推出涵盖不同价位的稳定衍生产品,进一步巩固了这一增长势头。主要企业之间的策略整合和投资活动正在加速配方技术、保护性包装解决方案和全通路分销网络的创新。儘管北美和欧洲市场仍是成熟的收入来源,但亚太地区凭藉着不断提升的护肤意识和优质化趋势,正成为强劲的成长引擎。在整个品类中,消费者正从基础护肤转向旨在显着改善和维持整体肤质的高效护肤系统。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 47亿美元 |

| 预计金额 | 124亿美元 |

| 复合年增长率 | 10.3% |

传统的低浓度美白霜正逐渐被更先进的维生素C复合物所取代,这些复合物旨在提供更高的稳定性和更佳的功效。最新的配方融合了高纯度左旋维生素C以及新一代衍生物,旨在增强其相容性和持久性。这些系统通常与互补的抗氧化剂和屏障支持成分相结合,以优化功效并延长使用寿命。诸如微囊包裹、无水配方、精确控制的pH环境以及保护性包装等技术进步有助于抑制氧化并保持产品品质。轻盈的液体、快速吸收的浓缩液和细腻的乳霜质地进一步提升了用户体验,同时保留了活性成分并最大限度地减少了皮肤刺激。

预计到2025年,精华液市场规模将达27亿美元,2035年将达72亿美元。这个细分市场之所以能推动整体需求成长,是因为浓缩型产品能够快速吸收,显着改善肌肤光泽、均匀肤色,并增强肌肤抵御环境压力的能力。消费者之所以青睐精华液,是因为与传统乳霜相比,精华液更容易迭加使用,而且能够更快地带来可见的效果。

预计到2025年,女性消费者市场规模将达到36亿美元,占总市场份额的76%,并预计在2035年达到94亿美元。由于女性对改善肤色和预防性护肤策略的意识较高,她们仍然是维生素C护肤品的主要使用者。在多步骤的美容护肤流程中,维生素C护理通常被视为基本步骤,特别适用于解决色素沉淀和长期皮肤弹性问题。

美国维生素C护肤市场预计到2025年将达到15亿美元,到2035年将达到45亿美元。在消费者信赖皮肤科医生推荐产品、成熟的数位化零售生态系统以及强大的药房分销管道的推动下,美国市场持续稳定成长。消费者尤其青睐高效稳定的维生素C产品,这类产品旨在平衡功效和皮肤刺激性,进一步巩固了美国在全球市场的主导地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 临床级美白溶液的应用日益普及

- 清洁美容运动和成分透明度

- 皮肤科和专业护肤的效果

- 产业潜在风险与挑战

- 维生素C的不稳定性及氧化

- 对刺激和致敏的担忧

- 机会

- 多活性和混合配方的兴起

- 亚太地区「美白护肤」文化的兴起

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

- 贸易数据分析

- 进出口量及进口额趋势

- 主要贸易走廊及关税的影响

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- 预测分析在产品开发的应用

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 美容精华液

- 乳霜和保湿霜

- 安瓿浓缩液

- 眼科治疗

- 面膜治疗

- 其他的

第六章 市场估计与预测:依维生素C衍生物划分,2022-2035年

- L-抗坏血酸(纯产品)

- 抗坏血酸葡糖苷

- 乙基抗坏血酸

- SAP/MAP

- THD/四异棕榈酸

- 其他的

第七章 市场估计与预测:依价格区间划分,2022-2035年

第八章 主要趋势

- 大众市场(10-40美元)

- 高级版(40-150 美元)

- 奢侈品(超过 150 美元)

第九章 市场估计与预测:性别,2022-2035年

- 男性

- 女士

第十章 市场估价与预测:依通路划分,2022-2035年

- 在线的

- 电子商务

- 企业网站

- 离线

- 大卖场和超级市场

- 药房/皮肤化妆品

- 专卖店

- 其他(直销、美容院、水疗中心、免税店)

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- Amorepacific Corporation

- Beiersdorf AG

- 雅诗兰黛公司

- Johnson & Johnson Consumer Inc.

- L'Oreal Group

- Mad Hippie Skin Care Products

- Murad LLC

- Paula's Choice Skincare

- Peter Thomas Roth Labs LLC

- Procter & Gamble Co.

- Shiseido Company, Limited

- Sunday Riley Modern Skincare LLC

- Timeless Skin Care

- TruSkin Naturals LLC

- Unilever PLC

The Global Vitamin C Based Skincare Product Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 12.4 billion by 2035.

Industry growth is fueled by a pronounced consumer preference for results-driven formulations that combine clean positioning with clinically supported performance. Buyers increasingly prioritize proven brightening, tone-evening, and age-defying benefits, driving sustained demand across facial care categories. Momentum is further reinforced by the rapid rise of social-driven product discovery, the expansion of pharmacy-led dermo-cosmetic distribution, and continuous portfolio diversification by established beauty manufacturers introducing stabilized derivatives across varied price points. Strategic consolidation and investment activity among leading companies are accelerating innovation in formulation technologies, protective packaging solutions, and omnichannel distribution networks. North America and Europe remain mature revenue generators, while Asia Pacific represents a strong growth engine supported by rising skincare awareness and premiumization trends. Across the category, consumers are transitioning away from basic skincare toward high-performance systems designed for visible, measurable improvements in overall skin quality and long-term maintenance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.7 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 10.3% |

Conventional low-strength brightening creams are steadily giving way to advanced vitamin C complexes engineered for higher stability and performance. Modern formulations incorporate pure L-ascorbic acid alongside next-generation derivatives designed to enhance compatibility and longevity. These systems are often combined with complementary antioxidants and barrier-support ingredients to optimize effectiveness and durability. Technological advancements such as encapsulation delivery methods, water-free compositions, carefully calibrated pH environments, and protective packaging formats help reduce oxidation and maintain product integrity. Lightweight liquids, fast-absorbing concentrates, and refined cream textures further improve user experience while preserving potency and minimizing sensitivity concerns.

The serums category generated USD 2.7 billion in 2025 and is forecast to reach USD 7.2 billion by 2035. This segment leads overall demand because concentrated formats deliver rapid absorption and noticeable improvements in radiance, uneven tone, and environmental stress defense. Consumers gravitate toward these formulations due to their efficient layering compatibility and reputation for faster visible transformation compared with traditional creams.

The female consumers segment accounted for USD 3.6 billion, holding 76% share in 2025, and is expected to reach USD 9.4 billion by 2035. Women remain the primary adopters of vitamin C skincare solutions, supported by strong awareness of complexion enhancement and preventative skin health strategies. Multi-step beauty regimens frequently position vitamin C treatments as foundational components, particularly for concerns related to discoloration and long-term dermal resilience.

United States Vitamin C Based Skincare Product Market reached USD 1.5 billion in 2025 and is projected to reach USD 4.5 billion by 2035. The country continues to demonstrate consistent growth driven by confidence in dermatologist-supported products, a well-established digital retail ecosystem, and strong pharmacy distribution channels. Consumers show a marked preference for high-efficacy, stabilized vitamin C solutions designed to balance strength with skin tolerance, reinforcing the nation's leadership position within the global landscape.

Key industry participants shaping the competitive environment include Beiersdorf AG, Amorepacific Corporation, Procter & Gamble Co., L'Oreal Group, Estee Lauder Companies Inc., Unilever PLC, Shiseido Company, Limited, Johnson & Johnson Consumer Inc., Murad LLC, Peter Thomas Roth Labs LLC, Paula's Choice Skincare, Sunday Riley Modern Skincare LLC, Timeless Skin Care, TruSkin Naturals LLC, and Mad Hippie Skin Care Products. These companies compete through formulation innovation, clinical positioning, premium branding, and expansion across both mass and prestige retail channels. Companies operating in the vitamin C-based skincare products market are prioritizing research-driven formulation upgrades, strategic mergers, and targeted geographic expansion to reinforce competitive positioning. Many brands are investing in advanced stabilization technologies and proprietary delivery systems to differentiate product performance and extend shelf life. Portfolio diversification across premium and accessible price tiers allows companies to capture a broader consumer base while maintaining brand equity. Partnerships with dermatology professionals and pharmacy networks strengthen clinical credibility, while digital-first marketing strategies and influencer collaborations amplify visibility and conversion rates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vitamin C Derivative

- 2.2.4 Price Tier

- 2.2.5 Gender

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of clinical grade brightening solutions

- 3.2.1.2 Clean-beauty movement & ingredient transparency

- 3.2.1.3 Dermatology & professional skincare influence

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Instability & oxidation of Vitamin C

- 3.2.2.2 Irritation & sensitivity concerns

- 3.2.3 Opportunities

- 3.2.3.1 Rise of multi active & hybrid formulations

- 3.2.3.2 Growth of APAC brightening skincare culture

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis

- 3.10.1 Import & Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 Predictive Analytics for Product Development

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Serums

- 5.3 Creams & Moisturizers

- 5.4 Ampoules & Concentrates

- 5.5 Eye Treatments

- 5.6 Masks & Treatments

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Vitamin C Derivative, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 L-Ascorbic Acid (Pure)

- 6.3 Ascorbyl Glucoside

- 6.4 Ethyl Ascorbic Acid

- 6.5 SAP/MAP

- 6.6 THD/Tetraisopalmitate

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Price Tier, 2022 - 2035 (USD Billion) (Thousand Units)

Chapter 8 Key trends

- 8.1 Mass Market (USD10-40)

- 8.2 Premium (USD40-150)

- 8.3 Luxury (>USD150)

Chapter 9 Market Estimates and Forecast, By Gender, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Male

- 9.3 Female

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-Commerce

- 10.2.2 Company Website

- 10.3 Offline

- 10.3.1 Hypermarkets & Supermarkets

- 10.3.2 Pharmacy/Dermocosmetics

- 10.3.3 Specialty Stores

- 10.3.4 Others (Direct Sales, Salons, Spas, Duty-Free)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Amorepacific Corporation

- 12.2 Beiersdorf AG

- 12.3 Estee Lauder Companies Inc.

- 12.4 Johnson & Johnson Consumer Inc.

- 12.5 L'Oreal Group

- 12.6 Mad Hippie Skin Care Products

- 12.7 Murad LLC

- 12.8 Paula's Choice Skincare

- 12.9 Peter Thomas Roth Labs LLC

- 12.10 Procter & Gamble Co.

- 12.11 Shiseido Company, Limited

- 12.12 Sunday Riley Modern Skincare LLC

- 12.13 Timeless Skin Care

- 12.14 TruSkin Naturals LLC

- 12.15 Unilever PLC

化学换肤市场:按化学试剂、最终用户、应用和分销管道分類的全球市场预测,2026-2032年护肤品市场:2026-2032年全球市场预测(依产品类型、肌肤问题、销售管道及最终用户划分)医用级护肤市场:2026-2032年全球市场预测(按产品类型、原料来源、肤质、配方、活性成分类型、价格范围、包装、功能、应用、分销管道和最终用户划分)皮肤健康市场:全球市场按产品类型、分销管道、应用和最终用户分類的预测——2026-2032年高级临床护肤产品市场:2026-2032年全球市场预测(按产品类型、皮肤问题、剂型、价格范围、分销管道和最终用户划分)

化学换肤市场:按化学试剂、最终用户、应用和分销管道分類的全球市场预测,2026-2032年护肤品市场:2026-2032年全球市场预测(依产品类型、肌肤问题、销售管道及最终用户划分)医用级护肤市场:2026-2032年全球市场预测(按产品类型、原料来源、肤质、配方、活性成分类型、价格范围、包装、功能、应用、分销管道和最终用户划分)皮肤健康市场:全球市场按产品类型、分销管道、应用和最终用户分類的预测——2026-2032年高级临床护肤产品市场:2026-2032年全球市场预测(按产品类型、皮肤问题、剂型、价格范围、分销管道和最终用户划分) 2026-2030年全球视网醇护肤品市场洁面霜市场:依产品形态、肤质、年龄层、性别、价格范围、应用领域、包装类型、成分类型和分销管道划分-全球预测,2026-2032年

2026-2030年全球视网醇护肤品市场洁面霜市场:依产品形态、肤质、年龄层、性别、价格范围、应用领域、包装类型、成分类型和分销管道划分-全球预测,2026-2032年 头髮及身体喷雾市场:按类型、分销管道和地区划分(2026-2034 年)

头髮及身体喷雾市场:按类型、分销管道和地区划分(2026-2034 年) 2026-2030年全球青少年个人护理产品市场

2026-2030年全球青少年个人护理产品市场 基于微生物组的护肤疗法市场分析及预测(至2035年):按类型、产品、服务、技术、应用、最终用户、形式、材料类型和安装类型划分

基于微生物组的护肤疗法市场分析及预测(至2035年):按类型、产品、服务、技术、应用、最终用户、形式、材料类型和安装类型划分