|

市场调查报告书

商品编码

1982304

高尔夫球车市场商机、成长要素、产业趋势分析及2026-2035年预测。Golf Cart Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

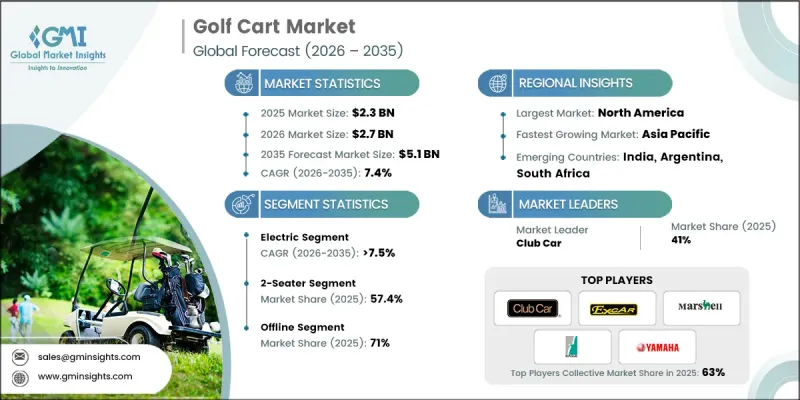

全球高尔夫球车市场预计到 2025 年将价值 23 亿美元,预计到 2035 年将以 7.4% 的复合年增长率增长至 51 亿美元。

市场成长主要得益于封闭式住宅社区、老年住宅计划以及规划完善的智慧城镇的快速发展,这些计画优先考虑紧凑型低速交通工具。高尔夫球车作为一种经济便捷的短程交通途径,正日益融入精心管理的住宅环境中。强调行人友善布局和低排放交通途径的城市发展策略进一步加速了高尔夫球车的普及。因此,配套完善的规划社区配备了专用车道和充电基础设施,为全球稳定的车辆更新换代和市场扩张创造了机会。同时,製造商正积极寻求併购、合作以及推出新产品,以增强自身竞争力。随着向锂离子电池系统和全面电气化的转型不断推进,产业格局正在发生巨大变化。与传统电池技术相比,锂离子电池解决方案具有更长的使用寿命、更快的充电速度、更轻的重量和更低的维护需求,从而增强了市场的长期永续性,同时降低了整体拥有成本 (TCO) 并提高了营运效率。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 23亿美元 |

| 预测金额 | 51亿美元 |

| 复合年增长率 | 7.4% |

除了休閒用途外,高尔夫球车在商业和公共设施的应用也日益广泛,从而扩大了整体市场规模。其紧凑的尺寸、高机动性和低营运成本,促使各机构将其用于内部交通、商用旅行和轻型物流。这种转变正使高尔夫球车从纯粹的休閒车辆转变为支援各种业务功能的实用出行解决方案。

预计到2025年,电动车市占率将达到62%,并在2026年至2035年间以7.5%的复合年增长率成长。人们对零排放旅行和环保交通解决方案日益增长的兴趣正在推动电动车的普及。电动车符合永续性目标和环境认证要求,因为它们不会产生废气,并能显着降低噪音水平。这些优势正在增强住宅和商业领域的长期采购需求。

预计2025年,双座高尔夫球车市占率将达到57.4%,并在2026年至2035年间维持7.5%的复合年增长率。其紧凑的尺寸和便捷的操控性使其成为传统高尔夫球场运营的理想之选。轻量化的设计降低了对地面的衝击,提高了能源效率,为管理大规模车队的营运商带来了成本优势。持续的车辆更新换代和新车购买需求正在推动该细分市场在全球范围内的成长。

预计到2025年,美国高尔夫球车市场将占据87%的市场份额,市场规模将达到14亿美元。美国拥有庞大的高尔夫球场网络,这支撑了稳定的车辆需求。各个年龄层的高参与率也促进了稳定的购买和设备更换週期。持续的车辆现代化改造,包括向电动和锂离子电池驱动车型的升级,正在推动该地区製造商的长期收入成长。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 封闭社区和智慧城镇的扩张

- 高尔夫旅游和休閒活动的成长

- 电气化和锂离子电池的普及

- 在商业和公共设施中扩大使用

- 客製化和联网汽车功能

- 产业潜在风险与挑战

- 锂离子电池初始成本较高

- 对低速车辆的监管限制

- 电池处理及环境问题

- 与替代微型出行解决方案的竞争

- 市场机会

- 亚太地区旅游业的扩张

- 电动车的成长

- 车队租赁和出租模式

- 电池管理技术进步

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国环保署(EPA)

- 美国国家公路交通安全管理局 (NHTSA) - FMVSS 500

- 职业安全与健康管理局(OSHA)

- 加拿大车辆安全标准(CMVSS)

- 州级道路使用限制

- 欧洲

- 欧盟机械指令

- 符合CE标誌

- 低电压指令(LVD)

- 电磁相容性(EMC)指令

- 各国道路认证要求

- 亚太地区

- 中国电动车和轻型商用车法规结构

- 印度中央机动车辆法规(CMVR)

- 日本道路运输车辆法

- 东协协调电动车政策的努力

- 澳洲设计规则(ADR)

- 拉丁美洲

- 巴西国家交通委员会(CONTRAN)规章

- 墨西哥NOM标准

- 区域城市交通和电动车奖励计划

- 中东和非洲

- 海湾合作委员会车辆合规性和型式法规认证

- 南非道路交通法(NRTA)

- 旅游区和自由区的营运标准

- 北美洲

- 关键市场趋势与转型

- 未来市场趋势

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产基地

- 消费者群体

- 进出口

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估算与预测:依燃料类型划分,2022-2035年

- 汽油

- 电

- 太阳能

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 高尔夫球场

- 饭店和度假村

- 飞机场

- 住宅计划

- 其他的

第七章 市场估价与预测:依销售管道划分,2022-2035年

- 在线的

- 离线

第八章 市场估算与预测:依座位容量划分,2022-2035年

- 双座

- 四座

- 6座

- 其他的

第九章 市场估计与预测:依地区划分,2021-2034年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 波兰

- 荷兰

- 比利时

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚

- ANZ

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东和非洲(MEA)

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- 世界公司

- Club Car

- Columbia

- Cushman

- EZ-GO

- Garia

- Polaris

- Yamaha

- 当地公司

- Advanced EV

- Bintelli

- Evolution EV

- Melex

- Pilotcar

- Star EV

- Tomberlin

- 新兴企业

- Eco Planeta

- Guangdong Lvtong

- HDK

- Jinghang Sightseeing

- Langqing

- Marshell

- Suzhou Eagle

The Global Golf Cart Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 5.1 billion by 2035.

Market growth is supported by the rapid development of gated residential communities, retirement living projects, and planned smart townships that prioritize compact and low-speed mobility. Golf carts are increasingly integrated into controlled residential environments as a cost-effective and convenient transportation solution for short-distance travel. Urban development strategies that emphasize pedestrian-friendly layouts and low-emission transit options are further accelerating adoption. As a result, master-planned communities are incorporating dedicated pathways and charging infrastructure, creating steady replacement cycles and fleet expansion opportunities worldwide. In parallel, manufacturers are actively pursuing mergers, acquisitions, partnerships, and new product introductions to strengthen their competitive positioning. The ongoing transition toward lithium-ion battery systems and full electrification is reshaping the industry landscape. Compared to conventional battery technologies, lithium-ion solutions offer extended lifespan, faster charging, reduced weight, and lower maintenance requirements, improving overall ownership economics and operational efficiency while reinforcing long-term market sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 7.4% |

Beyond recreational applications, golf carts are witnessing rising deployment across commercial and institutional facilities, expanding the overall addressable market. Organizations are utilizing these vehicles for internal transportation, operational mobility, and light-duty logistics due to their compact structure, maneuverability, and low operating expenses. This shift is transforming golf carts from purely leisure-oriented vehicles into practical mobility solutions supporting diverse business functions.

The electric segment accounted for 62% share in 2025 and is anticipated to grow at a CAGR of 7.5% from 2026 to 2035. Growing emphasis on zero-emission mobility and environmentally responsible transportation solutions is driving adoption. Electric models eliminate tailpipe emissions and significantly reduce noise levels, aligning with sustainability objectives and environmental certification initiatives. These advantages are strengthening long-term procurement demand across residential and commercial settings.

The 2-seater segment held 57.4% share in 2025 and is expected to register a CAGR of 7.5% during 2026-2035. Their compact dimensions and ease of handling make them highly suitable for traditional golf course operations. Lightweight construction reduces surface impact and enhances energy efficiency, delivering cost advantages for operators managing large fleets. Continuous demand for replacement units and new purchases is supporting segment growth globally.

U.S. Golf Cart Market held an 87% share in 2025, generating USD 1.4 billion. The country benefits from an extensive network of golf facilities, sustaining consistent fleet demand. Strong participation rates across multiple age demographics contribute to steady procurement and equipment replacement cycles. Ongoing fleet modernization initiatives, including upgrades to electric and lithium-ion-powered models, are reinforcing long-term revenue growth for manufacturers operating in the region.

Key companies operating in the Global Golf Cart Market include Club Car, Yamaha, E-Z-GO, Cushman, Columbia, Marshell Green, Suzhou Eagle, Dongguan Excar, LANGQING, and Aoxiang. Companies in the Global Golf Cart Market are reinforcing their competitive strength through product innovation, battery technology advancements, and strategic partnerships. Manufacturers are investing in lithium-ion platforms, smart connectivity features, and improved vehicle design to enhance performance and user experience. Strategic alliances with residential developers and commercial operators are expanding distribution channels and long-term supply agreements. Many firms are introducing customized configurations tailored to specific end-user requirements, improving brand differentiation and customer loyalty. Geographic expansion and localized manufacturing initiatives are also being implemented to reduce production costs and strengthen regional presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel

- 2.2.3 Application

- 2.2.4 Sales channel

- 2.2.5 Seating capacity

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of gated communities and smart townships

- 3.2.1.2 Growth in golf tourism and leisure activities

- 3.2.1.3 Electrification and lithium-ion battery adoption

- 3.2.1.4 Increasing use in commercial & institutional facilities

- 3.2.1.5 Customization and connected vehicle features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront cost of lithium-ion models

- 3.2.2.2 Regulatory restrictions on low-speed vehicles

- 3.2.2.3 Battery disposal and environmental concerns

- 3.2.2.4 Competition from alternative micro-mobility solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Asia Pacific tourism sector

- 3.2.3.2 Growth of electric utility vehicles

- 3.2.3.3 Fleet leasing and rental models

- 3.2.3.4 Technological advancements in battery management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) - FMVSS 500

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.1.5 State-Level Road Use Regulations

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Directive

- 3.4.2.2 CE Marking Compliance

- 3.4.2.3 Low Voltage Directive (LVD)

- 3.4.2.4 Electromagnetic Compatibility (EMC) Directive

- 3.4.2.5 National Road Homologation Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese EV & LSV Regulatory Framework

- 3.4.3.2 Indian Central Motor Vehicle Rules (CMVR)

- 3.4.3.3 Japanese Road Transport Vehicle Act

- 3.4.3.4 ASEAN EV Policy Harmonization Efforts

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) Regulations

- 3.4.4.2 Mexican NOM Standards

- 3.4.4.3 Regional Urban Mobility & EV Incentive Programs

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Vehicle Compliance & Type Approval Regulations

- 3.4.5.2 South African National Road Traffic Act (NRTA)

- 3.4.5.3 Tourism & Free-Zone Operational Standards

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Electric

- 5.4 Solar-powered

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Golf Course

- 6.3 Hotels and Resorts

- 6.4 Airports

- 6.5 Housing Projects

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By Seating Capacity, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 2-Seater

- 8.3 4-Seater

- 8.4 6-Seater

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Southeast Asia

- 9.4.6 ANZ

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Club Car

- 10.1.2 Columbia

- 10.1.3 Cushman

- 10.1.4 E-Z-GO

- 10.1.5 Garia

- 10.1.6 Polaris

- 10.1.7 Yamaha

- 10.2 Regional Players

- 10.2.1 Advanced EV

- 10.2.2 Bintelli

- 10.2.3 Evolution EV

- 10.2.4 Melex

- 10.2.5 Pilotcar

- 10.2.6 Star EV

- 10.2.7 Tomberlin

- 10.3 Emerging Players

- 10.3.1 Eco Planeta

- 10.3.2 Guangdong Lvtong

- 10.3.3 HDK

- 10.3.4 Jinghang Sightseeing

- 10.3.5 Langqing

- 10.3.6 Marshell

- 10.3.7 Suzhou Eagle

高尔夫球车和社区型电动车市场:按车辆类型、电池电压、续航里程、速度等级、组件、应用和销售管道划分-2026-2032年全球市场预测高尔夫球车市场:2026-2032年全球市场预测(按产品类型、所有权、应用和产业划分)

高尔夫球车和社区型电动车市场:按车辆类型、电池电压、续航里程、速度等级、组件、应用和销售管道划分-2026-2032年全球市场预测高尔夫球车市场:2026-2032年全球市场预测(按产品类型、所有权、应用和产业划分) 2026年全球高尔夫球车及週边电动车(NEV)市场报告2026年全球高尔夫球车市场报告

2026年全球高尔夫球车及週边电动车(NEV)市场报告2026年全球高尔夫球车市场报告 全球高尔夫球车和新能源汽车市场规模、份额、趋势和成长分析报告(2026-2034年)

全球高尔夫球车和新能源汽车市场规模、份额、趋势和成长分析报告(2026-2034年) 高尔夫球车市场报告:按产品类型、应用、座位容量和地区划分(2026-2034 年)日本高尔夫球车市场报告(按产品类型、座位容量(小型、中型、大型)、应用和地区划分,2026-2034年)

高尔夫球车市场报告:按产品类型、应用、座位容量和地区划分(2026-2034 年)日本高尔夫球车市场报告(按产品类型、座位容量(小型、中型、大型)、应用和地区划分,2026-2034年) 高尔夫球车市场规模、份额和成长分析(按产品、座位数、销售管道和地区划分)-2026-2033年产业预测

高尔夫球车市场规模、份额和成长分析(按产品、座位数、销售管道和地区划分)-2026-2033年产业预测 电动高尔夫球童:全球市占率及排名、总销售量及需求预测(2025-2031年)花园推车市场按类型、尺寸、框架材料、机制、最终用途和分销管道划分 - 全球预测,2025-2030 年

电动高尔夫球童:全球市占率及排名、总销售量及需求预测(2025-2031年)花园推车市场按类型、尺寸、框架材料、机制、最终用途和分销管道划分 - 全球预测,2025-2030 年