|

市场调查报告书

商品编码

1982306

流动化学市场机会、成长要素、产业趋势分析及2026-2035年预测Flow Chemistry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

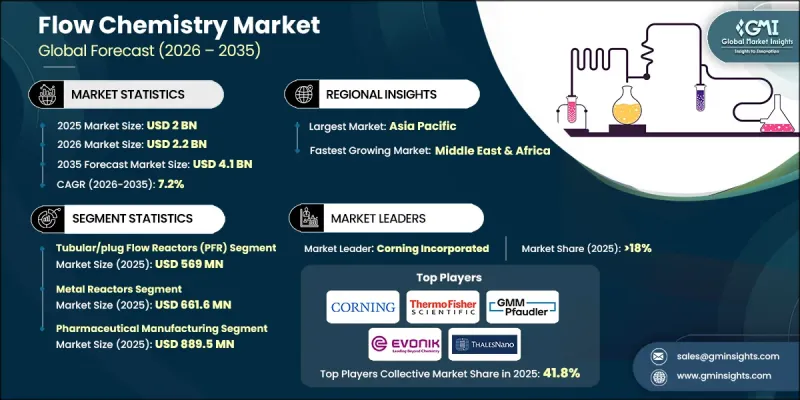

全球流动化学市场预计到 2025 年价值 20 亿美元,预计到 2035 年将以 7.2% 的复合年增长率增长至 41 亿美元。

製药业向连续生产的转型正显着推动市场扩张。美国FDA等监管机构积极推广连续生产工艺,因为它能够提高产品品质、增强过程控制并缩短生产前置作业时间。流动化学能够安全处理高活性中间体,同时支援即时监控,并符合品质源自于设计(QbD)原则和先进的製程优化。随着製药企业生产设施的现代化,对流动系统的需求持续成长。对永续和环保化学实践的日益重视进一步加速了流动技术的应用。与传统的间歇式生产相比,连续流动製程消耗的溶剂较少、产生的废弃物较少,通常所需的能源也较低。更严格的环境法规和全球永续性努力正迫使製造商转向更清洁的生产技术。流动化学透过实现更可控的反应并最大限度地减少对环境的影响,为实现这些目标提供了支持。微反应器工程和模组化流动平台的进步也透过提高扩充性、柔软性和操作响应能力,进一步巩固了市场地位。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 20亿美元 |

| 预测金额 | 41亿美元 |

| 复合年增长率 | 7.2% |

2025年,管式或活塞流反应器(PFR)市场规模将达5.69亿美元。反应器类型的细分反映了化学製程策略的明显转变,製造商力求在适应性、扩充性和运作性能之间取得平衡。间歇式反应器因其能够适应多种产品线并实现小规模规模生产的精确控制,仍保持较高的应用率。然而,化学技术的进步,以及日益严格的安全和环境法规,正迫使企业重新考虑传统的间歇式配置。这种转变在传热需求高和涉及危险中间体的製程中尤其明显,因为在这些製程中,连续性系统通常在可控性和安全性方面更具优势。

预计到2025年,金属反应器市场规模将达到6.616亿美元。随着业界采用针对特定化学应用和连续加工需求的客製化系统,反应器的选择也呈现出明显的专业化趋势。管式反应器、活塞流反应器(PFR)和连续搅拌釜式反应器(CSTR)因其运作可靠性和扩充性而仍然广受欢迎。在催化应用领域,填充床反应器和固定台反应器因其能够改善催化剂相互作用和提高整体反应效率,正日益受到业界的认可。同时,微结构反应器也因其紧凑的结构能够实现卓越的传热传质性能,从而支援高度可控和精确的合成工艺,而备受关注。

预计2025年,北美流动化学市场规模将达到2.995亿美元。这一区域市场的扩张主要得益于製药、特种化学品和生技产业对连续生产技术的日益普及。美国在区域市场中占据重要份额,这得益于其在工艺创新方面的巨额投资、先进合成技术的广泛应用以及强大的研究机构和合约开发与生产组织(CDMO)网络。製造商正越来越多地利用流动化学来提高反应效率、增强操作安全性并确保符合法规要求,尤其是在复杂和高风险的化学製程中。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 製药业连续生产製程的推广应用

- 大力推动绿色永续化学

- 微反应器和模组化系统的技术进步

- 产业潜在风险与挑战

- 大笔初始投资

- 与传统基础设施整合相关的挑战

- 市场机会

- 在光化学和电化学等新兴应用领域的拓展

- 对客製化、模组化和滑座式系统的需求日益增长

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计资料(HS编码)(註:仅提供主要国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依反应器类型划分,2022-2035年

- 管式/活塞流反应器(PFR)

- 微结构反应器

- 填充床/固定床反应器

- 连续搅拌釜式反应器(CSTR)

- 光化学流体反应器

- 电化学流动反应器

- 振盪流反应器(OFR)

- 混合和整合系统

- 其他的

第六章 市场估算与预测:依材料类型划分,2022-2035年

- 聚合物反应器

- 金属反应器

- 玻璃/石英反应器

- 陶瓷/硅反应器

- 其他材料

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 製药生产

- 精细化学品生产

- 石油化学加工

- 农药生产

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Thermo Fisher Scientific

- Xylem Inc.

- Alfa Laval AB

- SPX Technologies Inc.

- Sulzer Ltd.

- Corning Incorporated

- Syrris Ltd.

- Vapourtec Ltd.

- Chemtrix BV

- Evonik

- Zibo Taiji Industrial Enamel Co.,Ltd

- GMM Pfaudler

The Global Flow Chemistry Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 4.1 billion by 2035.

The rising shift toward continuous manufacturing in the pharmaceutical sector is significantly contributing to market expansion. Regulatory bodies such as the U.S. FDA actively encourage continuous processing due to its ability to improve product quality, enhance process control, and shorten production timelines. Flow chemistry enables the safe handling of highly reactive intermediates while supporting real-time monitoring, aligning with Quality by Design principles and advanced process optimization. As pharmaceutical manufacturers modernize production facilities, demand for flow-based systems continues to grow. Growing emphasis on sustainable and green chemistry practices is further accelerating adoption. Continuous flow processes consume less solvent, generate lower waste volumes, and typically require reduced energy compared to conventional batch operations. Increasing environmental regulations and global sustainability initiatives are encouraging manufacturers to transition toward cleaner production technologies. Flow chemistry supports these objectives by enabling more controlled reactions with minimized environmental impact. Advancements in microreactor engineering and modular flow platforms are also strengthening the market by improving scalability, flexibility, and operational responsiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 7.2% |

The tubular or plug flow reactors (PFR) segment reached USD 569 million in 2025. Segmentation by reactor type reflects a clear shift in chemical processing strategies, as manufacturers aim to balance adaptability, scalability, and operational performance. Batch reactors continue to maintain strong adoption due to their versatility in handling multiple product lines and enabling precise control in small- to mid-scale production. However, advancements in chemical engineering technologies, along with more rigorous safety and environmental regulations, are prompting companies to reassess traditional batch configurations. This transition is particularly evident in processes involving high heat transfer demands or hazardous intermediates, where continuous systems often provide enhanced control and safety advantages.

The metal reactors segment captured USD 661.6 million in 2025. Increasing specialization in reactor selection is evident as industries adopt systems tailored to specific chemical applications and continuous processing requirements. Tubular or plug flow reactors (PFR) and continuous stirred-tank reactors (CSTR) remain widely preferred due to their operational reliability and scalability. In catalytic applications, packed-bed and fixed-bed reactors are gaining stronger industry acceptance because they improve catalyst interaction and overall reaction efficiency. At the same time, microstructured reactors are drawing growing research attention, as their compact configurations enable superior heat and mass transfer performance, supporting highly controlled and precise synthesis processes.

North America Flow Chemistry Market generated USD 299.5 million in 2025. The region's expansion is driven by the growing implementation of continuous manufacturing across pharmaceuticals, specialty chemicals, and biotechnology sectors. The United States holds the dominant regional share, supported by significant investments in process innovation, widespread adoption of advanced synthesis technologies, and a strong network of research institutions and contract development and manufacturing organizations. Manufacturers are increasingly leveraging flow chemistry to improve reaction efficiency, enhance operational safety, and ensure regulatory compliance, particularly in complex and high-risk chemical processes.

Key participants in the Global Flow Chemistry Market include Evonik, Corning Incorporated, GMM Pfaudler, Thermo Fisher Scientific, Sulzer Ltd., Vapourtec Ltd., Zibo Taiji Industrial Enamel Co. Ltd, Syrris Ltd., SPX Technologies Inc., Chemtrix BV, Xylem Inc., and Alfa Laval AB. Companies operating in the Global Flow Chemistry Market are implementing strategic initiatives to strengthen their competitive positioning and expand their global footprint. Major players are investing in advanced reactor technologies, modular system design, and digital process integration to enhance efficiency and scalability. Strategic collaborations with pharmaceutical manufacturers and specialty chemical producers enable customized solutions and long-term supply agreements. Firms are also focusing on expanding production capabilities and regional distribution networks to improve market accessibility. Continuous investment in research and development supports innovation in microreactor platforms and automation technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Reactor Type

- 2.2.3 Material Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of continuous manufacturing in pharmaceuticals

- 3.2.1.2 Strong push for green and sustainable chemistry

- 3.2.1.3 Technological advancements in microreactors and modular systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Capital Investment

- 3.2.2.2 Integration Issues with Legacy Infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Emerging Applications like Photochemistry & Electrochemistry

- 3.2.3.2 Growing Demand for Custom, Modular, and Skid Mounted Systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Reactor Type, 2022 - 2035 (USD million) (Tons)

- 5.1 Key trends

- 5.2 Tubular/Plug Flow Reactors (PFR)

- 5.3 Microstructured Reactors

- 5.4 Packed-Bed/Fixed-Bed Reactors

- 5.5 Continuous Stirred-Tank Reactors (CSTR)

- 5.6 Photochemical Flow Reactors

- 5.7 Electrochemical Flow Reactors

- 5.8 Oscillatory Flow Reactors (OFR)

- 5.9 Hybrid & Integrated Systems

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD million) (Tons)

- 6.1 Key trends

- 6.2 Polymer-Based Reactors

- 6.3 Metal Reactors

- 6.4 Glass/Quartz Reactors

- 6.5 Ceramic/Silicon Reactors

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Tons)

- 7.1 Key trends

- 7.2 Pharmaceutical manufacturing

- 7.3 Fine chemicals production

- 7.4 Petrochemical processing

- 7.5 Agrochemical manufacturing

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Thermo Fisher Scientific

- 9.2 Xylem Inc.

- 9.3 Alfa Laval AB

- 9.4 SPX Technologies Inc.

- 9.5 Sulzer Ltd.

- 9.6 Corning Incorporated

- 9.7 Syrris Ltd.

- 9.8 Vapourtec Ltd.

- 9.9 Chemtrix BV

- 9.10 Evonik

- 9.11 Zibo Taiji Industrial Enamel Co.,Ltd

- 9.12 GMM Pfaudler

流动化学市场规模、份额、趋势和预测:按反应器、应用和地区划分,2026-2034 年

流动化学市场规模、份额、趋势和预测:按反应器、应用和地区划分,2026-2034 年 流动化学市场:依反应器类型、尺寸、应用和终端用户产业划分-2026-2032年全球市场预测工业规模製程光反应器市场:依反应器类型、运作模式、光源、应用和终端用户产业划分-全球预测,2026-2032年

流动化学市场:依反应器类型、尺寸、应用和终端用户产业划分-2026-2032年全球市场预测工业规模製程光反应器市场:依反应器类型、运作模式、光源、应用和终端用户产业划分-全球预测,2026-2032年 流动化学市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)

流动化学市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年) 全球流动化学品市场规模、份额、趋势和成长分析报告(2026-2034)

全球流动化学品市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球流动化学市场报告流动化学市场-2026-2031年预测

2026年全球流动化学市场报告流动化学市场-2026-2031年预测 微反应器技术市场规模、份额和成长分析(按类型、产品类型、混合方法、应用、最终用户和地区划分)—2026-2033年产业预测

微反应器技术市场规模、份额和成长分析(按类型、产品类型、混合方法、应用、最终用户和地区划分)—2026-2033年产业预测 流动化学市场规模、份额和成长分析(按反应器类型、应用、纯化方法和地区划分)—产业预测(2026-2033 年)微反应器技术市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)

流动化学市场规模、份额和成长分析(按反应器类型、应用、纯化方法和地区划分)—产业预测(2026-2033 年)微反应器技术市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)