|

市场调查报告书

商品编码

1982309

空间通讯市场机会、成长要素、产业趋势分析及2026-2035年预测。Sky-based Communication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

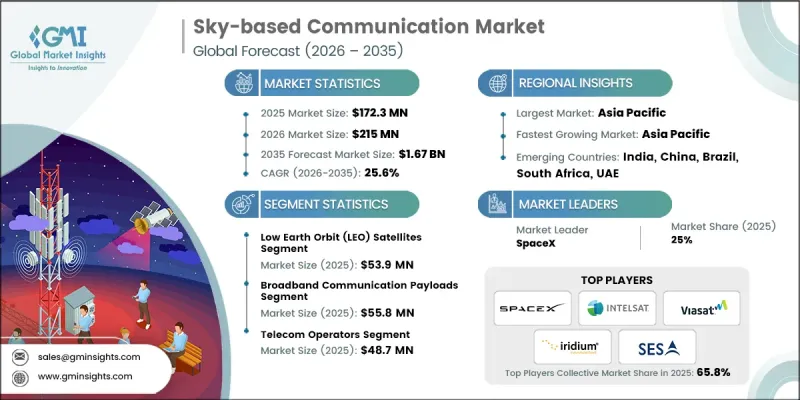

全球卫星通讯市场预计到 2025 年将价值 1.723 亿美元,预计到 2035 年将达到 16.7 亿美元,年复合成长率为 25.6%。

市场成长的驱动力来自对卫星宽频连接日益增长的需求、低地球轨道卫星星系的快速部署、不断扩大的国防和安全通讯需求,以及航空航太和海事领域应用的不断增加。 5G框架与非地面网路的整合进一步强化了卫星基础设施在下一代连结中的作用。随着全球弥合数位落差的努力活性化,卫星系统正成为向地面网路覆盖有限的偏远和地理环境恶劣地区提供宽频存取的切实可行的解决方案。由于其广域覆盖、快速部署和网路弹性,空间通讯平台正成为商业和策略应用领域越来越有吸引力的选择。推动全民数位包容,加上数据消耗量的成长和行动需求的增加,正在加速全球空间通讯生态系统的长期投资。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 1.723亿美元 |

| 预测金额 | 16.7亿美元 |

| 复合年增长率 | 25.6% |

数位公共服务、远端教育平台、远端医疗解决方案的扩展以及安全通讯框架的现代化,都日益依赖可靠的卫星宽频基础设施。公共部门的投资、对频率分配的支持以及国家互联互通倡议,都提升了卫星通讯网路的商业性和战略意义。低地球轨道(LEO)卫星星系的快速部署,凭藉其相比传统卫星架构更低的延迟和更高的频宽,正在重塑竞争格局。各国政府正支持将低地球轨道卫星融入国家网络,以增强通讯容错能力、提高资料安全性并加强冗余性,从而进一步拓展太空通讯市场。

预计2025年,低地球轨道(LEO)卫星市场规模将达5,390万美元。 LEO卫星提供低延迟、高吞吐量的连接,使其成为即时宽频服务、物联网连接和直接设备通讯解决方案的理想选择。公共和私营营运商加速部署大规模卫星群,扩大了全球覆盖范围,并提高了服务的连续性。为了保持竞争力,製造商正致力于开发模组化和扩充性的卫星平台、先进的卫星群管理系统以及高效能通讯有效载荷,以满足不断发展的宽频和安全通讯需求。

预计到2025年,宽频通讯酬载市场规模将达到5,580万美元。这些有效载荷将支援高容量、低延迟的互联网服务,适用于企业网路、工业IoT、航空通讯、海事通讯和政府应用。对高速资料传输、云端服务和先进数位应用日益增长的需求,正促使营运商在多种轨道配置下部署增强型有效载荷技术,从而强化整个卫星宽频生态系统。

到2025年,北美卫星通讯市场占有率将达到28.6%。该地区透过对卫星宽频基础设施、安全通讯系统和先进地面网路能力的巨额投资,保持着主导地位。发射能力的持续提升和多样化卫星星系的整合,正在扩大服务欠缺地区的通讯覆盖范围。不断完善的监管法规、公私合营以及政府主导的资金筹措倡议,持续加速商业化进程,同时增强民用和国防领域的安全通讯能力。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 基于卫星的宽频连线的需求日益增长

- 低地球轨道(LEO)卫星星系的扩展

- 对国防和安全通讯的需求日益增长

- 航空和航运领域的应用扩展

- 5G与非地面电波网路(NTN)的融合

- 陷阱与挑战

- 高昂的部署和基础设施成本

- 讯号延迟和太空碎片风险

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新经营模式

- 合规要求

- 供应链韧性

- 国防预算分析

- 全球国防费用趋势

- 区域国防预算分配

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 主要国防现代化项目

- 预算预测(2025-2034 年)

- 对产业成长的影响

- 国防预算

- 分段式国防预算分配

- 人员

- 运作/维护

- 采购

- 研究、开发、测试和评估

- 基础设施和建筑

- 技术与创新

- 永续发展倡议

- 供应链韧性

- 地缘政治分析

- 劳动力分析

- 数位转型

- 併购和策略联盟的趋势

- 风险评估与管理

- 重大合约授予情况(2022-2025 年)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域部署对比

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 伙伴关係和联盟

- 技术进步

- 业务拓展与投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依平台划分,2022-2035年

- 高空平台系统(HAPS)

- 近空间平台(NSP)

- 低地球轨道(LEO)卫星

- 中轨道(MEO)卫星

- 地球静止轨道(GEO)卫星

第六章 市场估算与预测:酬载类型,2022-2035年

- 宽频通讯有效载荷

- 窄频/物联网酬载

- 行动回程有效载荷

- 设备到设备 (D2D) 有效载荷

- 广播有效载荷(电视/广播)

- 军用安全通讯有效载荷

第七章 市场估计与预测:依最终用户产业划分,2022-2035年

- 通讯业者

- 航空业

- 航运业

- 国防/国防安全保障

- 政府机构

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- SpaceX

- Intelsat

- SES SA

- Inmarsat

- Viasat

- 按地区分類的主要企业

- 北美洲

- L3Harris Technologies

- Honeywell International

- EchoStar

- AST SpaceMobile

- Maxar Technologies

- 欧洲

- Eutelsat OneWeb

- Thales Group

- Airbus

- 亚太地区

- Telesat

- 北美洲

- 小众/颠覆者

- Iridium Communications

The Global Sky-based Communication Market was valued at USD 172.3 million in 2025 and is estimated to grow at a CAGR of 25.6% to reach USD 1.67 billion by 2035.

Market growth is fueled by rising demand for satellite-enabled broadband connectivity, rapid deployment of low earth orbit constellations, growing defense and secure communication needs, and expanding adoption across aviation and maritime sectors. The integration of 5G frameworks with non-terrestrial networks is further strengthening the role of satellite infrastructure in next-generation connectivity. As global efforts intensify to bridge the digital divide, satellite-based systems are emerging as a practical solution for delivering broadband access to remote and geographically challenging areas where terrestrial networks remain limited. Sky-based communication platforms offer wide-area coverage, rapid deployment, and network resilience, making them increasingly attractive for both commercial and strategic applications. The push toward universal digital inclusion, combined with rising data consumption and mobility requirements, is accelerating long-term investment across the global sky-based communication ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $172.3 Million |

| Forecast Value | $1.67 Billion |

| CAGR | 25.6% |

Expanding digital public services, remote education platforms, telehealth solutions, and modernization of secure communication frameworks are increasing reliance on dependable satellite broadband infrastructure. Public sector investment, spectrum allocation support, and national connectivity initiatives are strengthening the commercial and strategic case for satellite communication networks. The rapid rollout of low-earth-orbit satellite constellations is reshaping the competitive landscape by delivering lower latency and higher bandwidth compared to traditional satellite architectures. Governments are supporting LEO integration to enhance communication resilience, improve data security, and reinforce national network redundancy, driving further expansion of the sky-based communication market.

The low earth orbit satellites segment generated USD 53.9 million in 2025. LEO satellites provide low-latency and high-throughput connectivity, making them well-suited for real-time broadband services, IoT connectivity, and direct-to-device communication solutions. Accelerated deployment of large-scale constellations by public and private operators is expanding global coverage and improving service continuity. To remain competitive, manufacturers are focusing on modular and scalable satellite platforms, advanced constellation management systems, and high-performance communication payloads designed to support evolving broadband and secure communication requirements.

The broadband communication payloads segment reached USD 55.8 million in 2025. These payloads enable high-capacity, low-latency internet services that support enterprise networks, industrial IoT, aviation connectivity, maritime communication, and government applications. Rising demand for high-speed data transfer, cloud-based services, and advanced digital applications is encouraging operators to deploy enhanced payload technologies across multiple orbital configurations, strengthening the overall satellite broadband ecosystem.

North America Sky-based Communication Market accounted for 28.6% share in 2025. The region maintains a leadership position due to significant investments in satellite broadband infrastructure, secure communication systems, and advanced ground network capabilities. Ongoing expansion of launch capacity and integration of diverse satellite constellations are increasing connectivity coverage across underserved areas. Regulatory evolution, public-private collaboration, and government-backed funding initiatives continue to accelerate commercialization while reinforcing secure communication capabilities for both civilian and defense sectors.

Key companies operating in the Global Sky-based Communication Market include SpaceX, Viasat, SES S.A., Eutelsat, OneWeb, Intelsat, Inmarsat, Iridium Communications, Telesat, AST Space Mobile, Airbus, Thales Group, L3Harris Technologies, Honeywell International, Maxar Technologies, and EchoStar. Companies in the Global Sky-based Communication Market are strengthening their market position through constellation expansion, strategic partnerships, and vertical integration. Leading players are investing in next-generation satellite platforms, reusable launch technologies, and advanced payload innovation to improve bandwidth efficiency and reduce latency. Collaboration with telecom operators and government agencies enables integration with 5G and non-terrestrial networks, expanding service reach. Firms are also focusing on software-defined satellites, network management solutions, and secure encryption technologies to enhance service reliability and defense-grade communication.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Platform layer trends

- 2.2.2 Payload type trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for satellite-based broadband connectivity

- 3.2.1.2 Expansion of low earth orbit (LEO) satellite constellations

- 3.2.1.3 Growing defense and secure communication requirements

- 3.2.1.4 Increasing adoption in aviation and maritime connectivity

- 3.2.1.5 Integration of 5G and non-terrestrial networks (NTN)

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High deployment and infrastructure costs

- 3.2.2.2 Signal latency and space debris risks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Defense Budget Analysis

- 3.12 Global Defense Spending Trends

- 3.13 Regional Defense Budget Allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key Defense Modernization Programs

- 3.15 Budget Forecast (2025-2034)

- 3.15.1 Impact on Industry Growth

- 3.15.2 Defense Budgets by Country

- 3.15.3 Defense Budget Allocation by Segment

- 3.15.3.1 Personnel

- 3.15.3.2 Operations and Maintenance

- 3.15.3.3 Procurement

- 3.15.3.4 Research, Development, Test and Evaluation

- 3.15.3.5 Infrastructure and Construction

- 3.15.3.6 Technology and Innovation

- 3.16 Sustainability Initiatives

- 3.17 Supply Chain Resilience

- 3.18 Geopolitical Analysis

- 3.19 Workforce Analysis

- 3.20 Digital Transformation

- 3.21 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.22 Risk Assessment and Management

- 3.23 Major Contract Awards (2022-2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Layer, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 High Altitude Platform Systems (HAPS)

- 5.3 Near-Space Platforms (NSP)

- 5.4 Low Earth Orbit (LEO) Satellites

- 5.5 Medium Earth Orbit (MEO) Satellites

- 5.6 Geostationary Orbit (GEO) Satellites

Chapter 6 Market Estimates and Forecast, By Payload Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Broadband Communication Payloads

- 6.3 Narrowband / IoT Payloads

- 6.4 Mobile Backhaul Payloads

- 6.5 Direct-to-Device (D2D) Payloads

- 6.6 Broadcast Payloads (TV/Radio)

- 6.7 Military Secure Communication Payloads

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Telecom Operators

- 7.3 Aviation Industry

- 7.4 Maritime Industry

- 7.5 Defense & Homeland Security

- 7.6 Government Agencies

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 SpaceX

- 9.1.2 Intelsat

- 9.1.3 SES S.A.

- 9.1.4 Inmarsat

- 9.1.5 Viasat

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 L3Harris Technologies

- 9.2.1.2 Honeywell International

- 9.2.1.3 EchoStar

- 9.2.1.4 AST SpaceMobile

- 9.2.1.5 Maxar Technologies

- 9.2.2 Europe

- 9.2.2.1 Eutelsat OneWeb

- 9.2.2.2 Thales Group

- 9.2.2.3 Airbus

- 9.2.3 Asia Pacific

- 9.2.3.1 Telesat

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Iridium Communications