|

市场调查报告书

商品编码

1982317

液封真空帮浦市场:成长机会、成长要素、产业趋势分析及2026-2035年预测。Liquid Ring Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

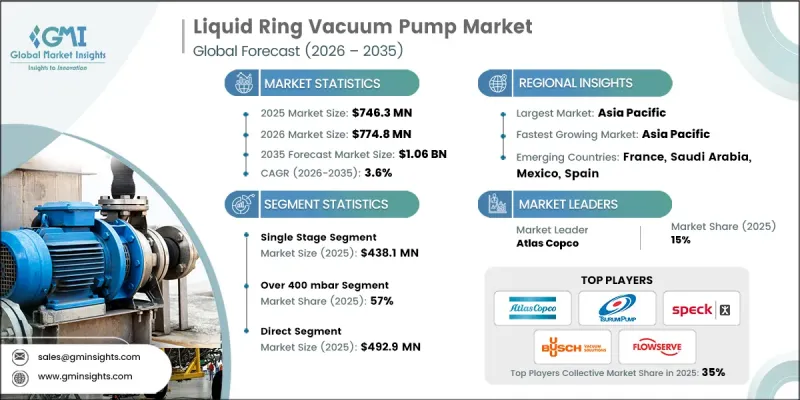

预计到 2025 年,全球液封真空帮浦市场规模将达到 7.463 亿美元,年复合成长率为 3.6%,预计到 2035 年将达到 10.6 亿美元。

液封真空帮浦的需求主要来自核心製程工业,这些产业对处理潮湿、饱和或受污染气体至关重要。化学、製药、食品饮料、石油天然气以及纸浆造纸等行业越来越依赖即使在製程条件波动的情况下也能稳定可靠运作的真空系统。随着产能的提升和现有系统的现代化改造,製造商优先考虑那些能够确保运作稳定性、低维护成本和抗污染性的真空解决方案。液封真空帮浦尤其适用于蒸馏、溶剂回收、真空干燥、过滤和脱气等应用,并且已成为许多工业製程中不可或缺的设备。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 7.463亿美元 |

| 预测金额 | 10.6亿美元 |

| 复合年增长率 | 3.6% |

对能够长期稳定运作且维护成本低的真空帮浦的需求日益增长,进一步推动了连续加工和自动化的发展。液环泵结构简单,对异物、液体和腐蚀性蒸气具有很高的耐受性,是生产含固体或水分气体的设备的理想选择。其可靠性和操作柔软性可最大限度地减少停机时间,尤其是在严苛的工业环境中。

到2025年,单级泵浦市场规模将达到4.381亿美元。单级液封真空帮浦采用单级压缩结构,其叶轮在部分充液的泵浦壳内偏心旋转,形成稳定的液环,从而平稳地压缩气体。此设计可实现无脉动运行,并能安全处理潮湿、饱和或受污染的气体,使其适用于工况波动较大且湿度较高的製程环境。

到2025年,泵压超过400毫巴的泵浦将占57%的市场。这些帮浦即使在工况波动的情况下也能保持稳定的吸力,因此非常适合处理高湿度气体或大颗粒气体等无需极高真空的应用。其高泵压性能使其能够有效地进行蒸气处理、真空脱气、过滤器支撑和流体输送,而无需产生极低的绝对压力。

预计到2025年,美国液封真空帮浦市占率将达到82.9%,市场规模将达到1.584亿美元。强大的工业基础,以及化学、製药、食品加工和能源等行业对真空技术的高需求,正在推动液封真空帮浦的需求成长。液封真空帮浦能够处理饱和气体、波动负载和恶劣的运作条件,符合美国对运作安全、製程稳定性和环境法规合规性的要求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 流程工业的需求不断成长

- 人们越来越关注环境合规性

- 工业化和自动化流程

- 产业潜在风险与挑战

- 有限真空

- 高用水量

- 机会

- 两级LRVP设计的进展

- 以永续发展主导的创新

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 单级

- 两阶段

第六章 市场估计与预测:依材料划分,2022-2035年

- 铸铁

- 不銹钢

- 其他的

第七章 市场估计与预测:依产能划分,2022-2035年

- 200毫巴或更低

- 200~400 mbar

- 超过400毫巴

第八章 市场估算与预测:依交通量划分,2022-2035年

- 25~600 m3/h

- 600~3000 m3/h

- 3,000~10,000 m3/h

- 超过10,000立方米

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 石油化工/化工

- 製药

- 食品製造

- 飞机

- 车

- 水处理

- 石油和天然气

- 发电

- EPS和塑料

- 纸浆和造纸

- 其他的

第十章 市场估价与预测:依通路划分,2022-2035年

- 直接地

- 间接

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- Atlas Copco

- Busch Vacuum Solutions

- Cutes

- Dekker Vacuum

- Finder

- Flowserve

- Graham Engineering

- Ingersoll Rand

- Omel

- PPI Pumps

- Samson

- Speck Pumpen

- Tsurumi

- Vooner

- Zibo Zhaohan

The Global Liquid Ring Vacuum Pump Market was valued at USD 746.3 million in 2025 and is estimated to grow at a CAGR of 3.6% to reach USD 1.06 billion by 2035.

Demand for liquid ring vacuum pumps is primarily driven by core process industries, where handling wet, saturated, or contaminated gases is essential. Industries such as chemicals, pharmaceuticals, food and beverage, oil and gas, and pulp and paper rely heavily on vacuum systems that provide stable, reliable operation under variable process conditions. As production capacity increases and existing systems are modernized, manufacturers are prioritizing vacuum solutions that ensure operational stability, low maintenance, and resilience to contamination. Liquid ring pumps are particularly suitable for applications like distillation, solvent recovery, vacuum drying, filtering, and degassing, making them indispensable for many industrial processes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $746.3 Million |

| Forecast Value | $1.06 Billion |

| CAGR | 3.6% |

The adoption of continuous processing and automation further supports the need for vacuum pumps capable of extended, low-maintenance operation. Liquid ring pumps, with their simple mechanical design and high tolerance for debris, liquids, and corrosive vapors, are ideal for facilities producing gas streams containing solids or moisture. Their reliability and operational flexibility ensure minimal downtime, particularly in demanding industrial environments.

In 2025, the single-stage pumps segment reached USD 438.1 million. Single-stage liquid ring vacuum pumps feature a single compression stage with an impeller rotating eccentrically within a partially liquid-filled casing, forming a stable liquid ring that compresses gas smoothly. This design delivers pulsation-free operation while safely handling wet, saturated, or contaminated gases, making them suitable for processes with variable conditions or high moisture content.

The pumps with discharge capabilities above 400 mbar segment held 57% share in 2025. These pumps maintain steady suction under varying conditions, making them ideal for applications involving high-moisture gases or large particles, where deep vacuum is unnecessary. Their performance at higher discharge pressures allows them to efficiently handle vapors, vacuum degassing, filter support, and fluid transfer without creating extremely low absolute pressure.

U.S. Liquid Ring Vacuum Pump Market accounted for 82.9% share in 2025, generating USD 158.4 million. The strong industrial framework, coupled with significant vacuum technology requirements across chemical, pharmaceutical, food processing, and energy sectors, supports demand for liquid ring vacuum pumps. Their ability to manage saturated gases, variable loads, and extreme operating conditions aligns with the U.S. focus on operational safety, process stability, and environmental compliance.

Key players in the Global Liquid Ring Vacuum Pump Market include Atlas Copco, Dekker Vacuum, Ingersoll Rand, Flowserve, Tsurumi, Samson, Graham Engineering, Vooner, Omel, Speck Pumpen, PPI Pumps, Busch Vacuum Solutions, Finder, Cutes, and Zibo Zhaohan. Companies in the Liquid Ring Vacuum Pump Market are pursuing multiple strategies to strengthen their presence and market foothold. These include expanding manufacturing capacities, developing advanced, energy-efficient, and corrosion-resistant models, and investing in R&D to enhance performance under variable process conditions. Strategic collaborations with end-user industries and after-sales service networks improve market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Capacity

- 2.2.5 Flow rate

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand from process industries

- 3.2.1.2 Growing focus on environmental compliance

- 3.2.1.3 Rising industrialization and automation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Limited vacuum depth

- 3.2.2.2 High water consumption

- 3.2.3 Opportunities

- 3.2.3.1 Advancements in two-stage LRVP designs

- 3.2.3.2 Sustainability-driven innovations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million) (Million Units)

- 5.1 Key trends

- 5.2 Single stage

- 5.3 Two stages

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million) (Million Units)

- 6.1 Key trends

- 6.2 Cast iron

- 6.3 Stainless steel

- 6.4 Other

Chapter 7 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million) (Million Units)

- 7.1 Key trends

- 7.2 Up to 200 mbar

- 7.3 200 to 400 mbar

- 7.4 Over 400 mbar

Chapter 8 Market Estimates and Forecast, By Flow Rate, 2022 - 2035 (USD Million) (Million Units)

- 8.1 Key trends

- 8.2 25 - 600 M3H

- 8.3 600 - 3000 M3H

- 8.4 3000 - 10000 M3H

- 8.5 Over 10000 M3

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Million Units)

- 9.1 Key trends

- 9.2 Petrochemical & chemical

- 9.3 Pharmaceutical

- 9.4 Food manufacturing

- 9.5 Aircraft

- 9.6 Automobile

- 9.7 Water treatment

- 9.8 Oil & gas

- 9.9 Power generation

- 9.10 EPS and plastics

- 9.11 Pulp & paper

- 9.12 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Million Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Atlas Copco

- 12.2 Busch Vacuum Solutions

- 12.3 Cutes

- 12.4 Dekker Vacuum

- 12.5 Finder

- 12.6 Flowserve

- 12.7 Graham Engineering

- 12.8 Ingersoll Rand

- 12.9 Omel

- 12.10 PPI Pumps

- 12.11 Samson

- 12.12 Speck Pumpen

- 12.13 Tsurumi

- 12.14 Vooner

- 12.15 Zibo Zhaohan