|

市场调查报告书

商品编码

1982321

男性女乳症手术市场:成长机会、成长要素、产业趋势分析及2026-2035年预测Gynecomastia Procedures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

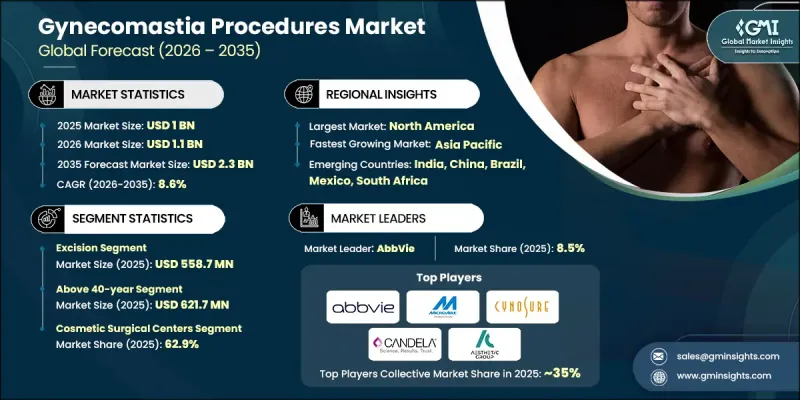

全球男性女乳症手术市场预计到 2025 年价值 10 亿美元,预计到 2035 年将以 8.6% 的复合年增长率增长至 23 亿美元。

市场成长动能主要受肥胖率上升、男性荷尔蒙失衡问题日益严重、外科手术技术持续创新所驱动。体脂率升高与内分泌失调密切相关,而雌激素活性升高(尤其是脂肪组织代谢引起的雌激素活性升高)会显着增加男性女乳症的发生率。此外,胸部脂肪过度堆积往往是促使患者寻求矫正手术以改善医疗和美容效果的因素之一。肥胖负担日益加重,加上公众意识的提高、诊断率的提升以及社会对男性整形手术的接受度不断提高,正推动着全球范围内持续增长的手术需求。微创技术的进步和手术精准度的提升进一步增强了患者的信心,并在主要市场建立了长期治疗模式。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 10亿美元 |

| 预测金额 | 23亿美元 |

| 复合年增长率 | 8.6% |

按手术类型划分,市场可分为抽脂术和切除术,其中切除术预计到2025年将创造5.587亿美元的市场规模,占据相当大的市场份额。切除术是指透过精心设计的切口精确切除乳房组织,对于仅靠消脂无法解决的緻密乳房组织,此方法能够有效矫正。此方法可获得可靠的塑形效果,尤其适用于中度至重度病例。其临床疗效和永久性切除组织的能力正推动着该技术在外科手术领域的持续发展。

以最终用户划分,预计2025年,整形外科中心将占据62.9%的市场。这些机构专门提供选择性的整形手术,拥有专业知识、先进设备和经验丰富的手术团队,专注于男性乳房缩小手术。其高效的运作使其能够接纳更多患者并确保治疗效果的稳定性。与医院相比,整形外科中心通常提供更短的等待时间、更具竞争力的价格和更精简的医疗服务模式。这些优点对自费患者极具吸引力,而自费患者正是寻求男性女乳症矫正手术的大多数患者。

从区域来看,预计到2025年,北美将占据全球男性女乳症手术市场的40.5%以上。美国市场的成长主要得益于高肥胖率以及人们对男性女乳症作为一种可治疗的医疗和美容问题的认识不断提高。教育的普及、咨询管道的增加以及数位化医疗的广泛应用,都鼓励了更多男性寻求专业治疗。人们对男性健康和外表观念的转变,也持续推动着全部区域。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 肥胖症盛行率上升

- 越来越多的男性患有荷尔蒙失衡症。

- 科技的快速发展

- 人们对男性女乳症的认识不断提高

- 产业潜在风险与挑战

- 治疗费用高昂

- 保险不涵盖的情况

- 市场机会

- 对微创手术的需求日益增长

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 科技趋势

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略仪錶板

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依治疗类型划分,2022-2035年

- 抽脂手术

- 切除

第六章 市场估计与预测:依年龄组别划分,2022-2035年

- 18-40岁

- 40岁以上

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 整形外科中心

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- MicroAire Surgical Instruments

- Lumenis

- Aesthetic Group

- Candela Corporation

- Johnson &Johnson

- Cutera

- Cynosure(Hologic, Inc.)

- AbbVie Inc.

- Solta Medical

- Sientra

The Global Gynecomastia Procedures Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 2.3 billion by 2035.

Market momentum is supported by the growing incidence of obesity, a rising population of men experiencing hormonal irregularities, and continuous technological innovation in surgical techniques. Higher body fat levels are closely linked to endocrine disruption, particularly elevated estrogen activity resulting from adipose tissue metabolism, which significantly increases the likelihood of gynecomastia. In addition, excess fat accumulation in the chest region often leads patients to pursue corrective procedures for both medical and aesthetic improvement. The expanding burden of obesity, combined with greater awareness, improved diagnosis rates, and broader social acceptance of male aesthetic procedures, is translating into sustained procedural demand worldwide. Advancements in minimally invasive technologies and enhanced surgical precision are further strengthening patient confidence and long-term treatment adoption across key markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 8.6% |

By procedure type, the market is categorized into liposuction and excision, with the excision segment generating USD 558.7 million in 2025 and accounting for a substantial share. Excision procedures involve the precise removal of glandular breast tissue through carefully placed incisions, enabling effective correction in cases where dense tissue cannot be addressed through fat removal techniques alone. This method provides reliable contouring outcomes and is particularly suited for moderate to advanced presentations. Its clinical effectiveness and ability to deliver permanent tissue removal continue to drive adoption across surgical practices.

In terms of end use, the cosmetic surgical centers segment captured 62.9% share in 2025. These facilities are specifically structured to deliver elective aesthetic procedures, offering specialized expertise, advanced equipment, and experienced surgical teams focused on male breast reduction treatments. Their operational efficiency supports higher patient throughput and consistent results. Compared to hospital settings, cosmetic surgical centers generally provide shorter scheduling timelines, competitive pricing structures, and streamlined care delivery models. These advantages strongly appeal to self-funded patients, who represent a significant portion of individuals seeking gynecomastia correction.

Regionally, North America accounted for more than 40.5% of the global gynecomastia procedures industry share in 2025. Growth across the U.S. market is largely fueled by the high prevalence of obesity and increasing recognition of gynecomastia as a manageable medical and cosmetic concern. Broader education initiatives, expanded consultation access, and digital health engagement have encouraged more men to pursue professional treatment. Evolving perceptions surrounding male wellness and physical appearance continue to support procedural uptake throughout the region.

Key companies active in the Global Gynecomastia Procedures Market include Johnson & Johnson, AbbVie Inc., Candela Corporation, Cutera, Lumenis, Cynosure, Solta Medical, Sientra, MicroAire Surgical Instruments, and Aesthetic Group. Companies operating in the Gynecomastia Procedures Market are strengthening their competitive position through innovation, portfolio expansion, and strategic collaborations. Leading players are investing heavily in advanced surgical technologies that improve precision, reduce recovery time, and enhance patient outcomes. Many firms are broadening their aesthetic device portfolios to address evolving clinical preferences and surgeon demand. Partnerships with cosmetic surgical centers and specialty clinics are helping manufacturers expand distribution networks and increase product visibility. Organizations are also prioritizing physician training programs and hands-on workshops to build brand loyalty and encourage product adoption. In addition, mergers, acquisitions, and geographic expansion strategies are being implemented to reinforce global presence and capture emerging growth opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Procedure type trends

- 2.2.2 Age group trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of obesity

- 3.2.1.2 Rising number of men affected by hormonal imbalances

- 3.2.1.3 Upsurge in technological advancements

- 3.2.1.4 Increasing awareness regarding gynecomastia

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of procedures

- 3.2.2.2 Lack of reimbursement scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for minimally invasive procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Procedure Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Liposuction

- 5.3 Excision

Chapter 6 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 18-40 years

- 6.3 Above 40 years

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cosmetic surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.4 Italy

- 8.3.5 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 MicroAire Surgical Instruments

- 9.2 Lumenis

- 9.3 Aesthetic Group

- 9.4 Candela Corporation

- 9.5 Johnson & Johnson

- 9.6 Cutera

- 9.7 Cynosure (Hologic, Inc.)

- 9.8 AbbVie Inc.

- 9.9 Solta Medical

- 9.10 Sientra