|

市场调查报告书

商品编码

1982322

汽车电动驱动系统组件的市场机会、成长要素、产业趋势分析及 2026-2035 年预测。Automotive Electric Drivetrain Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

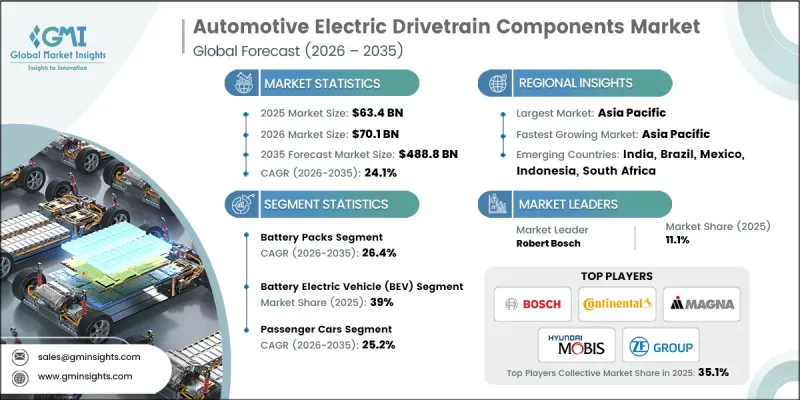

2025 年全球汽车电动传动系统零件市场规模预计为 634 亿美元,预计到 2035 年将达到 4,888 亿美元,年复合成长率为 24.1%。

汽车产业整体的快速电气化正在加速对先进电动驱动系统的需求。日益严格的全球排放气体法规迫使汽车製造商加快向电动车(EV)平台转型。这些监管压力正推动电驱动系统、逆变器、电力电子设备和整合式电动推进模组的产量大幅成长。锂离子电池製造成本的持续降低和生产效率的提高,进一步改变了汽车定价结构,并增强了电动车的竞争力。随着电池成本的下降,製造商正在扩大轻量化马达和高效能逆变器系统的生产规模,以满足不断增长的全球需求。动力传动系统的进步也在提升续航里程、充电相容性和整体系统性能,从而促进电动车的广泛普及。汽车製造商正在将智慧电桥、互联控制模组和先进的诊断功能整合到电力传动系统架构中,以优化即时监控和能量管理。法规要求、电池成本的下降以及以性能主导的创新,共同推动了电力传动系统零件在全球汽车产业核心成长引擎中的地位日益提升。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 634亿美元 |

| 预计金额 | 4888亿美元 |

| 复合年增长率 | 24.1% |

预计到2025年,电池组市占率将达到26%,并在2026年至2035年间以26.4%的复合年增长率成长。能量密度、电池管理系统和新一代电芯化学技术的持续进步正在提升续航里程和行车安全。业界关注的重点仍然是快速充电能力、更高的耐用性和成本优化。新兴电池技术和不断发展的材料成分预计将在整个预测期内进一步提升性能标准和生产规模。

预计到2025年,乘用车市占率将达到65%,并在2026年至2035年间以25.2%的复合年增长率成长。排放气体目标和对效率提升的追求正在推动乘用车领域电气化的扩张。汽车製造商正在引入轻量化动力总成模组、模组化架构和高容量电池系统,以优化续航里程和联网汽车。消费者正受益于不断扩展的充电网路和政府的支持措施,这些措施正在加速都市区和郊区的普及。现代电动搭乘用融合了再生煞车、即时能量优化和车联网系统等整合技术,而所有这些技术都依赖先进的电动动力总成零件。

预计到2025年,北美汽车电动传动系统零件市场规模将达172亿美元。各主要市场为统一电动车标准所做的区域性努力,正在缓解跨境供应限制,并推动传动系统的大规模生产。供应商之间的产业合作正在加速下一代电驱动桥技术和整合推进平台的研发。同时,2025年充电基础设施的持续扩张正在增强消费者信心,并进一步刺激对电动传动系统零件的需求。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 电动车的快速普及和电气化进程的推进

- 严格的排放法规和政府政策

- 更低的电池成本和更高的技术性能

- 扩大电动车充电基础设施

- 产业潜在风险与挑战

- 高昂的生产成本和零件成本

- 供应链脆弱性与原料供应限制

- 市场机会

- 先进的电力电子和轻量化模组设计

- 新兴和发展中市场

- 永续性和回收解决方案

- 合作伙伴关係和跨行业伙伴关係

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 汽车创新联盟

- 汽车工业行动小组

- 欧洲

- 欧洲汽车製造商协会

- 联合国欧洲经济委员会(UNECE)世界机动车法规协调论坛(WP.29)

- 亚太地区

- 亚太经合组织汽车对话

- 东协汽车联盟

- 拉丁美洲

- 墨西哥电动车推广协会

- 巴西电动车协会

- 中东和非洲

- 波湾合作理事会标准化组织

- 南非标准局

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析

- 产品特定定价

- 区域定价

- 生产统计

- 生产基地

- 消费者群体

- 出口和进口

- 成本細項分析

- 供应商成本结构

- 成本构成要素的应用

- 持续营运成本

- 客户间接费用

- 专利分析

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 关于碳足迹的考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依组件划分,2022-2035年

- 电池组

- 电动驱动模组

- 直流/交流逆变器

- DC/DC转换器

- 热力系统

- 电源分配模组(PDM)

- 其他的

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 电池式电动车(BEV)

- 混合动力电动车(HEV)

- 插电式混合动力汽车(PHEV)

- 燃料电池汽车(FCEV)

第七章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车

- MCV(中型商用车)

- 重型商用车(HCV)

第八章 市场估算与预测:依销售管道划分,2022-2035年

- OEM

- 售后市场

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Aisin

- BorgWarner

- Continental

- Denso

- Eaton

- Hitachi Astemo

- Hyundai Mobis

- Magna International

- Marelli

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- 当地公司

- BYD Company

- Contemporary Amperex Technology

- Dana

- Infineon Technologies

- LG Energy Solution

- MAHLE

- Nidec

- Panasonic(Automotive Division)

- 新兴企业

- American Axle &Manufacturing

- GKN Automotive(Dowlais Group)

- Mitsubishi Electric

- QuantumScape

- WiTricity

The Global Automotive Electric Drivetrain Components Market was valued at USD 63.4 billion in 2025 and is estimated to grow at a CAGR of 24.1% to reach USD 488.8 billion by 2035.

Rapid electrification across the automotive sector is accelerating demand for advanced electric drivetrain systems. Tightening emission standards worldwide compel original equipment manufacturers to transition toward electric vehicle platforms at a faster pace. This regulatory pressure is significantly increasing the production of e-drives, inverters, power electronics, and integrated electric propulsion modules. Continuous cost reductions in lithium-ion battery manufacturing and improvements in production efficiency are further reshaping vehicle pricing structures, making electric vehicles more competitive. As battery costs decline, manufacturers are scaling production of lightweight electric motors and high-efficiency inverter systems to meet growing global demand. Advancements in drivetrain technology are also enhancing vehicle range, charging compatibility, and overall system performance, which supports broader EV adoption. Automakers are integrating intelligent e-axles, connected control modules, and advanced diagnostics into electric drivetrain architectures to optimize real-time monitoring and energy management. The combination of regulatory mandates, falling battery costs, and performance-driven innovation is positioning electric drivetrain components as a core growth engine within the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $63.4 Billion |

| Forecast Value | $488.8 Billion |

| CAGR | 24.1% |

The battery packs segment held a 26% share in 2025 and is anticipated to grow at a CAGR of 26.4% from 2026 to 2035. Ongoing advancements in energy density, battery management systems, and next-generation cell chemistries are improving driving range and operational safety. Industry focus remains centered on faster charging capabilities, enhanced durability, and cost optimization. Emerging battery technologies and evolving material compositions are expected to further strengthen performance benchmarks and manufacturing scalability throughout the forecast period.

The passenger cars segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 25.2% between 2026 and 2035. Emission reduction targets and the pursuit of improved efficiency drive increasing electrification within the passenger vehicle segment. Automakers are deploying lightweight drivetrain modules, modular architectures, and high-capacity battery systems to optimize range and vehicle dynamics. Consumers are benefiting from expanding charging networks and supportive government incentives, which are accelerating adoption across urban and suburban regions. Modern passenger electric vehicles incorporate integrated technologies such as regenerative braking, real-time energy optimization, and connected vehicle systems, all of which rely on advanced electric drivetrain components.

North America Automotive Electric Drivetrain Components Market reached USD 17.2 billion in 2025. Regional efforts to harmonize electric vehicle standards across major markets are reducing cross-border supply constraints and enabling higher-volume manufacturing of drivetrain systems. Industry collaboration among suppliers is fostering the development of next-generation e-axle technologies and integrated propulsion platforms. At the same time, continued expansion of charging infrastructure throughout 2025 is strengthening consumer confidence and stimulating further demand for electric drivetrain components.

Key companies operating in the Global Automotive Electric Drivetrain Components Market include Robert Bosch, BorgWarner, ZF Friedrichshafen, Magna International, Denso, Continental, GKN Automotive, Hyundai Mobis, Dana, and Hitachi Astemo. Companies competing in the Global Automotive Electric Drivetrain Components Market are reinforcing their competitive edge through sustained investment in research and development, strategic partnerships, and vertical integration. Manufacturers are advancing high-efficiency e-drive systems, compact inverters, and integrated e-axle platforms to enhance performance and reduce system weight. Collaborations with automakers secure long-term supply agreements and early-stage integration into new electric vehicle platforms. Firms are expanding production capacity and localizing supply chains to mitigate risk and improve responsiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption & electrification push

- 3.2.1.2 Strict emission regulations & government policies

- 3.2.1.3 Declining battery costs & improving tech performance

- 3.2.1.4 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production & component costs

- 3.2.2.2 Supply chain vulnerabilities & raw material constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Advanced power electronics & lightweight modular designs

- 3.2.3.2 Emerging & developing markets

- 3.2.3.3 Sustainability & recycling solutions

- 3.2.3.4 Collaborations & cross industry partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Alliance for Automotive Innovation

- 3.4.1.2 Automotive Industry Action Group

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations (WP.29)

- 3.4.3 Asia Pacific

- 3.4.3.1 APEC Automotive Dialogue

- 3.4.3.2 ASEAN Automotive Federation

- 3.4.4 Latin America

- 3.4.4.1 Mexican Association for the Promotion of Electric Vehicles

- 3.4.4.2 Brazilian Electric Vehicle Association

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Vendor cost structure

- 3.10.2 Implementation of cost components

- 3.10.3 Ongoing operational costs

- 3.10.4 Indirect customer costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand units)

- 5.1 Key trends

- 5.2 Battery packs

- 5.3 Electric drive module

- 5.4 DC/AC inverter

- 5.5 DC/DC converter

- 5.6 Thermal system

- 5.7 Power distribution module (PDM)

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Thousand units)

- 6.1 Key trends

- 6.2 Battery electric vehicle (BEV)

- 6.3 Hybrid electric vehicle (HEV)

- 6.4 Plug-in hybrid electric vehicle (PHEV)

- 6.5 Fuel cell electric vehicle (FCEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Thousand units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Aisin

- 10.1.2 BorgWarner

- 10.1.3 Continental

- 10.1.4 Denso

- 10.1.5 Eaton

- 10.1.6 Hitachi Astemo

- 10.1.7 Hyundai Mobis

- 10.1.8 Magna International

- 10.1.9 Marelli

- 10.1.10 Robert Bosch

- 10.1.11 Valeo

- 10.1.12 ZF Friedrichshafen

- 10.2 Regional players

- 10.2.1 BYD Company

- 10.2.2 Contemporary Amperex Technology

- 10.2.3 Dana

- 10.2.4 Infineon Technologies

- 10.2.5 LG Energy Solution

- 10.2.6 MAHLE

- 10.2.7 Nidec

- 10.2.8 Panasonic (Automotive Division)

- 10.3 Emerging players

- 10.3.1 American Axle & Manufacturing

- 10.3.2 GKN Automotive (Dowlais Group)

- 10.3.3 Mitsubishi Electric

- 10.3.4 QuantumScape

- 10.3.5 WiTricity

2026-2034年全球汽车电动传动系统零件市场规模、份额、趋势及成长分析报告全球汽车动力传动系统市场规模、份额、趋势和成长分析报告(2026-2034年)汽车传动系统市场规模、份额、成长率及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

2026-2034年全球汽车电动传动系统零件市场规模、份额、趋势及成长分析报告全球汽车动力传动系统市场规模、份额、趋势和成长分析报告(2026-2034年)汽车传动系统市场规模、份额、成长率及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 汽车动力传动系统市场规模、份额、趋势及预测(依车辆类型、动力传动系统及地区划分,2026-2034年)

汽车动力传动系统市场规模、份额、趋势及预测(依车辆类型、动力传动系统及地区划分,2026-2034年) 电动商用车马达控制器市场(按控制器类型、额定功率、额定电压、车辆类型、架构和最终用户产业划分),全球预测(2026-2032年)

电动商用车马达控制器市场(按控制器类型、额定功率、额定电压、车辆类型、架构和最终用户产业划分),全球预测(2026-2032年) 汽车动力传动系统技术市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、技术、地区及竞争格局划分,2021-2031年预测)

汽车动力传动系统技术市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、技术、地区及竞争格局划分,2021-2031年预测) 汽车动力传动系统市场规模、份额和成长分析(按车辆类型、动力传动系统、零件和地区划分)-2026-2033年产业预测

汽车动力传动系统市场规模、份额和成长分析(按车辆类型、动力传动系统、零件和地区划分)-2026-2033年产业预测 齿轮磨刀器:全球市场份额和排名、总收入和需求预测(2025-2031年)

齿轮磨刀器:全球市场份额和排名、总收入和需求预测(2025-2031年) 内齿轮滑齿机市场规模、份额和趋势分析报告:按机器类型、自动化程度、齿轮尺寸、技术、最终用途、地区和细分市场预测(2025-2033 年)全球锁毂市场按产品类型、材料类型、最终用途、车辆类型和分销管道划分-2025-2030 年全球预测

内齿轮滑齿机市场规模、份额和趋势分析报告:按机器类型、自动化程度、齿轮尺寸、技术、最终用途、地区和细分市场预测(2025-2033 年)全球锁毂市场按产品类型、材料类型、最终用途、车辆类型和分销管道划分-2025-2030 年全球预测