|

市场调查报告书

商品编码

1982325

2026 年至 2035 年微创手术器材的市场机会、成长要素、产业趋势与预测。Minimally Invasive Surgical Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

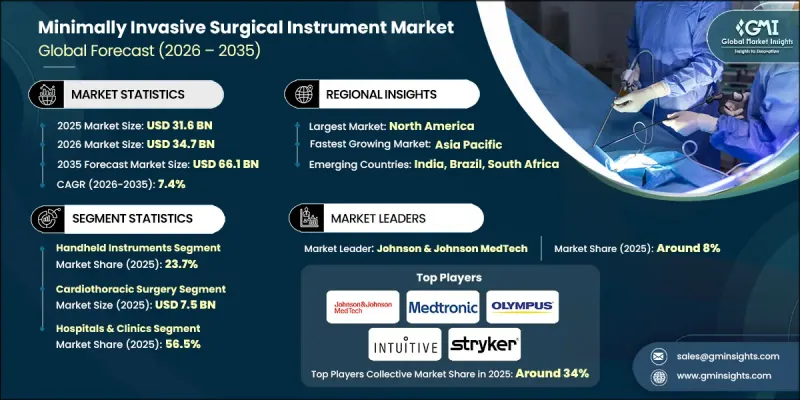

2025年全球微创手术器械市场价值为316亿美元,预计到2035年将以7.4%的复合年增长率增长至661亿美元。

微创手术需求的激增、机器人辅助手术的日益普及、技术的持续创新以及慢性病盛行率的上升是推动该市场成长的主要因素。人口老化和已开发国家门诊手术的日益增加也进一步促进了市场成长。手术器械的最新进展拓展了微创手术在多个专科领域的应用范围。触觉回馈等技术增强了外科医生的触觉感知能力,而一次性先进能量器材则提高了医疗机构的无菌性和成本效益。机器人辅助平台的广泛应用使得以往只能透过开放性手术完成的手术现在可以透过微创方式进行。总而言之,先进器械、手术效率的提高以及为医院带来的成本节约效益的结合,正在推动这些技术在全球范围内的普及应用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 316亿美元 |

| 预计金额 | 661亿美元 |

| 复合年增长率 | 7.4% |

到2025年,手持式器械市场占有率将达到23.7%。这些器械的创新重点在于人体工学设计、提高操作灵活性以触及难以到达的解剖区域,以及采用轻便耐用的材料,例如钛合金和先进聚合物。主要的手持式器械包括腹腔镜抓钳、剪刀、持针器和其他专用器械。一次性、无菌器材的需求也是推动此品类成长的重要因素。

预计2025年,心胸外科手术市场规模将达75亿美元。与传统手术方法相比,微创心血管手术通常切口较小,从而缩短恢復时间,降低感染风险,并减少功能障碍。机器人辅助平台可实现3D可视化并提高器械的灵活性,使瓣膜修復等精准手术更有效率且安全。

预计2025年,美国微创手术器械市场规模将达116亿美元。该地区的成长主要得益于高昂的人均医疗成本、完善的医保报销体係以及对尖端医疗技术的早期应用。私人保险和联邦医疗保险(Medicare)对微创手术的广泛覆盖,支撑了多个外科专科的需求。此外,医疗机构也逐渐意识到缩短住院时间和改善患者预后所带来的成本效益,从而推动了对微创手术基础设施的投资。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策及对资料完整性的承诺

- 资讯来源一致性通讯协定

- GMI人工智慧政策及对资料完整性的承诺

- 调查过程和可靠性评分

- 研究路径的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 慢性病盛行率增加

- 外科器械的技术进步

- 机器人辅助手术的广泛应用

- 微创手术的需求正在激增。

- 产业潜在风险与挑战

- 手术器械高成本

- 开发中国家的还款挑战

- 机会

- 电外科和能量设备领域的技术创新

- 远端手术和远端辅助手术的扩展

- 促进因素

- 成长潜力分析

- 监理情势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析

- 救赎方案

- 北美洲

- 欧洲

- 亚太地区

- 政策环境

- 供应链分析

- 对环境和永续发展的承诺

- 投资机会和创业投资趋势

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 手持装置

- 夹爪

- 收缩器和升降器

- 扩充器

- 缝合器械

- 其他手持工具

- 监测和可视化设备

- 外科内视镜

- 腹腔镜

- 关节镜

- 泌尿系统内视镜

- 神经科学用内视镜

- 其他内视镜

- 扩充装置

- 切削刀具

- 导向装置

- 引导管

- 导管导引线

- 辅助器具

- 电外科设备

第六章 市场估计与预测:依手术类型划分,2022-2035年

- 心胸外科

- 整形外科手术

- 胃肠外科手术

- 泌尿系统手术

- 妇科手术

- 美容和肥胖手术

- 其他类型的手术

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院和诊所

- 门诊手术中心

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- Abbott

- B. Braun

- Becton, Dickinson and Company

- Biorad Medisys

- Boston Scientific

- CONMED

- FUJIFILM

- Intuitive Surgical Operations

- Johnson & Johnson MedTech

- KARL STORZ

- Medtronic

- OLYMPUS

- Smith+Nephew

- Stryker

- WEXLER SURGICAL

- ZIMMER BIOMET

The Global Minimally Invasive Surgical Instrument Market was valued at USD 31.6 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 66.1 billion by 2035.

The market is propelled by a surge in demand for less invasive surgical procedures, wider adoption of robotic-assisted surgeries, ongoing technological innovation, and the increasing prevalence of chronic conditions. Aging populations and the rising trend of outpatient surgeries in developed countries are further supporting market expansion. Recent developments in surgical instruments have expanded the range of minimally invasive procedures across multiple specialties. Technologies such as haptic feedback have enhanced surgeons' tactile perception, while disposable advanced energy devices improve sterility and cost-effectiveness for healthcare facilities. Robotic-assisted platforms have become widely accessible, allowing procedures once limited to open surgeries to now be performed minimally invasively. Overall, the combination of advanced instrumentation, procedural efficiency, and hospital cost-saving benefits is driving the adoption of these technologies globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.6 Billion |

| Forecast Value | $66.1 Billion |

| CAGR | 7.4% |

The handheld instruments segment held a 23.7% share in 2025. Innovations in these devices focus on ergonomics, increased articulation for hard-to-reach anatomical areas, and the use of lightweight, durable materials like titanium alloys and advanced polymers. Core handheld tools include laparoscopic graspers, scissors, needle holders, and other specialty instruments. Emphasis on disposable and infection-free instruments is also supporting growth in this category.

The cardiothoracic surgery segment reached USD 7.5 billion in 2025. Minimally invasive cardiac procedures typically use smaller incisions rather than traditional approaches, reducing recovery times, infection risk, and functional limitations. Robotic-assisted platforms provide three-dimensional visualization and enhanced instrument articulation, enabling precise procedures such as valve repairs to be conducted more efficiently and safely.

U.S. Minimally Invasive Surgical Instrument Market was valued at USD 11.6 billion in 2025. Growth in the region is fueled by high per-capita healthcare spending, sophisticated reimbursement systems, and early adoption of cutting-edge medical technologies. The widespread coverage of minimally invasive procedures by private insurance and Medicare supports demand across multiple surgical specialties. Additionally, healthcare providers recognize the cost benefits of shorter hospital stays and improved patient outcomes, encouraging investment in minimally invasive infrastructure.

Key players in the Global Minimally Invasive Surgical Instrument Market include Johnson & Johnson MedTech, Intuitive Surgical Operations, Medtronic, B. Braun, Boston Scientific, Stryker, Abbott, OLYMPUS, Smith + Nephew, Becton, Dickinson and Company, KARL STORZ, ZIMMER BIOMET, WEXLER SURGICAL, FUJIFILM, and Biorad Medisys. Market leaders adopt several strategies to strengthen their presence. They focus heavily on research and development to launch advanced, ergonomically designed instruments and integrate robotic-assisted technology. Companies expand both direct and indirect distribution networks while forming strategic collaborations with hospitals and surgical centers to increase adoption. Marketing campaigns highlight clinical efficacy, procedural efficiency, and cost benefits, while training programs ensure surgeon proficiency with new devices. Firms also pursue mergers, acquisitions, and geographic expansion to gain market share and enhance global competitiveness, leveraging innovation and strong brand recognition to maintain leadership in the rapidly growing minimally invasive surgical instruments sector.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Surgery type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancements in surgical instruments

- 3.2.1.3 Growing adoption of robotic-assisted surgeries

- 3.2.1.4 Surging demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of surgical instruments

- 3.2.2.2 Reimbursement challenges in developing countries

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovations in electrosurgical and energy devices

- 3.2.3.2 Expansion of tele-surgery and remote-assisted operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Reimbursement scenario

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Policy landscape

- 3.9 Supply chain analysis

- 3.10 Environmental and sustainability initiatives

- 3.11 Investment opportunities and venture capital trends

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Handheld instruments

- 5.2.1 Graspers

- 5.2.2 Retractors/elevators

- 5.2.3 Dilators

- 5.2.4 Suturing instruments

- 5.2.5 Other handheld instruments

- 5.3 Monitoring & visualization devices

- 5.4 Surgical scopes

- 5.4.1 Laparoscopes

- 5.4.2 Arthroscopes

- 5.4.3 Urology endoscopes

- 5.4.4 Neuroendoscopes

- 5.4.5 Other scopes

- 5.5 Inflation devices

- 5.6 Cutter instruments

- 5.7 Guiding devices

- 5.7.1 Guiding catheters

- 5.7.2 Guidewires

- 5.8 Auxiliary devices

- 5.9 Electrosurgical devices

Chapter 6 Market Estimates and Forecast, By Surgery Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiothoracic surgery

- 6.3 Orthopedic surgery

- 6.4 Gastrointestinal surgery

- 6.5 Urological surgery

- 6.6 Gynecological surgery

- 6.7 Cosmetic & bariatric surgery

- 6.8 Other surgery types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end-users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 B. Braun

- 9.3 Becton, Dickinson and Company

- 9.4 Biorad Medisys

- 9.5 Boston Scientific

- 9.6 CONMED

- 9.7 FUJIFILM

- 9.8 Intuitive Surgical Operations

- 9.9 Johnson & Johnson MedTech

- 9.10 KARL STORZ

- 9.11 Medtronic

- 9.12 OLYMPUS

- 9.13 Smith + Nephew

- 9.14 Stryker

- 9.15 WEXLER SURGICAL

- 9.16 ZIMMER BIOMET