|

市场调查报告书

商品编码

1982330

2026 年至 2035 年电动Scooter升降机和运输车的市场机会、成长要素、产业趋势分析和预测。Electric Scooter Lift and Carrier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

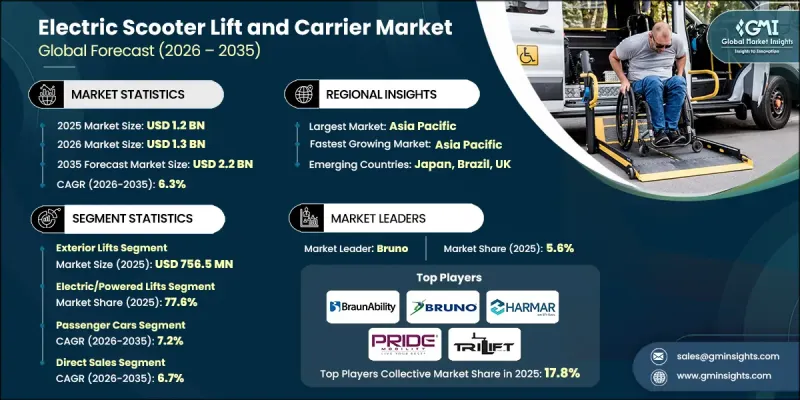

预计到 2025 年,全球电动Scooter升降机和运输车市场价值将达到 12 亿美元,并预计以 6.3% 的复合年增长率增长,到 2035 年达到 22 亿美元。

对便利安全的电动Scooter运输解决方案的需求日益增长,推动了市场扩张。这些系统被老年人和行动不便者广泛使用,他们需要可靠的设备来移动Scooter。看护者、医疗保健专业人员和住宅机构也对高效的装载和储存解决方案提出了更高的需求。技术进步显着提升了产品功能,最新的系统融合了电动装置、无线控制和先进的安全组件,简化了操作。轻巧耐用的材料和模组化结构提高了车辆相容性和安装便利性。行业创新与更广泛的出行趋势保持同步,这些趋势强调自主性、舒适性和与电动和混合动力汽车的无缝整合。随着电动车的普及,製造商正致力于研发节能型升降系统,旨在最大限度地降低能耗,同时保持高性能和结构强度。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 12亿美元 |

| 预测金额 | 22亿美元 |

| 复合年增长率 | 6.3% |

产品研发的重点在于提升安全性、易用性和便利性。最新产品配备了自动升降机构、简化的操作介面和增强型稳定係统,最大限度地减少了操作人员的身体负担,并提高了可靠性。防滑平台和高度适应性的安装结构等设计改进,确保了Scooter在运输过程中稳固可靠,并可适应多种车型。

预计2025年,外置升降机市占率将达到64.9%,市场规模将达7.565亿美元。其强劲的市场地位得益于其与多种车型相容,以及无需对车辆内部进行任何改装即可轻鬆安装。外置升降机系统可节省车内空间,通常配备折迭式或电动平台,简化装卸操作。其便捷实用的特性使其成为个人使用者和专业护理人员寻求高效运输解决方案的首选,且无需对车辆进行结构性改装。

预计到2025年,电动升降机和动力升降机市场份额将达到77.6%,到2035年市场规模将达到18亿美元。动力升降系统正逐渐成为主流,因为其人性化的设计使得使用者只需极少的体力即可搬运Scooter。这些解决方案对行动不便或行动受限的用户尤其具有吸引力,因为它们显着减轻了搬运负担,并降低了受伤风险。其日益增长的普及速度持续超过手动升降机。

预计到2025年,美国电动Scooter升降机和运输车市场规模将达到3.946亿美元。对无障碍出行解决方案日益增长的需求正在推动全国范围内的普及。随着电动Scooter使用量的增加,对可靠运输系统的需求也随之成长。车载升降平台和紧凑型运输车旨在简化装卸过程,同时减轻使用者的体力负担。製造商正在整合智慧功能和轻量化结构组件,以提高营运效率和整体用户体验。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球人口老化和行动障碍日益增多

- 残疾和慢性病增加

- 电动代步Scooter和电动轮椅的广泛普及。

- 消费者对出行解决方案的认知度不断提高

- 产业潜在风险与挑战

- 高昂的初始购买和安装成本

- 车辆相容性和改装方面的挑战

- 市场机会

- 亚太及新兴市场扩张

- 与电动车和自动驾驶汽车的集成

- 开发轻巧小巧的设计

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国运输部

- 美国国家公路交通安全管理局

- 美国无障碍委员会

- 加拿大运输部

- 加拿大标准协会

- 欧洲

- 欧盟委员会

- 欧洲标准化委员会

- 欧洲铁路管理局

- 车辆认证机构

- TUV Rheinland

- 亚太地区

- 国土交通省

- 中华人民共和国交通部

- 印度汽车研究协会

- 陆路交通局

- 拉丁美洲

- 陆路运输署

- 国家计量、品质和技术研究院

- 基础设施、通讯和运输部

- 国立先进工业科学技术研究所

- 工商监督署

- 中东和非洲

- 能源和基础设施部

- 沙乌地阿拉伯标准、计量和品质组织

- 南非标准局

- 海湾标准化组织

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 目前技术

- 液压升降系统

- 电动平台升降机

- 挂钩式载具系统

- 车载式起吊装置和吊车

- 遥控升降机构

- 新兴技术

- 物联网智慧电梯系统

- 人工智慧驱动的负载检测与安全控制

- 轻质复合材料结构

- 自动展开式升降平台

- 电动车整合电源管理系统

- 目前技术

- 生产统计

- 生产基地

- 消费中心

- 进出口

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 永续性和环境影响

- 环境影响评估

- 社会影响和对当地社区的益处

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 与电动车生态系统的整合

- 电动车特定设计要求

- 电池负载对电动车续航里程的影响

- 充电基础设施相容性

- 与智慧车辆集成

- 未来电动车平台的机会

- 安装和使用者体验分析

- 按车辆类型分類的安装复杂性

- 专业安装与自行安装

- 安装时间和成本分析

- 为老年人和身心障碍者提供无障碍设施

- 使用者介面和易用性

- 人工智慧对市场的影响

- 智慧负载管理

- 自动驾驶功能

- 个人化使用者体验

- 客户支援和故障排除

- 案例研究

- 未来前景与机会

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估算与预测:依产品划分,2022-2035年

- 室内电梯

- 平台升降机

- 起吊装置/吊车

- 室外电梯

- 挂钩式载具

- 卡车货箱式升降机

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 电动升降机

- 手动升降机

第七章 市场估计与预测:依负载容量,2022-2035年

- 轻载

- 中号

- 大的

第八章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- SUV

- 轿车

- MPV

- 皮卡车

- 小型货车

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 个人使用

- 医疗设施

- 旅行和交通服务

- 商业和租赁服务

第十章 市场估价与预测:依销售管道划分,2022-2035年

- 直销

- 间接销售

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 比利时

- 俄罗斯

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 新加坡

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界公司

- Bruno

- Harmar Mobility

- BraunAbility

- Ricon

- Pride Mobility

- American Wheelchairs

- Invacare

- Drive Mobility

- 当地公司

- Wheelchair Carrier

- EZ Carrier

- Vantage Mobility

- TriLift

- Autolift

- Savaria

- Mobility Innovations

- HandiRamp

- 新兴企业

- ComfyGO

- Fotona Mobility

- 备註 - 欧洲

- Himor Lift

The Global Electric Scooter Lift and Carrier Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 2.2 billion by 2035.

The rising need for convenient and secure transportation solutions for mobility scooters drives market expansion. These systems are widely used by aging populations and individuals with mobility limitations who require dependable equipment to move scooters between locations. Demand is also supported by caregivers, healthcare providers, and residential care environments seeking efficient loading and storage solutions. Technological progress is significantly enhancing product functionality, with modern systems incorporating powered mechanisms, wireless controls, and advanced safety components to simplify operation. The use of lightweight yet durable materials, along with modular construction, allows improved vehicle compatibility and easier installation. Industry innovation is aligning with broader mobility trends that emphasize independence, comfort, and seamless integration with electric and hybrid vehicles. As electric vehicle adoption increases, manufacturers are focusing on energy-efficient lift systems engineered to consume minimal power while maintaining high performance and structural strength.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 6.3% |

Product development is centered on improving safety, usability, and convenience. Advanced configurations now feature automated lifting mechanisms, simplified control interfaces, and reinforced stabilization systems that minimize physical strain and enhance reliability. Design enhancements such as slip-resistant platforms and adaptable mounting structures enable compatibility with a wide range of vehicle types while maintaining secure scooter positioning during transport.

The exterior lifts segment held 64.9% share, generating USD 756.5 million in 2025. Its strong position is attributed to broad vehicle compatibility and straightforward installation processes that eliminate the need for interior vehicle modifications. Exterior-mounted systems preserve cabin space and often incorporate foldable or powered platforms that streamline loading and unloading procedures. Their practicality and ease of operation have made them a preferred choice among both individual users and professional caregivers seeking efficient transport solutions without structural vehicle alterations.

The electric or powered lifts segment held 77.6% share in 2025 and is forecast to reach USD 1.8 billion by 2035. Powered systems dominate due to their user-friendly design, enabling scooter handling with minimal physical effort. These solutions significantly reduce lifting strain and lower the risk of injury, making them especially appealing to users with limited strength or mobility challenges. Their growing popularity continues to outpace manually operated alternatives.

U.S. Electric Scooter Lift and Carrier Market reached USD 394.6 million in 2025. Increasing demand for accessible mobility solutions is driving adoption across the country. As mobility scooters become more widely used, the need for reliable transportation systems has intensified. Vehicle-mounted lifting platforms and compact carrier configurations are designed to simplify loading and unloading processes while reducing the physical burden on users. Manufacturers are integrating smart functionality and lightweight structural components to improve operational efficiency and overall user experience.

Key companies operating in the Global Electric Scooter Lift and Carrier Market include Bruno, Harmar, BraunAbility, Drive Mobility, Pride, American Wheelchairs, EZ Carrier, Comfygo, TriLift, and Himor Lift. Companies in the Electric Scooter Lift and Carrier Market are strengthening their competitive position through product innovation, strategic partnerships, and geographic expansion. Manufacturers are investing in research and development to introduce lighter, energy-efficient, and technologically advanced lifting systems that enhance user convenience and safety. Collaboration with vehicle manufacturers and mobility equipment distributors helps expand market reach and improve product compatibility. Businesses are also focusing on expanding distribution networks and improving after-sales service to build customer loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Operation

- 2.2.4 Weight Capacity

- 2.2.5 Vehicle

- 2.2.6 End-Use

- 2.2.7 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global elderly population & mobility impairment cases

- 3.2.1.2 Increasing prevalence of disabilities & chronic conditions

- 3.2.1.3 Growing adoption of mobility scooters & electric wheelchairs

- 3.2.1.4 Rising consumer awareness of mobility solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial purchase & installation costs

- 3.2.2.2 Vehicle compatibility & modification challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Asia Pacific & emerging markets

- 3.2.3.2 Integration with electric & autonomous vehicles

- 3.2.3.3 Development of lightweight & compact designs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Transportation

- 3.4.1.2 National Highway Traffic Safety Administration

- 3.4.1.3 U.S. Access Board

- 3.4.1.4 Transport Canada

- 3.4.1.5 Canadian Standards Association

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 European Committee for Standardization

- 3.4.2.3 European Union Agency for Railways

- 3.4.2.4 Vehicle Certification Agency

- 3.4.2.5 TUV Rheinland

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Land, Infrastructure, Transport and Tourism

- 3.4.3.2 Ministry of Transport of the People's Republic of China

- 3.4.3.3 Automotive Research Association of India

- 3.4.3.4 Land Transport Authority

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Transportes Terrestres

- 3.4.4.2 Instituto Nacional de Metrologia, Calidad y Tecnologia

- 3.4.4.3 Secretaria de Infraestructura, Comunicaciones y Transportes

- 3.4.4.4 Instituto Nacional de Tecnologia Industrial

- 3.4.4.5 Superintendencia de Industria y Comercio

- 3.4.5 Middle East & Africa

- 3.4.5.1 Ministry of Energy and Infrastructure

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization

- 3.4.5.3 South African Bureau of Standards

- 3.4.5.4 Gulf Standardization Organization

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technologies

- 3.7.1.1 Hydraulic lift systems

- 3.7.1.2 Electric motorized platform lifts

- 3.7.1.3 Hitch-mounted carrier systems

- 3.7.1.4 Inside-vehicle hoist and crane lifts

- 3.7.1.5 Remote-control operated lifting mechanisms

- 3.7.2 Emerging technologies

- 3.7.2.1 IoT-enabled smart lift systems

- 3.7.2.2 AI-based load sensing and safety control

- 3.7.2.3 Lightweight composite material structures

- 3.7.2.4 Automated self-deploying lift platforms

- 3.7.2.5 EV-integrated power management systems

- 3.7.1 Current technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Integration with EV ecosystems

- 3.12.1 EV-specific design requirements

- 3.12.2 Battery load impact on EV range

- 3.12.3 Charging infrastructure compatibility

- 3.12.4 Smart vehicle integration

- 3.12.5 Future ev platform opportunities

- 3.13 Installation & user experience analysis

- 3.13.1 Installation complexity by vehicle type

- 3.13.2 Professional vs DIY installation

- 3.13.3 Installation time & cost analysis

- 3.13.4 Accessibility for elderly & disabled users

- 3.13.5 User interface & controls usability

- 3.14 Impact of AI on the market

- 3.14.1 Smart load management

- 3.14.2 Autonomous operation features

- 3.14.3 Personalized user experience

- 3.14.4 Customer support & troubleshooting

- 3.15 Case studies

- 3.16 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Interior lifts

- 5.2.1 Platform lifts

- 5.2.2 Hoist/Crane lifts

- 5.3 Exterior lifts

- 5.3.1 Hitch-mounted carriers

- 5.3.2 Truck bed-mounted lifts

Chapter 6 Market Estimates & Forecast, By Operation, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Electric/Powered lifts

- 6.3 Manual lifts

Chapter 7 Market Estimates & Forecast, By Weight Capacity, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Light duty

- 7.3 Medium duty

- 7.4 Heavy duty

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 SUV

- 8.2.3 Sedan

- 8.2.4 MPV

- 8.3 Pickup Trucks

- 8.4 Minivans

Chapter 9 Market Estimates & Forecast, By End-Use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Individual/Personal use

- 9.3 Healthcare facilities

- 9.4 Mobility & transportation services

- 9.5 Commercial/Rental services

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Russia

- 11.3.8 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Singapore

- 11.4.7 Indonesia

- 11.4.8 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Bruno

- 12.1.2 Harmar Mobility

- 12.1.3 BraunAbility

- 12.1.4 Ricon

- 12.1.5 Pride Mobility

- 12.1.6 American Wheelchairs

- 12.1.7 Invacare

- 12.1.8 Drive Mobility

- 12.2 Regional players

- 12.2.1 Wheelchair Carrier

- 12.2.2 EZ Carrier

- 12.2.3 Vantage Mobility

- 12.2.4 TriLift

- 12.2.5 Autolift

- 12.2.6 Savaria

- 12.2.7 Mobility Innovations

- 12.2.8 HandiRamp

- 12.3 Emerging players

- 12.3.1 ComfyGO

- 12.3.2 Fotona Mobility

- 12.3.3 Memo Europe

- 12.3.4 Himor Lift

2026年全球折迭式电动Scooter市场报告2026年全球电动自行车和Scooter市场报告2026年全球电动Scooter共享市场报告

2026年全球折迭式电动Scooter市场报告2026年全球电动自行车和Scooter市场报告2026年全球电动Scooter共享市场报告 面向老年人的无障碍交通出行市场预测(至2034年):按交通方式、技术、最终用户和地区分類的全球分析

面向老年人的无障碍交通出行市场预测(至2034年):按交通方式、技术、最终用户和地区分類的全球分析 全球电动Scooter市场:依产品类型、应用、销售管道、电池类型、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年)

全球电动Scooter市场:依产品类型、应用、销售管道、电池类型、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年) 全球带座椅电动Scooter市场(按电池类型、应用和分销管道划分)预测(2026-2032)电动DC马达Scooter直流马达市场:按马达类型、额定功率、电压、应用、最终用户和分销管道划分,全球预测(2026-2032年)电动Scooter马达市场:按马达类型、功率、电压、销售管道、应用和最终用户划分,全球预测(2026-2032年)

全球带座椅电动Scooter市场(按电池类型、应用和分销管道划分)预测(2026-2032)电动DC马达Scooter直流马达市场:按马达类型、额定功率、电压、应用、最终用户和分销管道划分,全球预测(2026-2032年)电动Scooter马达市场:按马达类型、功率、电压、销售管道、应用和最终用户划分,全球预测(2026-2032年) 微型电动自行车市场规模、份额和成长分析(按类型、有效载荷能力、应用、最终用户和地区划分)—2026-2033年产业预测

微型电动自行车市场规模、份额和成长分析(按类型、有效载荷能力、应用、最终用户和地区划分)—2026-2033年产业预测 电动滑板Scooter市场规模、份额和成长分析(按电池类型、驱动系统、产品类型、电压、应用、最终用户和地区划分)—2026-2033年产业预测

电动滑板Scooter市场规模、份额和成长分析(按电池类型、驱动系统、产品类型、电压、应用、最终用户和地区划分)—2026-2033年产业预测