|

市场调查报告书

商品编码

1982342

手术台市场机会、成长要素、产业趋势分析及2026-2035年预测Surgical Table Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

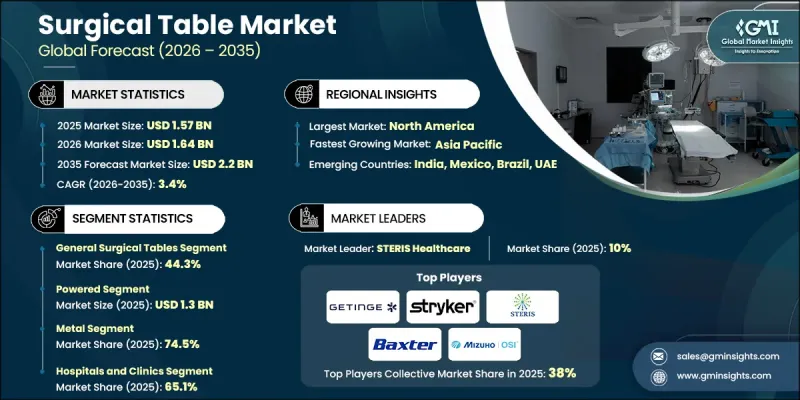

全球手术台市场预计到 2025 年将达到 15.7 亿美元,年复合成长率为 3.4%,到 2035 年将达到 22 亿美元。

全球手术量增加、医疗保健支出上升以及新兴地区医疗基础设施发展是推动市场扩张的主要因素。手术台技术的创新,以及医院和门诊手术中心数量的成长,持续刺激市场需求。由于慢性病和创伤病例增加、人口老化以及外科手术服务覆盖范围扩大,普通外科、整形外科、循环系统外科和微创手术的数量都在增加。医院和手术中心正投资购买最先进的手术台,以提高病人安全、手术精准度和营运效率。为因应手术量的成长,医院和手术中心纷纷更换老旧手术台,同时不断进行设计创新以提升临床性能,这些因素共同推动了市场渗透。总而言之,便利性、安全性和技术进步的融合,正使该市场受益匪浅。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 15.7亿美元 |

| 预计金额 | 22亿美元 |

| 复合年增长率 | 3.4% |

预计到2025年,一般外科手术台市占率将达到44.3%,主要得益于市场对符合人体工学和多功能设计的高需求。这些手术台适用于多种一般外科手术,包括腹部手术、血管手术和内分泌手术。其可调节的定位、柔软性以及与标准手术配件的兼容性,使其成为医院和门诊手术中心不可或缺的设备。

预计2025年,电动手术台市场规模将达13亿美元。由于电动手术台具有精准、调节平稳、操作高效等优点,医院越来越倾向选择电动手术台。对于那些进行大量复杂微创手术、对精准度和易用性要求极高的医疗机构而言,电动手术台尤其受欢迎。

预计到2025年,北美手术台市占率将达到35.1%,并在整个预测期内保持稳定成长。该地区的成长主要得益于手术量大、医疗基础设施先进以及对最尖端科技的早期应用。对电动和影像增强手术台的投资正在推动微创手术、整形外科手术和机器人辅助手术的发展。老旧手动手术台因不符合现代安全和人体工学标准而被淘汰,这也持续推动市场需求。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策及对资料完整性的承诺

- 资讯来源一致性通讯协定

- GMI人工智慧政策及对资料完整性的承诺

- 调查过程和可靠性评分

- 研究路径的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 全球手术数量增加

- 手术台的技术进步

- 新兴市场医疗保健成本上升和基础设施改善

- 医院和门诊手术中心数量增加

- 产业潜在风险与挑战

- 由复合材料製成的手术台成本高昂

- 机会

- 电动和混合动力手术台的需求日益增长

- 新兴国家医疗旅游的兴起

- 促进因素

- 成长潜力分析

- 监理情势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 政策环境

- 供应链分析

- 按设备类型进行价格分析

- 对环境和永续发展的承诺

- 波特的分析

- PESTEL 分析

- 差距分析

- 消费者洞察

- 未来市场趋势

- 人工智慧和生成式人工智慧对市场的影响

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 通用手术台

- 专用手术台

- 减重手术

- 神经外科

- 泌尿系统

- 整形外科

- 其他专用手术台

- 儿童手术台

- 渗透性手术台

第六章 市场估算与预测:依设备类型划分,2022-2035年

- 动力

- 电的

- 油压

- 杂交种

- 无动力

第七章 市场估计与预测:依材料划分,2022-2035年

- 金属

- 复合材料

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 医院和诊所

- 门诊手术中心

- 其他最终用户

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- ALVO Medical

- AMTAI Medical Equipment, Inc

- Baxter

- FAMED Lodz

- Getinge

- medifa GmbH

- Merivaara Corp

- Mizuho OSI

- Narang Medical Limited

- SKYTRON

- STERIS Healthcare

- Stille

- Stryker

The Global Surgical Table Market was valued at USD 1.57 billion in 2025 and is estimated to grow at a CAGR of 3.4% to reach USD 2.2 billion by 2035.

Market expansion is driven by the increasing volume of surgical procedures worldwide, rising healthcare spending, and the development of healthcare infrastructure in emerging regions. Technological innovation in surgical tables, coupled with a growing number of hospitals and ambulatory surgical centers, continues to fuel demand. The rise in chronic diseases, trauma cases, and an aging population, along with broader access to surgical care, is boosting procedure volumes across general, orthopedic, cardiovascular, and minimally invasive surgeries. Hospitals and surgical centers are investing in modern tables to improve patient safety, surgical precision, and operational efficiency. Replacement of older tables due to higher surgical throughput, combined with design innovations that enhance clinical performance, is further accelerating market adoption. Overall, the market is benefiting from the convergence of accessibility, safety, and technological advancements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.57 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 3.4% |

The general surgical tables segment 44.3% share in 2025, owing to high demand for ergonomic and versatile designs. These tables accommodate a wide variety of general surgical procedures, including abdominal, vascular, and endocrine surgeries. Their adjustable positioning, flexibility, and compatibility with standard surgical accessories make them indispensable in hospitals and ambulatory surgical centers.

The powered surgical tables segment reached USD 1.3 billion in 2025. Hospitals increasingly prefer powered tables for their precision, smooth adjustments, and operational efficiency. These tables are particularly popular in high-volume facilities performing complex and minimally invasive procedures, where accuracy and ease of use are critical.

North America Surgical Table Market accounted for 35.1% share in 2025 and is expected to grow steadily over the forecast period. The region's growth is fueled by high surgical volumes, advanced healthcare infrastructure, and early adoption of cutting-edge technologies. Investments in electric and imaging-compatible tables are supporting minimally invasive, orthopedic, and robotic-assisted surgeries. Replacement of older manual tables that do not meet modern safety and ergonomic standards continues to drive demand.

Key players in the Global Surgical Table Market include STERIS Healthcare, Mizuho OSI, ALVO Medical, Baxter, Merivaara Corp, Getinge, Stille, AMTAI Medical Equipment, Inc., FAMED Lodz, Narang Medical Limited, medifa GmbH, and SKYTRON. Companies in the surgical table market strengthen their position by focusing on innovation, including powered and imaging-compatible tables that enhance precision and efficiency. Many players are expanding product portfolios to cover general, orthopedic, cardiovascular, and minimally invasive applications. Strategic collaborations with hospitals and surgical centers improve market penetration and provide feedback for product development. Firms are investing in ergonomics, patient safety features, and modular designs to meet evolving clinical requirements. Geographic expansion into emerging markets and targeted marketing initiatives help reach a wider customer base.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Device type trends

- 2.2.4 Material trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of surgical procedures globally

- 3.2.1.2 Technological advancements in surgical tables

- 3.2.1.3 Rising healthcare expenditure coupled with improving infrastructure in emerging markets

- 3.2.1.4 Increasing number of hospitals and ambulatory surgical centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of composite surgical tables

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for electric and hybrid surgical tables

- 3.2.3.2 Rising medical tourism in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Policy landscape

- 3.7 Supply chain analysis

- 3.8 Pricing analysis by device type

- 3.9 Environmental and sustainability initiatives

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Consumer insights

- 3.14 Future market trends

- 3.15 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 General surgical tables

- 5.3 Specialty surgical tables

- 5.3.1 Bariatric

- 5.3.2 Neurology

- 5.3.3 Urology

- 5.3.4 Orthopedic

- 5.3.5 Other specialty surgical tables

- 5.4 Pediatric surgical tables

- 5.5 Radiolucent surgical tables

Chapter 6 Market Estimates and Forecast, By Device Type, 2022 - 2035 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Powered

- 6.2.1 Electric

- 6.2.2 Hydraulic

- 6.2.3 Hybrid

- 6.3 Non-powered

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Metal

- 7.3 Composite

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Ambulatory surgical centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALVO Medical

- 10.2 AMTAI Medical Equipment, Inc

- 10.3 Baxter

- 10.4 FAMED Lodz

- 10.5 Getinge

- 10.6 medifa GmbH

- 10.7 Merivaara Corp

- 10.8 Mizuho OSI

- 10.9 Narang Medical Limited

- 10.10 SKYTRON

- 10.11 STERIS Healthcare

- 10.12 Stille

- 10.13 Stryker

解剖台市场:2026-2032年全球市场预测(依产品类型、材质、价格范围、最终用户和应用划分)

解剖台市场:2026-2032年全球市场预测(依产品类型、材质、价格范围、最终用户和应用划分) 2026年全球手术台及照明市场报告2026年全球手术台市场报告

2026年全球手术台及照明市场报告2026年全球手术台市场报告 全球手术台市场规模、份额、趋势和成长分析报告(2026-2034年)全球手术台市场规模、份额、趋势和成长分析报告(2026-2034年)

全球手术台市场规模、份额、趋势和成长分析报告(2026-2034年)全球手术台市场规模、份额、趋势和成长分析报告(2026-2034年) 手术台市场 - 全球产业规模、份额、趋势、机会及预测(依产品类型、材质、最终用途、地区及竞争格局划分,2021-2031年)翻新手术台市场按类型、机制、移动性、应用、最终用户和销售管道,全球预测,2026-2032年

手术台市场 - 全球产业规模、份额、趋势、机会及预测(依产品类型、材质、最终用途、地区及竞争格局划分,2021-2031年)翻新手术台市场按类型、机制、移动性、应用、最终用户和销售管道,全球预测,2026-2032年 手术台市场规模、份额和成长分析(按产品类型、材质、最终用户和地区划分)-2026-2033年产业预测手术台市场-2025-2030年预测

手术台市场规模、份额和成长分析(按产品类型、材质、最终用户和地区划分)-2026-2033年产业预测手术台市场-2025-2030年预测 皮肤科检查台市场报告:趋势、预测和竞争分析(至 2031 年)

皮肤科检查台市场报告:趋势、预测和竞争分析(至 2031 年)