|

市场调查报告书

商品编码

1982353

地板清洁设备市场机会、成长要素、产业趋势分析及2026-2035年预测。Floor Cleaning Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

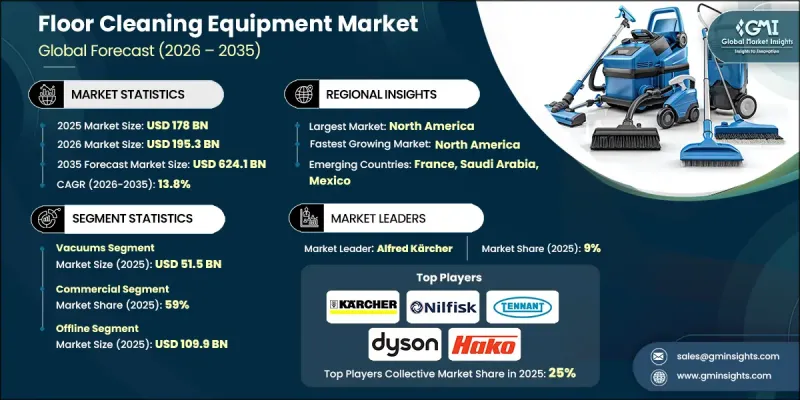

预计到 2025 年,全球地面清洁设备市场价值将达到 1,780 亿美元,并将以 13.8% 的复合年增长率成长,到 2035 年达到 6,241 亿美元。

人们对住宅、商业和公共环境中的卫生和公共卫生标准的日益重视,正显着推动市场扩张。干净且维护良好的地板越来越被认为是保障整体安全、舒适度和提升品牌形象的关键。消费者越来越重视外观卫生的生活和职场环境,这正在改变传统的清洁方式。企业不再只依赖人工,而是投资先进的设备型清洁解决方案,以提高营运效率并维持一致的卫生标准。同时,生活方式的改变、健康意识的增强以及对低尘室内环境的需求,也提高了房主对清洁度的期望。使用者希望以最少的努力减少过敏原、改善室内空气品质并保持美观的空间,因此对高效且技术先进的地板清洁设备的需求不断增长。快速的都市化、住宅基础设施的扩张以及自动化清洁技术的创新,持续重塑全球地板清洁设备市场的竞争格局。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 1780亿美元 |

| 预测金额 | 6241亿美元 |

| 复合年增长率 | 13.8% |

在住宅中,安装高性能吸尘器以维持更健康的室内环境并简化日常维护已成为日益流行的趋势。人们对空气中颗粒物和整体健康的担忧正在影响他们的购买决策,促使住宅选择耐用、节能且易于使用的产品。这种意识的增强推动了市场对能够以更少的时间和精力实现卓越清洁效果的设备的需求。

预计到2025年,吸尘器市场规模将达到515亿美元。吸尘器在日常清洁中扮演着核心角色,能够有效率地吸除各种地面上的灰尘、污垢和细小颗粒。与传统的扫地方式(可能将细小颗粒扩散到空气中)不同,吸尘器系统利用吸力和过滤机制来收集污染物,直到进行处理。其便利性、稳定的性能以及能够清洁难以触及的角落,使其成为各种室内环境清洁的理想选择。吸力、过滤技术和人体工学设计的不断进步,正进一步推动着这个细分市场的成长。

到2025年,商业领域将占据59%的市场。长期以来,地面清洁设备在商业环境中至关重要,因为商业环境需要对大占地面积进行持续的卫生管理。这些机器旨在提供快速、均匀且彻底的清洁效果,满足严格的卫生标准和操作要求。人流量大的企业依赖高效的清洁系统来维护安全、符合法规要求并确保整体环境品质。与人工清洁方法相比,机械化清洁解决方案具有更高的一致性和生产效率,因此在商业设施中广泛使用。

预计2025年,美国地面清洁设备市占率将达到78.5%,市场规模将达428亿美元。美国是全球最大的先进地面清洁设备市场之一,这得益于其完善的商业基础设施和严格的清洁标准。随着各组织机构优先考虑能够提高效率、减少人工依赖并确保清洁标准一致的现代化自动化设备,市场需求仍然强劲。技术主导解决方案的加速普及仍然是美国市场格局的关键因素。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 人们越来越关注卫生和清洁问题

- 技术进步

- 从人工清洁过渡到机械化清洁

- 产业潜在风险与挑战

- 高昂的维护和营运成本

- 与传统清洁方法的竞争

- 机会

- 机器人和自动化系统的快速普及

- 医疗和公共设施领域的需求不断增长

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过装置

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特的分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依设备类型划分,2022-2035年

- 洗涤器

- 搭乘用式洗涤器

- 推式洗地机

- 清扫机

- 吸尘器

- 立式吸尘器

- 卧式吸尘器

- 背包式吸尘器

- 机器人吸尘器

- 消失者

- 抛光机

- 撷取器

- 其他(落地式烘干机)

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 住宅

- 商业的

- 饭店及餐饮业

- 办公室

- 其他的

第七章 市场估计与预测:依价格划分,2022-2035年

- 低的

- 中等的

- 高的

第八章 市场估算与预测:依通路划分,2022-2035年

- 在线的

- 电子商务

- 品牌官方网站

- 离线

- 超级市场

- 专卖店

- 其他(百货公司等)

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Alfred Karcher

- Bosch

- Comac

- Dyson

- Eureka

- Factory Cat

- Fimap

- Haier

- Hako

- IPC Group

- LG

- Nilfisk

- Panasonic

- Taski

- Tennant

The Global Floor Cleaning Equipment Market was valued at USD 178 billion in 2025 and is estimated to grow at a CAGR of 13.8% to reach USD 624.1 billion by 2035.

Rising awareness of hygiene and sanitation standards across residential, commercial, and public environments is significantly driving market expansion. Clean and well-maintained floors are increasingly viewed as essential to overall safety, comfort, and brand perception. Consumers are placing greater emphasis on visibly sanitized living and working spaces, which has transformed traditional cleaning practices. Organizations are investing in advanced, equipment-driven cleaning solutions to improve operational efficiency and maintain consistent hygiene standards rather than relying solely on manual labor. At the same time, homeowners are elevating their cleanliness expectations due to lifestyle shifts, health awareness, and the desire for low-dust indoor environments. Demand for efficient and technologically advanced floor cleaning machines is rising as users seek to reduce allergens, enhance indoor air quality, and maintain visually appealing spaces with minimal effort. Rapid urbanization, growth in commercial infrastructure, and innovation in automated cleaning technologies continue to reshape the competitive landscape of the global floor cleaning equipment market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $178 Billion |

| Forecast Value | $624.1 Billion |

| CAGR | 13.8% |

Residential consumers are increasingly adopting high-performance cleaning machines to support healthier indoor environments and simplify routine maintenance. Concerns about airborne particles and general well-being are influencing purchasing decisions, encouraging households to select durable, energy-efficient, and user-friendly products. As awareness grows, the preference for equipment that delivers superior cleaning outcomes with less time and effort is strengthening market demand.

In 2025, the vacuums segment accounted for USD 51.5 billion. Vacuum cleaners play a central role in daily cleaning by efficiently extracting dust, debris, and microscopic particles from various floor surfaces. Unlike conventional sweeping techniques that may disperse fine particles into the air, vacuum systems use suction and filtration mechanisms to contain contaminants until disposal. Their practicality, performance consistency, and ability to access hard-to-reach areas make them highly preferred for maintaining cleanliness across diverse indoor environments. Continuous advancements in suction power, filtration technology, and ergonomic design are further supporting segment growth.

The commercial segment held 59% share in 2025. Floor cleaning equipment has long been essential in commercial environments that require consistent sanitation across extensive floor areas. These machines are designed to deliver rapid, uniform, and thorough cleaning results, meeting strict hygiene standards and operational requirements. Businesses with high foot traffic depend on efficient cleaning systems to maintain safety, regulatory compliance, and overall environmental quality. Mechanized cleaning solutions provide greater consistency and productivity compared to manual methods, reinforcing their widespread adoption in commercial settings.

U.S. Floor Cleaning Equipment Market held 78.5% share, generating USD 42.8 billion in 2025. The country represents one of the largest global markets for advanced floor cleaning machines, supported by extensive commercial infrastructure and stringent cleanliness expectations. Demand remains strong as organizations prioritize modern, automated equipment that enhances efficiency, reduces labor dependency, and ensures uniform cleaning standards. Accelerated adoption of technology-driven solutions continues to characterize the U.S. market landscape.

Key companies operating in the Global Floor Cleaning Equipment Market include Tennant, Dyson, Nilfisk, Panasonic, Alfred Karcher, Hako, LG, Fimap, Comac, Haier, IPC Group, Eureka, Factory Cat, Bosch, and Taski. Companies in the Global Floor Cleaning Equipment Market are strengthening their competitive positioning through product innovation, automation, and global expansion strategies. Manufacturers are investing in research and development to introduce smart, sensor-enabled, and autonomous cleaning systems that enhance operational efficiency and reduce labor costs. Many firms are focusing on sustainability by developing energy-efficient models and incorporating environmentally responsible materials. Strategic partnerships with distributors and facility management providers are improving market reach and after-sales service capabilities. Companies are also expanding their presence in emerging markets while reinforcing brand visibility through digital marketing and e-commerce platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Application

- 2.2.4 Price

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising focus on hygiene & cleanliness

- 3.2.1.2 Technological advancements

- 3.2.1.3 Shift from manual to mechanized cleaning

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High maintenance & operational costs

- 3.2.2.2 Competition with traditional cleaning methods

- 3.2.3 Opportunities

- 3.2.3.1 Rapid adoption of robotic & automated systems

- 3.2.3.2 Growing demand in healthcare & institutional sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Scrubbers

- 5.2.1 Ride-on scrubbers

- 5.2.2 Walk-behind scrubbers

- 5.3 Sweepers

- 5.4 Vacuums

- 5.4.1 Upright vacuums

- 5.4.2 Canister vacuums

- 5.4.3 Backpack vacuums

- 5.4.4 Robotic vacuums

- 5.5 Burnishers

- 5.6 Polishers

- 5.7 Extractors

- 5.8 Others (Floor Dryers)

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 Hotels & hospitality

- 6.3.2 Offices

- 6.3.3 Others

Chapter 7 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Brand websites

- 8.3 Offline

- 8.3.1 Supermarkets

- 8.3.2 Specialty stores

- 8.3.3 Others (Departmental stores, etc.)

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alfred Karcher

- 10.2 Bosch

- 10.3 Comac

- 10.4 Dyson

- 10.5 Eureka

- 10.6 Factory Cat

- 10.7 Fimap

- 10.8 Haier

- 10.9 Hako

- 10.10 IPC Group

- 10.11 LG

- 10.12 Nilfisk

- 10.13 Panasonic

- 10.14 Taski

- 10.15 Tennant

地板抛光服务市场:按服务类型、地板材料、合约类型、服务提供者、价格范围、最终用户划分,全球预测(2026-2032年)家用地面清洁设备市场:依产品类型、操作方式、应用和分销管道划分-2026-2032年全球预测AI Ultra 二合一扫拖机器人市场:按连接方式、导航技术、地板类型、价格范围、最终用户和分销管道分類的全球预测(2026-2032 年)

地板抛光服务市场:按服务类型、地板材料、合约类型、服务提供者、价格范围、最终用户划分,全球预测(2026-2032年)家用地面清洁设备市场:依产品类型、操作方式、应用和分销管道划分-2026-2032年全球预测AI Ultra 二合一扫拖机器人市场:按连接方式、导航技术、地板类型、价格范围、最终用户和分销管道分類的全球预测(2026-2032 年) 2026-2030年全球地板垫市场地面清洁设备市场依产品类型、操作方式、动力来源、通路和最终用户划分,全球预测(2026-2032年)

2026-2030年全球地板垫市场地面清洁设备市场依产品类型、操作方式、动力来源、通路和最终用户划分,全球预测(2026-2032年) 磨床市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

磨床市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 全球水泥浆清洗设备市场

全球水泥浆清洗设备市场 2025-2029年全球地板清洁机市场全球地板抛光机市场全球地板清洁机市场

2025-2029年全球地板清洁机市场全球地板抛光机市场全球地板清洁机市场