|

市场调查报告书

商品编码

1982357

医疗设备报销市场:成长机会、成长要素、产业趋势分析及 2026-2035 年预测。Medical Devices Reimbursement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

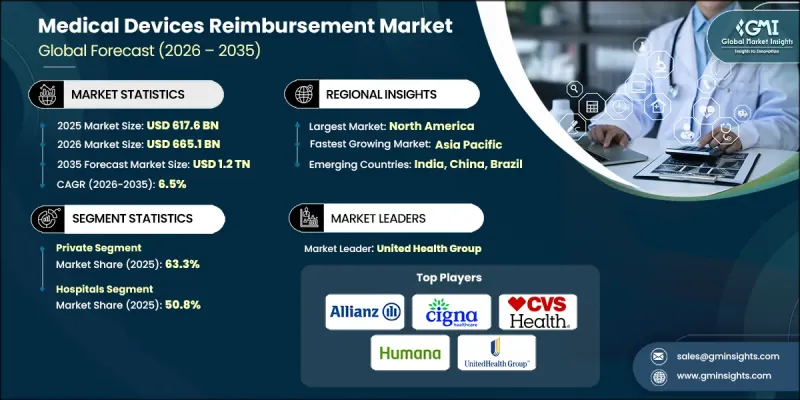

全球医疗设备报销市场预计到 2025 年将达到 6,176 亿美元,预计到 2035 年将以 6.5% 的复合年增长率增长至 1.2 兆美元。

市场扩张的驱动因素包括医疗成本上升、慢性病盛行率增加以及政府为促进医疗设备普及而采取的支持措施。此外,基于价值的医疗模式的采用正在重塑报销框架,强调临床疗效和成本效益。医疗设备报销是指医疗服务提供者(例如医院、诊所和手术中心)在诊断、监测和治疗中使用医疗器材的购置、维护和使用所获得的补偿。随着新的支付模式、资格标准和市场准入管道的出现,报销结构也在不断发展,这为能够改善患者预后并降低整体医疗成本的创新医疗器材创造了机会。这些变革性趋势正在加强医疗设备与现代医疗体系的融合,同时确保其财务永续性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 6176亿美元 |

| 预测金额 | 1.2兆美元 |

| 复合年增长率 | 6.5% |

预计到2025年,私人保险公司市占率将达到63.3%。与公共保险公司相比,私人保险公司、雇主提供的保险计划和补充保险通常能提供更快的理赔审批速度和更优惠的赔付率。此外,私人保险更有可能承保先进的高端医疗设备。这一领域的成长主要得益于中高所得者的增加,尤其是在私人保险渗透率较高的亚太地区。

截至2025年,医院领域将占50.8%的市占率。医院的报销范围将涵盖住院、门诊、门诊手术中心和急诊。推动这一增长的主要因素是手术数量的增加、先进技术的应用以及复杂手术报销范围的扩大。许多医疗设备的报销并非以单一器械计算,而是采用打包支付模式,例如手术费和诊断相关分组(DRG)支付。

预计到2025年,北美医疗设备报销市占率将达到47.2%。美国市场受惠于庞大的医疗保健经济、完善的报销系统、清晰的监管以及医疗技术的先进应用。公共和私人支出确保了高端医疗设备的保险覆盖,从而支撑了市场稳定。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策及对资料完整性的承诺

- 资讯来源一致性通讯协定

- GMI人工智慧政策及对资料完整性的承诺

- 调查过程和可靠性评分

- 研究路径的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 慢性病盛行率增加

- 引入基于价值的医疗保健模式

- 医疗费用不断上涨带来的负担

- 政府扶持计划

- 产业潜在风险与挑战

- 复杂的还款框架

- 少付发票金额或拒收发票。

- 机会

- 扩大远端患者监护的报销范围

- 政府和私人对医疗保健领域的投资

- 促进因素

- 成长潜力分析

- 监理情势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 政策倡议

- 编码系统概述

- 赎回模式展望

- 在政策和促进和谐方面存在区域差异

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依支付方划分,2022-2035年

- 民众

- 私人的

第六章 市场估计与预测:依医疗机构划分,2022-2035年

- 医院

- 门诊设施

- 其他医疗机构

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章:公司简介

- Allianz

- Anthem Insurance Companies, Inc.

- Aviva

- BNP Paribas

- Cigna

- CVS Health

- Experian Health

- Humana Inc.

- Nippon Life Insurance Company

- United Health Group

- WellCare Health Plans, Inc.

The Global Medical Devices Reimbursement Market was valued at USD 617.6 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 1.2 trillion by 2035.

The market expansion is driven by rising healthcare expenditures, increasing prevalence of chronic illnesses, and supportive government initiatives promoting access to medical devices. The adoption of value-based healthcare models has also reshaped reimbursement frameworks, emphasizing clinical effectiveness and cost-efficiency. Medical device reimbursement involves compensating healthcare providers, including hospitals, clinics, and surgical centers, for the acquisition, maintenance, and use of devices in diagnosis, monitoring, and treatment. Reimbursement structures are evolving with new payment models, coverage criteria, and market access pathways, creating opportunities for innovative devices that improve patient outcomes and reduce overall healthcare costs. These transformative trends are strengthening the integration of medical devices into modern healthcare systems while ensuring financial sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $617.6 Billion |

| Forecast Value | $1.2 Trillion |

| CAGR | 6.5% |

The private payer segment held a 63.3% share in 2025. Private insurers, employer-sponsored plans, and supplemental policies generally offer faster coverage decisions and more favorable payment rates than public payers. Private coverage is also more likely to include advanced or premium devices. Growth in this segment is supported by rising middle- and high-income populations, particularly in the Asia-Pacific region, where private insurance adoption is increasing.

The hospitals segment accounted for 50.8% share in 2025. Reimbursement in hospitals includes inpatient, outpatient, ambulatory surgical centers, and emergency departments. Growth is fueled by higher surgical volumes, adoption of advanced technologies, and broader reimbursement for complex procedures. Many devices are reimbursed as part of bundled payments, such as procedure fees or diagnosis-related groups, rather than on an individual device basis.

North America Medical Devices Reimbursement Market held 47.2% share in 2025. The U.S. market benefits from a large healthcare economy, established reimbursement infrastructure, regulatory clarity, and advanced adoption of medical technologies. Public and private spending ensures coverage for premium medical devices and supports market stability.

Key players in the Global Medical Devices Reimbursement Market include Allianz, Anthem Insurance Companies, Inc., Aviva, BNP Paribas, Cigna, CVS Health, Experian Health, Humana Inc., Nippon Life Insurance Company, United Health Group, and WellCare Health Plans, Inc. Companies in the Medical Devices Reimbursement Market strengthen their presence through multiple strategies. They focus on expanding private payer partnerships, offering tailored coverage plans for innovative devices, and negotiating favorable payment terms. Investments in digital claims management, real-time reimbursement analytics, and regulatory compliance tools improve operational efficiency. Firms also develop education programs for healthcare providers to increase adoption of reimbursed devices and demonstrate clinical and economic value. Strategic collaborations with hospitals, insurers, and technology providers enhance market penetration, while ongoing monitoring of evolving policies ensures adaptability to new payment models.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Payer trends

- 2.2.3 Healthcare setting trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Adoption of value-based healthcare models

- 3.2.1.3 Growing burden of healthcare cost

- 3.2.1.4 Supportive government programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex reimbursement framework

- 3.2.2.2 Underpayment or denial of claims

- 3.2.3 Opportunities

- 3.2.3.1 Growth in remote patient monitoring reimbursement

- 3.2.3.2 Government & private investment in healthcare

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Policy initiatives

- 3.7 Coding systems overview

- 3.8 Reimbursement models outlook

- 3.9 Regional policy differences & harmonization efforts

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Payer, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Public

- 5.3 Private

Chapter 6 Market Estimates and Forecast, By Healthcare Setting, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Outpatient facilities

- 6.4 Other settings

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Allianz

- 8.2 Anthem Insurance Companies, Inc.

- 8.3 Aviva

- 8.4 BNP Paribas

- 8.5 Cigna

- 8.6 CVS Health

- 8.7 Experian Health

- 8.8 Humana Inc.

- 8.9 Nippon Life Insurance Company

- 8.10 United Health Group

- 8.11 WellCare Health Plans, Inc.