|

市场调查报告书

商品编码

1982360

碳管理系统市场机会、成长要素、产业趋势分析及2026-2035年预测Carbon Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

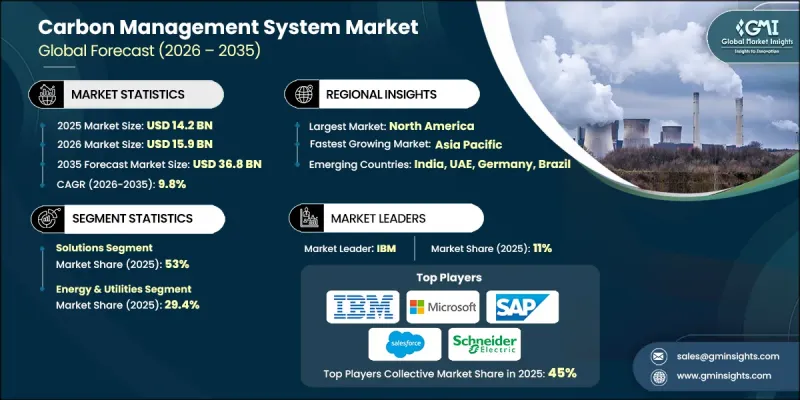

全球碳管理系统市场预计到 2025 年将价值 142 亿美元,预计到 2035 年将以 9.8% 的复合年增长率增长至 368 亿美元。

由于技术创新、监管压力和企业永续发展优先事项的转变,碳管理市场正在经历转型。企业正越来越多地采用碳管理解决方案,以实现全球气候目标、管理营运排放并降低气候相关风险。云端平台的兴起,以及人工智慧 (AI)、机器学习 (ML) 和物联网 (IoT) 技术的融合,正在重塑碳管理实践,实现即时监测、预测分析和自动化报告,从而提高准确性和营运效率。环境、社会和管治(ESG) 报告已成为一项策略要求,促使碳管理服务提供者提供整合的 ESG 工具,用于追踪排放、能源消耗和更广泛的永续发展措施。生命週期评估也日益重要,使企业能够量化产品製造、物流、使用和处置阶段的排放,从而提供可操作的数据,以减少整个供应链的碳足迹。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 142亿美元 |

| 预测金额 | 368亿美元 |

| 复合年增长率 | 9.8% |

预计到 2025 年,解决方案领域将占据 53% 的市场份额,到 2035 年将以 9.4% 的复合年增长率成长。製造业、能源和交通运输业排放概况的日益复杂化,推动了对提供预测分析、即时追踪和 ESG 报告功能的企业级 CMS 平台的需求。

预计到2025年,能源和公共产业产业将占据29.4%的市场份额,到2035年将以10%的复合年增长率成长。由于该产业温室气体排放庞大,因此是碳管理系统(CMS)应用的主要目标领域。随着公共产业不断扩大可再生能源、储能、智慧电网和绿色费率方案的应用,亟需能够即时准确量化碳排放强度,并提供透明、可审计数据的系统,以用于规划和客户报告。

美国碳管理系统市场占82%的份额,预计2025年市场规模将达39亿美元。监管要求已将排放管理转变为营运必需环节,尤其是在油气基础设施的甲烷排放管理方面。各公司正利用碳管理系统平台整合感测器和卫星数据,实现洩漏侦测和修復工作流程的自动化,将技术估计值与实际测量结果进行核对,并维护可供执法部门审计的记录。州级法规和采购计画也在推动将范围1-3的数据整合到资金筹措和合约中,使碳管理系统从单纯的合规工具提升为核心的营运、风险和财务系统。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监理情势

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

- 新机会和趋势

- 数位化和物联网集成

- 进入新兴市场

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 竞争性标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 市场规模及预测:依组件划分,2022-2035年

- 解决方案

- 服务

第六章 市场规模及预测:依市场进入方式划分,2022-2035年

- 云

- 现场

第七章 市场规模及预测:依产业划分,2022-2035年

- 能源与公共产业

- 製造业

- 住宅/商业建筑

- 运输/物流

- 资讯科技/通讯

- 其他的

第八章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第九章:公司简介

- Accuvio

- Carbon Footprint Ltd.

- Dakota Software

- Enablon

- EnergyCap

- Engie

- Enviance

- Envirosoft

- ESP

- IBM

- Intelex

- Isometrix

- Locus Technologies

- NativeEnergy

- Salesforce

- SAP

- Schneider Electric

- Trinity Consultants

- Watershed

- Zevero

The Global Carbon Management System Market was valued at USD 14.2 billion in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 36.8 billion by 2035.

The market is transformed by a combination of technological innovation, regulatory pressure, and evolving corporate sustainability priorities. Businesses are increasingly adopting CMS solutions to align with global climate targets, manage operational emissions, and mitigate climate-related risks. The rise of cloud-based platforms, along with the integration of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) technologies, is reshaping carbon management practices, enabling real-time monitoring, predictive insights, and automated reporting for improved accuracy and operational efficiency. Environmental, Social, and Governance (ESG) reporting has become a strategic imperative, prompting CMS providers to offer integrated ESG tools that track emissions, energy consumption, and broader sustainability initiatives. Lifecycle assessments are also gaining prominence, allowing organizations to quantify emissions from product manufacturing, logistics, use, and end-of-life disposal, providing actionable data to reduce carbon footprints across supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.2 Billion |

| Forecast Value | $36.8 Billion |

| CAGR | 9.8% |

The solutions segment held 53% share in 2025 and is anticipated to grow at a CAGR of 9.4% through 2035. Rising complexity in emissions profiles across manufacturing, energy, and transport sectors is driving demand for enterprise-grade CMS platforms offering predictive analytics, real-time tracking, and ESG reporting capabilities.

The energy and utilities segment held 29.4% share in 2025 and is projected to grow at a CAGR of 10% by 2035. The sector is a major adopter of CMS due to its substantial greenhouse gas emissions. As utilities increase renewable integration, storage, smart grids, and green tariff offerings, they require systems that quantify carbon intensity accurately in real time and provide transparent, auditable data for planning and customer reporting.

U.S. Carbon Management System Market held 82% share, generating USD 3.9 billion in 2025. Regulatory mandates are converting emissions management into operational imperatives, particularly for methane across oil and gas infrastructure. Companies are leveraging CMS platforms to integrate sensor and satellite data, automate leak detection and repair workflows, reconcile engineering estimates with actual measurements, and maintain auditable records suitable for enforcement. State-level regulations and procurement programs are also driving Scope 1-3 data integration into financing and contracts, elevating CMS from a compliance tool to a core operational, risk, and financial system.

Key players in the Global Carbon Management System Market include: Engie, SAP, Enablon, Watershed, Locus Technologies, Accuvio, Dakota Software, IBM, EnergyCap, Intelex, Zevero, NativeEnergy, ESP, Isometrix, Schneider Electric, Carbon Footprint Ltd., Envirosoft, Trinity Consultants, Salesforce, and Enviance. Companies in the Carbon Management System Market are employing strategic initiatives to strengthen their position and expand market presence. They are investing heavily in AI, IoT, and cloud-based innovations to deliver real-time emissions monitoring, predictive analytics, and automated ESG reporting. Strategic alliances and partnerships with utilities, manufacturing firms, and government agencies improve market access and long-term adoption. Companies are expanding globally, localizing solutions to meet regional compliance standards, and integrating CMS platforms with energy management, sustainability, and finance systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Component trends

- 2.1.3 Deployment trends

- 2.1.4 Industry trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Solutions

- 5.3 Services

Chapter 6 Market Size and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Size and Forecast, By Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Energy & utilities

- 7.3 Manufacturing

- 7.4 Residential & commercial building

- 7.5 Transportation & logistics

- 7.6 IT & telecom

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Accuvio

- 9.2 Carbon Footprint Ltd.

- 9.3 Dakota Software

- 9.4 Enablon

- 9.5 EnergyCap

- 9.6 Engie

- 9.7 Enviance

- 9.8 Envirosoft

- 9.9 ESP

- 9.10 IBM

- 9.11 Intelex

- 9.12 Isometrix

- 9.13 Locus Technologies

- 9.14 NativeEnergy

- 9.15 Salesforce

- 9.16 SAP

- 9.17 Schneider Electric

- 9.18 Trinity Consultants

- 9.19 Watershed

- 9.20 Zevero

2026年全球云端排放管理市场报告

2026年全球云端排放管理市场报告 脱碳软体市场:按类型、可近性、技术、部署模式、企业规模和最终用户产业划分-2026-2032年全球预测2026年全球云碳管理系统市场报告碳管理软体市场:按组件、应用、部署类型、最终用户产业、组织类型和企业规模划分-2026-2032年全球预测2026年智慧碳全球市场报告2026年全球碳管理系统市场报告

脱碳软体市场:按类型、可近性、技术、部署模式、企业规模和最终用户产业划分-2026-2032年全球预测2026年全球云碳管理系统市场报告碳管理软体市场:按组件、应用、部署类型、最终用户产业、组织类型和企业规模划分-2026-2032年全球预测2026年智慧碳全球市场报告2026年全球碳管理系统市场报告 智慧碳足迹分析市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户、模组、功能划分酵素催化二氧化碳还原市场分析及预测(至2035年):依类型、产品、服务、技术、应用、材料类型、製程、最终用户、功能及设备划分

智慧碳足迹分析市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户、模组、功能划分酵素催化二氧化碳还原市场分析及预测(至2035年):依类型、产品、服务、技术、应用、材料类型、製程、最终用户、功能及设备划分 2026-2034年全球能源和公共产业碳管理系统市场规模、份额、趋势和成长分析报告

2026-2034年全球能源和公共产业碳管理系统市场规模、份额、趋势和成长分析报告 碳管理软体市场规模、份额、趋势及预测(按组件、应用、垂直产业及地区划分),2026-2034年

碳管理软体市场规模、份额、趋势及预测(按组件、应用、垂直产业及地区划分),2026-2034年