|

市场调查报告书

商品编码

1982367

蛋白质体学市场机会、成长要素、产业趋势分析及2026-2035年预测Proteomics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

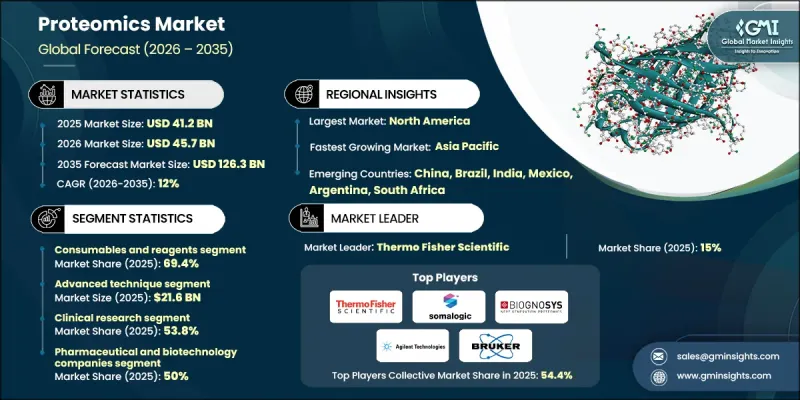

全球蛋白质体学市场预计到 2025 年将达到 412 亿美元,预计到 2035 年将以 12% 的复合年增长率成长至 1,263 亿美元。

蛋白质体学是对生物系统中蛋白质的研究,包括蛋白质的鑑定、定量和功能分析。该领域的工具包括质谱平台、蛋白质微阵列和无标定定量系统,以支援高通量蛋白质谱分析。科技的快速进步以及人工智慧和机器学习在蛋白质体学工作流程中的应用正在推动市场扩张。单细胞蛋白质体学的兴起正在革新研究,它能够在单一细胞层面进行蛋白质分析,从而深入了解肿瘤异质性、疾病进展和免疫系统动态。这些进步不仅改变了研究方式,也使蛋白质体学在临床诊断上的应用日益广泛。现代高通量系统不断提高灵敏度、速度和准确性,增强了大规模研究的数据质量,并加速了全球精准医疗的发展。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 412亿美元 |

| 预测金额 | 1263亿美元 |

| 复合年增长率 | 12% |

预计到 2025 年,耗材和试剂领域将占市场份额的 69.4%,复合年增长率为 12.3%。该领域包括蛋白质晶片、检测试剂盒、试剂、缓衝液、层析管柱和电泳凝胶,这些产品在质谱、层析法和微阵列分析中反覆使用,从而确保了持续的收入。

预计到2025年,先进技术领域的市场规模将达到216亿美元。此领域涵盖质谱分析、蛋白质微阵列、凝胶电泳技术及其他先进技术。与传统方法相比,这些技术具有更高的灵敏度、准确性和通量,从而推动了研究、临床诊断、药物研发和个人化医疗领域的创新。

预计北美蛋白质体学市场规模将在2025年达到199亿美元,到2035年将达到619亿美元,复合年增长率(CAGR)为12.2%。这一增长得益于强大的生物医学研究基础设施、快速的技术应用以及先进的医疗保健生态系统。人工智慧和机器学习在数据分析中的应用,以及学术机构、生技公司和製药公司之间的合作,正在加速蛋白质谱分析、生物标记开发和精准医疗的应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 慢性病和复杂疾病盛行率增加

- 对个人化医疗和精准医疗的需求日益增长

- 质谱和生物资讯技术的进步

- 增加对基于蛋白质体学的药物发现和诊断的投资。

- 产业潜在风险与挑战

- 设备和试剂高成本

- 数据解读与分析的复杂性

- 市场机会

- 拓展临床蛋白质体学在疾病早期检测的应用

- 开发用于标靶治疗的新型生物标记

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 北美洲

- 科技趋势

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依组件划分,2022-2035年

- 装置

- 耗材和试剂

- 服务

第六章 市场估计与预测:依技术划分,2022-2035年

- 先进技术

- 蛋白质微阵列

- 基于凝胶的方法

- 质谱分析

- 其他先进技术

- 传统技术

- ELISA

- 层析法

- 艾德曼定序

- 蛋白质印迹法

- 生物资讯学和电脑分析

- 其他方法

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 临床诊断

- 临床研究

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 製药和生物製药公司

- 学术和研究机构

- 研究所

- 其他最终用户

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Agilent Technologies

- Biognosys

- Bio-Rad

- Bruker

- Creative Proteomics

- F. Hoffmann-La Roche

- Merck KGaA

- PREOMICS

- Promega

- Quantum-Si

- Seer

- SomaLogic Operating

- Thermo Fisher Scientific(Olink)

- Waters

The Global Proteomics Market was valued at USD 41.2 billion in 2025 and is estimated to grow at a CAGR of 12% to reach USD 126.3 billion by 2035.

Proteomics encompasses the study of proteins within biological systems, including their identification, quantification, and functional analysis. Tools in this market include mass spectrometry platforms, protein microarrays, and label-free quantification systems that support high-throughput protein profiling. Rapid advancements in technology and the integration of AI and machine learning into proteomic workflows are driving market expansion. The rise of single-cell proteomics is revolutionizing research by enabling protein analysis at the individual cell level, providing deep insights into tumor heterogeneity, disease progression, and immune system dynamics. These advances are not only transforming research but are also making proteomics increasingly applicable in clinical diagnostics. Modern high-throughput systems continue to improve sensitivity, speed, and accuracy, enhancing data quality for large-scale studies and accelerating precision medicine development worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $41.2 Billion |

| Forecast Value | $126.3 Billion |

| CAGR | 12% |

The consumables and reagents segment accounted for 69.4% share in 2025 and is projected to grow at a CAGR of 12.3%. This segment includes protein chips, assay kits, reagents, buffers, chromatography columns, and electrophoresis gels, which are repeatedly used in mass spectrometry, chromatography, and microarray analyses, ensuring recurring revenue.

The advanced techniques segment reached USD 21.6 billion in 2025. This category includes mass spectrometry, protein microarrays, gel-based techniques, and other advanced methods. These approaches provide superior sensitivity, precision, and throughput compared to conventional methods, driving innovation in research, clinical diagnostics, drug development, and personalized therapies.

North America Proteomics Market reached USD 19.9 billion in 2025 and is projected to reach USD 61.9 billion by 2035, at a CAGR of 12.2%. Growth in the region is fueled by strong biomedical research infrastructure, rapid technology adoption, and an advanced healthcare ecosystem. The integration of AI and machine learning for data analysis, alongside collaboration among academic institutions, biotech firms, and pharmaceutical companies, is accelerating protein profiling, biomarker development, and precision medicine applications.

Key players in the Global Proteomics Market include Agilent Technologies, Biognosys, Bio-Rad, Bruker, Creative Proteomics, F. Hoffmann-La Roche, Merck KGaA, PREOMICS, Promega, Quantum-Si, Seer, SomaLogic, Thermo Fisher Scientific (Olink), and Waters. Companies in the Proteomics Market are strengthening their position by investing heavily in R&D to improve the sensitivity, accuracy, and throughput of proteomics platforms. They are forming strategic partnerships with academic institutions, pharmaceutical firms, and biotech startups to expand their service offerings and enhance collaborative innovation. Firms are also integrating AI and machine learning to streamline workflows and generate actionable insights from large proteomic datasets. Additionally, they are launching comprehensive consumable and reagent portfolios to ensure recurring revenue, expanding geographically to capture emerging markets, and participating in clinical validation programs to support regulatory approvals and adoption in clinical diagnostics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Technique trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic and complex diseases

- 3.2.1.2 Increasing demand for personalized and precision medicine

- 3.2.1.3 Advancements in mass spectrometry and bioinformatics technologies

- 3.2.1.4 Growing investments in proteomics-based drug discovery and diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of instruments and reagents

- 3.2.2.2 Complexity in data interpretation and analysis

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of clinical proteomics for early disease detection

- 3.2.3.2 Development of novel biomarkers for targeted therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Consumables and reagents

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Technique, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Advanced technique

- 6.2.1 Protein microarray

- 6.2.2 Gel-based technique

- 6.2.3 Mass spectrometry

- 6.2.4 Other advanced techniques

- 6.3 Conventional technique

- 6.3.1 ELISA

- 6.3.2 Chromatography based technique

- 6.3.3 Edman sequencing

- 6.3.4 Western blotting

- 6.4 Bioinformatics and computational analysis

- 6.5 Other techniques

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical diagnostics

- 7.3 Clinical research

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biopharmaceutical companies

- 8.3 Academic and research institutions

- 8.4 Laboratories

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent Technologies

- 10.2 Biognosys

- 10.3 Bio-Rad

- 10.4 Bruker

- 10.5 Creative Proteomics

- 10.6 F. Hoffmann-La Roche

- 10.7 Merck KGaA

- 10.8 PREOMICS

- 10.9 Promega

- 10.10 Quantum-Si

- 10.11 Seer

- 10.12 SomaLogic Operating

- 10.13 Thermo Fisher Scientific (Olink)

- 10.14 Waters

蛋白质体学市场:按类型、产品类型、技术、蛋白质体学种类、应用和最终用户划分-2026-2032年全球市场预测

蛋白质体学市场:按类型、产品类型、技术、蛋白质体学种类、应用和最终用户划分-2026-2032年全球市场预测 全球蛋白质体学市场:策略性洞察与预测(2026-2031年)核受体分析服务市场(按服务类型、测试类型、技术、应用和最终用户划分),全球预测,2026-2032年全球蛋白质体学市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球蛋白质体学市场:策略性洞察与预测(2026-2031年)核受体分析服务市场(按服务类型、测试类型、技术、应用和最终用户划分),全球预测,2026-2032年全球蛋白质体学市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 日本蛋白质体学市场报告(按分析类型、组件类型、技术、应用、最终用户(临床诊断实验室、研究机构及其他)和地区划分,2026-2034 年)

日本蛋白质体学市场报告(按分析类型、组件类型、技术、应用、最终用户(临床诊断实验室、研究机构及其他)和地区划分,2026-2034 年) 亚太地区蛋白质体学市场:按细分市场、应用和国家分類的分析和预测(2025-2035 年)

亚太地区蛋白质体学市场:按细分市场、应用和国家分類的分析和预测(2025-2035 年) 欧洲蛋白质体学市场:按细分市场、应用和国家分類的分析和预测(2025-2035 年)

欧洲蛋白质体学市场:按细分市场、应用和国家分類的分析和预测(2025-2035 年) 蛋白质体学市场-全球及区域分析:按产品、技术、应用、最终用户和地区划分-分析与预测(2025-2035)

蛋白质体学市场-全球及区域分析:按产品、技术、应用、最终用户和地区划分-分析与预测(2025-2035) 蛋白质体学市场

蛋白质体学市场 蛋白质体学市场-全球产业规模、份额、趋势、机会和预测,按产品、技术、应用、类型、最终用户、地区和竞争细分,2020-2030 年

蛋白质体学市场-全球产业规模、份额、趋势、机会和预测,按产品、技术、应用、类型、最终用户、地区和竞争细分,2020-2030 年