|

市场调查报告书

商品编码

1982386

自行车车架市场商机、成长要素、产业趋势分析及2026-2035年预测。Bicycle Frames Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

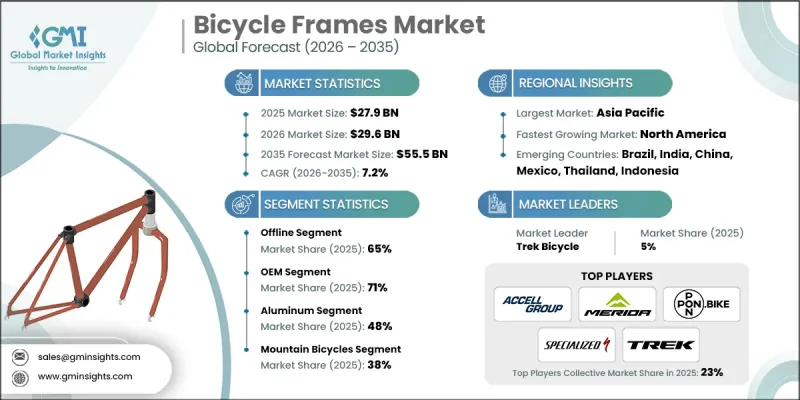

预计到 2025 年,全球自行车车架市场价值将达到 279 亿美元,并预计以 7.2% 的复合年增长率成长,到 2035 年达到 555 亿美元。

自行车车架在任何自行车的整体性能、安全性、耐用性和骑乘体验中都扮演着至关重要的角色,无论是公路车、山地自行车、混合动力车或电动自行车。由于车架直接影响骑乘舒适度、重量、空气动力学性能和载重能力,製造商正致力于轻量化材料和创新设计。该市场涵盖使用铝、碳纤维、钢、钛和先进复合材料製造车架,包括设计、管材成型、焊接、表面处理以及向OEM和售后市场渠道供货。液压成型铝和高模量碳纤维车架的技术进步显着提高了刚性重量比,并增强了性能。人们对健康、城市交通和自行车基础设施日益增长的关注正在推动对先进车架的需求。政府推广永续交通途径的措施和电动自行车的普及进一步促进了对增强型电池相容车架设计的需求,推动市场朝向高性能、环保的出行解决方案发展。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 279亿美元 |

| 预测金额 | 555亿美元 |

| 复合年增长率 | 7.2% |

预计到2025年,线下通路将占据65%的市场份额,并在2035年之前以6.9%的复合年增长率成长。由于自行车购买涉及实体检验,因此能够提供试骑、专业适配服务和社区互动的离线管道仍然至关重要。专业零售商透过提供专家咨询、交货前组装和持续维护支援来建立客户忠诚度并保证其零售利润。

预计到2025年,OEM(整车製造商)市占率将达到71%,并在2035年之前以7.5%的复合年增长率成长。 OEM伙伴关係的重点在于产量保障、联合技术开发、供应链整合以及智慧财产权(IP)合作。车架製造商透过材料创新、悬吊设计、製造流程优化和产品测试等方式为自行车品牌提供支援。电动自行车的成长进一步巩固了OEM管道,因为电池、马达和电子元件的整合需要车架供应商和品牌之间密切的技术合作。

预计2026年至2035年,中国自行车车架市场将以5.6%的复合年增长率成长。国家政策强调轻量化车架技术和与电动自行车相容的设计,以支持城市交通现代化、环保交通基础设施建设以及提升国内製造业竞争力。鼓励在地采购奖励和遵守出口法规的激励措施正在增强国内车架製造商在国内外市场的竞争力。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 健康意识的提高和骑乘运动的普及。

- 城市交通转型与交通拥挤解决方案

- 政府为促进自行车基础建设所做的努力

- 电动自行车市场的快速成长正在推动对专用车架的需求。

- 高性能自行车对轻质材料的需求

- 产业潜在风险与挑战

- 先进材料(碳纤维、钛)高成本

- 供应链中断和原材料短缺

- 后疫情时代市场饱和与库存过剩

- 来自低成本亚洲製造商的竞争

- 市场机会

- 电动自行车市场的发展需要更坚固的车架。

- 对客製化的需求使得高价位产品成为可能。

- 永续和可回收材料的创新

- 在新兴市场(印度、东南亚、拉丁美洲)拓展业务

- 直接面向消费者(D2C)经营模式的成长

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国消费品安全委员会 (CPSC) 自行车车架标准

- 加拿大 - 《加拿大消费品安全法》(CCPSA)下的自行车法规

- 欧洲

- 德国DIN标准与EN 15194电动自行车车架认证

- 英国—脱欧后自行车车架的安全和UKCA标誌要求

- 法国 - NF 标准和国家主动出行认证框架

- 义大利-UNI标准与智慧交通系统自行车基础设施的整合

- 亚太地区

- 中国和英国关于电动自行车车架的标准以及工信部技术法规

- 印度 - BIS 认证和 AIS 自行车车架安全标准

- 日本JIS标准与国土交通省自行车安全框架

- 澳洲 - 澳洲消费者法和AS/NZS自行车车架标准

- 拉丁美洲

- 墨西哥 - NOM 自行车安全标准和积极移动框架

- 阿根廷 - 交通法第 24.449 号

- 中东和非洲(MEA)

- 南非 - 道路交通法(1996 年)

- 沙乌地阿拉伯—SASO标准和2030愿景倡议促进积极出行

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 感测器技术的发展(摄影机、光达、雷达、超音波)

- 整合感测器融合

- 人工智慧和机器学习在行人侦测的应用

- 新兴技术

- V2X 通讯可提高侦测能力

- 适用于夜间和低光源环境的侦测技术

- 当前技术趋势

- 专利分析

- 主要专利趋势

- 技术创新热点

- 主要企业提交的专利申请

- 新的智慧财产权战略

- 价格分析

- 对过去价格趋势的分析

- 铝合金车架价格走势(2022-2025)

- 钢骨价格趋势(2022-2025)

- 碳纤维车架价格趋势(2022-2025)

- 钛合金车架价格趋势(2022-2025)

- 按玩家类型分類的定价策略

- 高阶定位策略(钛合金、高模量碳纤维)

- 价值细分市场策略(铝、标准碳钢)

- 成本定价模式(OEM製造)

- 使用案例和成功案例

- 案例研究

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- 设计自动化与生成式工程

- 品管和缺陷检测系统

- 需求预测和库存优化

- 风险、限制和监管考量

- 客户设计资料中的资料隐私

- 人工智慧模型在结构工程中的可靠性

- 对劳动力替代的担忧

- 未来前景与机会

- 新兴市场板块

- 未来预期的技术变革

- 永续发展趋势

- 经营模式创新

- 长期成长预测(2030-2040 年)

- 相关人员的策略建议

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依材料划分,2022-2035年

- 铝

- 钢

- 碳纤维

- 钛

- 其他的

第六章 市场估计与预测:依框架划分,2022-2035年

- 山地自行车

- 油电混合自行车

- 电动自行车

- 公路自行车

- 其他的

第七章 市场估价与预测:依销售管道划分,2022-2035年

- 在线的

- 离线

第八章 市场估算与预测:依通路划分,2022-2035年

- OEM

- 售后市场

第九章 市场估计与预测:依最终用途划分,2022-2035年

- 专业赛车自行车

- 休閒和爱好者的自行车

- 通勤者/都市区骑行者

- 年轻的自行车手

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 瑞典

- 丹麦

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

第十一章:公司简介

- 世界公司

- Argon 18

- Bianchi

- Cannondale Bikes

- Canyon

- Cervelo

- Cicli Pinarello SRL

- Giant Manufacturing

- GT Bicycles

- Kona Bikes

- Merida

- Santa Cruz

- SCOTT Sports

- Specialized Bicycle

- Trek

- 本地球员

- Chicago Bicycle Company

- Ideal Bike

- Dengfu Sports Equipment

- 新兴企业和技术基础设施公司

- Pinion

- YT Industries

- Aventon Bikes

The Global Bicycle Frames Market was valued at USD 27.9 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 55.5 billion by 2035.

Bicycle frames play a crucial role in overall bicycle performance, safety, durability, and rider experience across road, mountain, hybrid, and electric models. They directly affect ride quality, weight, aerodynamics, and load capacity, prompting manufacturers to focus on lightweight materials and innovative designs. The market includes frame production using aluminum, carbon fiber, steel, titanium, and advanced composite materials, encompassing design, tube forming, welding, surface finishing, and supply to OEM and aftermarket channels. Advances in hydroformed aluminum and high-modulus carbon fiber frames have significantly improved stiffness-to-weight ratios, enhancing performance. Rising interest in health, urban mobility, and cycling infrastructure is driving demand for advanced frames. Government initiatives promoting sustainable transportation and the growth of e-bikes further support demand for reinforced, battery-compatible frame designs, positioning the market toward high-performance, eco-friendly mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.9 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 7.2% |

The offline segment held a 65% share in 2025 and is expected to grow at a CAGR of 6.9% through 2035. Offline channels remain critical due to the hands-on nature of bicycle purchases, enabling test rides, professional fitting services, and community engagement. Specialty retailers provide expert consultations, pre-delivery assembly, and ongoing mechanical support, creating customer loyalty and justifying retail margins.

The OEM segment accounted for 71% share in 2025 and is estimated to grow at a CAGR of 7.5% through 2035. OEM partnerships focus on volume commitments, technical co-development, supply chain integration, and IP collaboration. Frame manufacturers support bicycle brands through material innovation, suspension design, manufacturing optimization, and product testing. Growth in e-bikes further strengthens the OEM channel, as integrating batteries, motors, and electronics requires close technical collaboration between frame suppliers and brands.

China Bicycle Frames Market is projected to grow at a CAGR of 5.6% from 2026 to 2035. National policies emphasize lightweight frame technologies and e-bike-compatible designs to support urban mobility modernization, green transportation infrastructure, and domestic manufacturing competitiveness. Incentives for local sourcing and compliance with export regulations enhance the competitiveness of domestic frame manufacturers in both local and international markets.

Key players in the Global Bicycle Frames Market include Trek, Cannondale Bikes, Bianchi, Cervelo, Specialized Bicycle, SCOTT Sports, Argon 18, Santa Cruz, Giant Manufacturing, and Canyon. Leading companies in the Global Bicycle Frames Market strengthen their position through strategic approaches. They invest in research and development to launch innovative, lightweight, and high-performance frames, integrating advanced materials and e-bike-ready designs. Firms expand distribution across offline and online channels, ensuring professional fitting and after-sales support. Partnerships with OEMs and component manufacturers enhance co-development and technical collaboration. Marketing emphasizes performance, durability, and sustainability, while strategic global expansion, manufacturing localization, and adherence to regulatory requirements allow companies to capture new markets and reinforce brand reputation in a highly competitive landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Frame

- 2.2.4 Sales Channel

- 2.2.5 Distribution Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health awareness and cycling adoption.

- 3.2.1.2 Urban mobility shift and traffic congestion solutions.

- 3.2.1.3 Government initiatives promoting cycling infrastructure.

- 3.2.1.4 E-bike market boom driving specialized frame demand.

- 3.2.1.5 Lightweight material demand for performance cycling.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced materials (carbon fiber, titanium).

- 3.2.2.2 Supply chain disruptions and raw material shortages.

- 3.2.2.3 Post-COVID market saturation and excess inventory.

- 3.2.2.4 Price competition from low-cost Asian manufacturers.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing e-bike segment requiring reinforced frames.

- 3.2.3.2 Customization demand enabling premium pricing.

- 3.2.3.3 Sustainable and recycled material innovation.

- 3.2.3.4 Expansion in emerging markets (India, Southeast Asia, LATAM).

- 3.2.3.5 Direct-to-consumer (D2C) business model growth.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Consumer product safety commission (CPSC) bicycle frame Standards

- 3.4.1.2 Canada - Canada consumer product safety act (CCPSA) bicycle regulations

- 3.4.2 Europe

- 3.4.2.1 Germany- DIN standards & EN 15194 E-bike frame certification

- 3.4.2.2 UK- Post-brexit bicycle frame safety & UKCA marking requirements

- 3.4.2.3 France- NF standards & national active mobility certification framework

- 3.4.2.4 Italy- UNI standards & ITS cycling infrastructure integration

- 3.4.3 Asia Pacific

- 3.4.3.1 China- GB standards & MIIT E-bike frame technical regulations

- 3.4.3.2 India- BIS certification & AIS bicycle frame safety standards

- 3.4.3.3 Japan- JIS standards & ministry of land infrastructure transport and tourism bicycle safety framework

- 3.4.3.4 Australia- Australian consumer law & AS/NZS bicycle frame standards

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM bicycle safety standards & active mobility framework

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- SASO standards & vision 2030 active mobility initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (camera, LiDAR, RADAR, ultrasonic)

- 3.7.1.2 Sensor fusion & integration

- 3.7.1.3 AI & machine learning in pedestrian detection

- 3.7.2 Emerging technologies

- 3.7.2.1 V2X communication for enhanced detection

- 3.7.2.2 Nighttime & low-light detection technologies

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Key patent trends

- 3.8.2 Technology innovation hotspots

- 3.8.3 Patent filing by key players

- 3.8.4 Emerging IP strategies

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Aluminum frame price trends (2022-2025)

- 3.9.3 Steel frame price trends (2022-2025)

- 3.9.4 Carbon fiber frame price trends (2022-2025)

- 3.9.5 Titanium frame price trends (2022-2025)

- 3.10 Pricing strategy by player type

- 3.10.1 Premium positioning strategy (titanium, high-modulus carbon)

- 3.10.2 Value segment strategy (aluminum, standard carbon)

- 3.10.3 Cost-plus pricing models (OEM manufacturing)

- 3.11 Use cases & success stories

- 3.12 Case studies

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 Design automation & generative engineering

- 3.14.3 Quality control & defect detection systems

- 3.14.4 Demand forecasting & inventory optimization

- 3.15 Risks, limitations & regulatory considerations

- 3.15.1 Data privacy in customer design data

- 3.15.2 AI model reliability in structural engineering

- 3.15.3 Workforce displacement concerns

- 3.16 Future outlook & opportunities

- 3.16.1 Emerging market segments

- 3.16.2 Technology disruptions on the horizon

- 3.16.3 Sustainability trends

- 3.16.4 Business model innovations

- 3.16.5 Long-term growth projections (2030-2040)

- 3.16.6 Strategic recommendations by stakeholder type

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

- 5.4 Carbon Fiber

- 5.5 Titanium

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Frame, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Mountain bicycle

- 6.3 Hybrid bicycle

- 6.4 Electric bicycle

- 6.5 Road bicycle

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Professional/competitive cyclists

- 9.3 Recreational/enthusiast cyclists

- 9.4 Commuters/urban cyclists

- 9.5 Youth cyclists

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Argon 18

- 11.1.2 Bianchi

- 11.1.3 Cannondale Bikes

- 11.1.4 Canyon

- 11.1.5 Cervelo

- 11.1.6 Cicli Pinarello SRL

- 11.1.7 Giant Manufacturing

- 11.1.8 GT Bicycles

- 11.1.9 Kona Bikes

- 11.1.10 Merida

- 11.1.11 Santa Cruz

- 11.1.12 SCOTT Sports

- 11.1.13 Specialized Bicycle

- 11.1.14 Trek

- 11.2 Regional Players

- 11.2.1 Chicago Bicycle Company

- 11.2.2 Ideal Bike

- 11.2.3 Dengfu Sports Equipment

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 Pinion

- 11.3.2 YT Industries

- 11.3.3 Aventon Bikes

自行车车架市场:按材料、应用、车架类型、最终用途和销售管道划分-2026-2032年全球市场预测

自行车车架市场:按材料、应用、车架类型、最终用途和销售管道划分-2026-2032年全球市场预测 自行车车架市场-全球产业规模、份额、趋势、机会、预测:按材料、车架类型、地区和竞争对手划分,2021-2031年

自行车车架市场-全球产业规模、份额、趋势、机会、预测:按材料、车架类型、地区和竞争对手划分,2021-2031年 碳纤维自行车车架:全球市占率及排名、总销售量及需求预测(2025-2031年)

碳纤维自行车车架:全球市占率及排名、总销售量及需求预测(2025-2031年) 自行车车架市场规模、份额和趋势分析报告:2025-2030 年按材料、车架类型、销售管道、分销管道、地区和细分市场进行的预测

自行车车架市场规模、份额和趋势分析报告:2025-2030 年按材料、车架类型、销售管道、分销管道、地区和细分市场进行的预测 全球自行车车架市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球自行车车架市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 自行车车架的全球市场:依方法、类型(电动自行车/非电动自行车)、车架类型、车架材料、应用、製造模式和地区(~2032)

自行车车架的全球市场:依方法、类型(电动自行车/非电动自行车)、车架类型、车架材料、应用、製造模式和地区(~2032)