|

市场调查报告书

商品编码

1998659

骨汤蛋白市场商机、成长要素、产业趋势分析及2026-2035年预测。Bone Broth Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

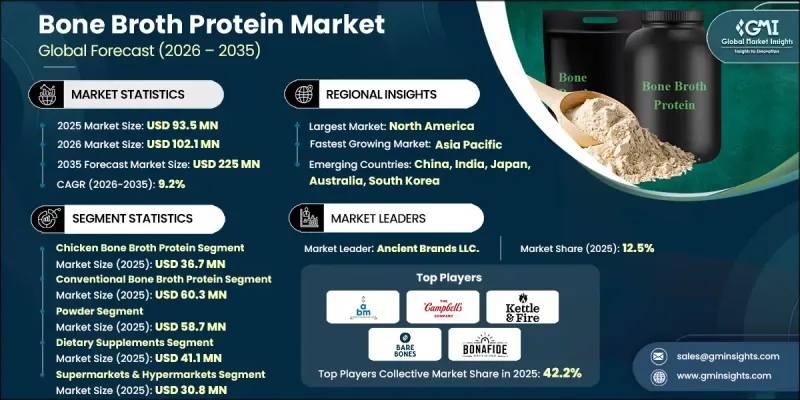

2025 年全球骨汤蛋白市场价值为 9,350 万美元,预计到 2035 年将以 9.2% 的复合年增长率增长至 2.25 亿美元。

骨汤蛋白是一种营养补充剂,它是透过长时间熬煮动物骨骼和结缔组织,提取有益成分而製成的。这种长时间的熬煮过程会释放出天然存在的胶原蛋白、明胶、胺基酸和必需矿物质,然后脱水製成粉末状粉。与许多其他经过深度加工的蛋白质补充剂不同,骨汤蛋白保留了骨汤中许多天然营养成分。因此,作为一种功能性成分,骨汤蛋白在健康和保健领域越来越受到关注,因为它能够支持整体健康的各个方面。消费者越来越重视骨汤蛋白,因为它在关节支持、消化系统健康和皮肤健康方面具有潜在益处。胶原蛋白在维持结缔组织的强度方面发挥着至关重要的作用,而胺基酸则有助于肌肉恢復和新陈代谢。对于那些因不耐受或过敏而避免食用乳製品蛋白的人来说,骨汤蛋白尤其具有吸引力。此外,骨汤蛋白通常经过最少的加工,符合「洁净标示」的趋势。其营养成分也适合以低碳水化合物摄取和消除常见过敏原为优先的饮食模式,进一步扩大了其在寻求天然且易于消化的蛋白质来源的消费者中的吸引力。

| 市场规模 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 9350万美元 |

| 预测金额 | 2.25亿美元 |

| 复合年增长率 | 9.2% |

2025年,传统骨汤蛋白的销售额达到6,030万美元。由于其广泛的供应管道和通常比其他产品类型更高的价格竞争力,该品类持续保持强劲的市场地位。许多消费者选择传统骨汤蛋白,是因为它既能提供胶原蛋白和蛋白质补充剂的营养益处,价格又相对实惠。广泛的零售网路和标准分销管道也促进了其受欢迎程度,尤其受到那些注重成本、寻求功能性营养产品但又不想支付高价的消费者的青睐。

预计到2025年,骨汤蛋白粉的市场规模将达到5,870万美元。骨汤蛋白粉因其保存期限长、储存方便、用途广泛而广受欢迎。消费者喜欢将蛋白粉添加到各种饮料和餐点中,并根据自身饮食需求调整蛋白质摄取量。这种蛋白粉常用于製作冰沙、奶昔、汤和其他食谱,为经常服用蛋白质补充剂的人提供了柔软性。骨汤蛋白粉的便利性和适应性使其在实体店和线上销售管道都占据了重要地位,尤其受到注重健康的消费者和健身爱好者的青睐,他们希望轻鬆补充日常营养。

预计到2035年,北美骨汤蛋白市场规模将达到9,000万美元。消费者对功能性营养产品日益增长的兴趣是该地区市场扩张的主要驱动力。消费者越来越倾向于选择有助于关节健康、皮肤健康和消化健康的营养补充剂,这推动了富含胶原蛋白的蛋白质产品的需求。此外,补充蛋白质已成为许多人日常营养摄取习惯的一部分,进一步提升了骨汤蛋白产品的受欢迎程度。在美国市场,便利产品形式的日益普及也为市场成长提供了助力,这些产品形式旨在满足忙碌的生活方式。随着消费者更加重视效率和便利性,即饮营养饮品和便利产品形式正成为更具吸引力的选择。此外,线上零售平台的扩张显着改善了消费者获取专业营养补充剂的管道,使他们更容易找到并购买骨汤蛋白产品。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 消费者对富含胶原蛋白的机能性食品的兴趣日益浓厚。

- 原始人饮食法和生酮饮食法的传播

- 不含乳製品的替代蛋白的需求

- 产业潜在风险与挑战

- 高昂的生产和采购成本

- 它对素食者和纯素食消费者的吸引力有限。

- 市场机会

- 开发即饮型及便利商店型产品。

- 风味增强和掩味技术的创新

- 新兴健康和保健市场的成长

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 来源

- 未来市场趋势

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依来源划分,2022-2035年

- 鸡骨汤衍生的蛋白质

- 牛汤衍生的蛋白质

- 土耳其骨汤衍生蛋白

- 鱼骨汤衍生的蛋白质

- 猪骨汤衍生的蛋白质

- 其他的

第六章 市场估算与预测:依原料划分,2022-2035年

- 有机骨汤蛋白

- 传统骨汤蛋白

第七章 市场估计与预测:依类型划分,2022-2035年

- 粉末

- 液体/即饮型(RTD)

- 胶囊和片剂

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 营养补充品

- 运动营养

- 饮食

- 宠物食品

- 其他的

第九章 市场估价与预测:依通路划分,2022-2035年

- 超级市场和大卖场

- 健康与专卖零售店

- 线上零售与电子商务

- 药局/药局

- 直接面向消费者 (D2C)

- 便利商店

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十一章:公司简介

- Ancient Brands, LLC.

- The Campbell's Company

- Kettle &Fire

- Bare Bones

- NOW Foods

- LonoLife

- Bonafide Provisions

- Bluebird Provisions

- Kitchen Basics

- FOND Bone Broth LLC

- Organixx

- Essentia Proteins

- Taranaki Bio Extracts(Butler Brand)

The Global Bone Broth Protein Market was valued at USD 93.5 million in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 225 million by 2035.

Bone broth protein is a nutritional supplement produced by slowly cooking animal bones and connective tissues to extract beneficial compounds. This extended preparation process releases naturally occurring collagen, gelatin, amino acids, and essential minerals, which are then dehydrated to create a powdered protein product. Unlike several other protein supplements that undergo heavy processing, bone broth protein retains many of the naturally occurring nutrients traditionally associated with bone broth. As a result, the product has gained attention in the health and wellness sector as a functional ingredient that supports various aspects of overall well-being. Consumers are increasingly valuing bone broth protein for its potential benefits related to joint support, digestive health, and skin health. Collagen plays a key role in maintaining connective tissue strength, while amino acids contribute to muscle recovery and metabolic activity. The product is particularly appealing to individuals who avoid dairy-based proteins due to intolerance or sensitivity. Additionally, bone broth protein aligns well with clean-label preferences because it is typically minimally processed. Its nutritional profile also suits dietary patterns that prioritize low-carbohydrate intake and exclude common allergens, which further expands its appeal among consumers seeking natural and easy-to-digest protein sources.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $93.5 Million |

| Forecast Value | $225 Million |

| CAGR | 9.2% |

The conventional segment generated USD 60.3 million in 2025. This category continues to maintain a strong presence because it is widely accessible and generally priced more competitively than alternative product types. Many consumers choose conventional bone broth protein as it provides the nutritional advantages associated with collagen and protein supplementation while remaining affordable. Its availability through broad retail networks and standard distribution channels also contributes to its widespread adoption, particularly among cost-conscious buyers seeking functional nutrition products without premium pricing.

The powder format reached USD 58.7 million in 2025. Powdered bone broth protein has gained significant popularity due to its long shelf life, convenient storage, and versatile applications. Consumers appreciate the ability to incorporate the powder into a wide variety of beverages and meals, allowing them to adjust protein intake according to personal dietary needs. The format is frequently used in smoothies, shakes, soups, and other recipes, providing flexibility for individuals who consume protein supplements regularly. The convenience and adaptability of powdered bone broth protein have contributed to its strong presence across both physical retail stores and digital sales channels, particularly among health-conscious consumers and fitness enthusiasts seeking convenient daily nutrition options.

North America Bone Broth Protein Market will reach USD 90 million by 2035. Rising interest in functional nutrition products is a major factor supporting market expansion across the region. Consumers are increasingly seeking dietary supplements that contribute to joint support, skin health, and digestive wellness, which has driven demand for collagen-rich protein products. In addition, protein supplementation has become a common part of many daily nutrition routines, further encouraging adoption of bone broth protein products. The market in the United States is also benefiting from the growing popularity of convenient product formats designed for fast-paced lifestyles. As consumers prioritize efficiency and accessibility, ready-to-consume nutritional beverages and convenient product formats are becoming more attractive options. Furthermore, the expansion of online retail platforms has significantly improved access to specialized nutritional supplements, enabling consumers to explore and purchase bone broth protein products more easily.

Key companies operating in the Global Bone Broth Protein Market include Kettle & Fire, Bare Bones, LonoLife, Bluebird Provisions, Bonafide Provisions, Ancient Brands, LLC., NOW Foods, The Campbell's Company, Kitchen Basics, FOND Bone Broth LLC, Organixx, Essentia Proteins, and Taranaki Bio Extracts (Butler Brand). Companies participating in the Bone Broth Protein Market are implementing several strategic initiatives to strengthen their competitive position and expand market reach. Many organizations are prioritizing product innovation by developing new formulations that enhance nutritional content and improve flavor profiles. Investment in research and development is helping manufacturers refine processing techniques and improve product quality while maintaining clean-label standards. Businesses are also expanding their distribution networks through partnerships with retailers, health stores, and digital commerce platforms to increase product accessibility. Branding and marketing strategies that emphasize natural ingredients, functional health benefits, and transparency are becoming increasingly important for attracting health-conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Nature

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 Distribution

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer interest in collagen-rich functional nutrition

- 3.2.1.2 Increasing adoption of paleo and keto lifestyles

- 3.2.1.3 Demand for dairy-free protein alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and sourcing costs

- 3.2.2.2 Limited appeal among vegetarian and vegan consumers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into ready-to-drink and convenience formats

- 3.2.3.2 Innovation in flavor enhancement and masking technologies

- 3.2.3.3 Growth in emerging health and wellness markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Chicken bone broth protein

- 5.3 Beef bone broth protein

- 5.4 Turkey bone broth protein

- 5.5 Fish bone broth protein

- 5.6 Pork bone broth protein

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Nature, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic bone broth protein

- 6.3 Conventional bone broth protein

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder

- 7.3 Liquid/Ready-to-Drink (RTD)

- 7.4 Capsules & Tablets

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Dietary supplements

- 8.3 Sports nutrition

- 8.4 Food & beverages

- 8.5 Pet food

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & hypermarkets

- 9.3 Health & specialty stores

- 9.4 Online retail & e-commerce

- 9.5 Pharmacies & drug stores

- 9.6 Direct-to-consumer (D2C)

- 9.7 Convenience stores

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Ancient Brands, LLC.

- 11.2 The Campbell's Company

- 11.3 Kettle & Fire

- 11.4 Bare Bones

- 11.5 NOW Foods

- 11.6 LonoLife

- 11.7 Bonafide Provisions

- 11.8 Bluebird Provisions

- 11.9 Kitchen Basics

- 11.10 FOND Bone Broth LLC

- 11.11 Organixx

- 11.12 Essentia Proteins

- 11.13 Taranaki Bio Extracts (Butler Brand)