|

市场调查报告书

商品编码

1998663

男性应力性尿失禁市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Male Stress Urinary Incontinence Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

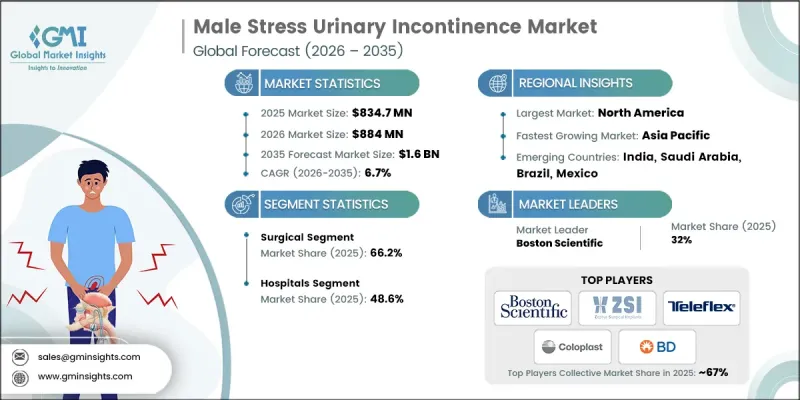

预计到 2025 年,全球男性应力性尿失禁市场价值将达到 8.347 亿美元,年复合成长率为 6.7%,到 2035 年将达到 16 亿美元。

市场成长主要受前列腺癌发病率上升、男性应力性尿失禁(SUI)盛行率增加以及医疗设备和外科手术技术的持续创新所驱动。由于摄护腺癌仍然是男性最常见的癌症之一,治疗后出现尿失禁併发症的患者人数持续成长。全球男性人口老化加剧,进一步推高了尿失禁的诊断率,并导致尿失禁管理需求增加。随着人们对治疗后泌尿系统併发症的认识不断提高,对侵入性和非侵入性治疗方案的需求也在稳步增长。该市场涵盖了专门用于治疗因身体用力引起的尿失禁的专业医疗技术。主要产品类型包括人工尿道括约肌和男性用吊带系统,旨在恢復尿失禁功能并显着提高患者的生活品质。此外,泌尿系统专科医疗中心的扩张以及新一代人工尿道括约肌设计的进步,正在推动该行业的长期需求。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 8.347亿美元 |

| 预测金额 | 16亿美元 |

| 复合年增长率 | 6.7% |

预计到2025年,手术治疗将占总治疗量的66.2%,这主要得益于门诊和日间手术中心手术量的增加。手术仍然是中重度男性压力性尿失禁(SUI)的首选治疗方法。人工尿道括约肌系统因其长期疗效显着且排尿控制效果稳定,广受认可为临床治疗的标竿。男性用吊带系统也是重要的治疗选择,尤其适用于症状较轻微且尿道功能尚存的患者。临床指引和既定的治疗通讯协定持续推动手术治疗在整个医疗体系中的普及。

到2025年,医院通路将占48.6%的市占率。这些机构是进行复杂外科手术(包括尿道括约肌植入术)的主要中心,这些手术需要经验丰富的外科团队和先进的手术设施。医院泌尿系统经常处理更复杂的术后尿失禁病例,并透过多学科协作提供全面的患者照护。即使门诊手术模式不断发展,医院仍然是提供先进的男性压力性尿失禁治疗的核心。

预计到2025年,北美男性应力性尿失禁市场份额将达到46.6%,并有望在预测期内保持稳定成长。该地区市场扩张的驱动因素包括前列腺相关治疗后尿失禁问题日益受到关注,以及先进治疗技术的普及率较高。完善的泌尿系统基础设施提升了患者获得治疗的便利性,实现了快速诊断、系统化的转诊途径,并提供了手术和保守治疗方案。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 影响产业的因素

- 成长驱动因素

- 男性应力性尿失禁盛行率增加(主要见于接受根治性摄护腺切除术的患者)

- 医疗设备和外科手术技术的进步

- 摄护腺癌发生率增加

- 产业潜在风险与挑战

- 高昂的手术费用

- 机会

- 大量未接受治疗的中度至重度压力性尿失禁患者

- 成长驱动因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 消费者洞察

- 投资环境

- 2025年各地区手术数量

- 男性用吊带

- 人工尿道括约肌(AUS)

- 以严重程度分類的尿失禁流行病学状况

- 波特五力分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 外科

- 人工尿道括约肌(AUS)

- 男性用吊带

- 可调节尿失禁气囊

- 非手术

- 保险套导尿管

- 阴茎夹

第六章 市场估算与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 泌尿系统诊所

- 其他最终用户

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章:公司简介

- AMI GmbH

- Becton, Dickinson and Company

- Boston Scientific

- CL Medical

- Coloplast

- Neomedic

- Promedon

- Rigicon, Inc.

- Teleflex

- Zephyr Surgical Implants(ZSI)

The Global Male Stress Urinary Incontinence Market was valued at USD 834.7 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 1.6 billion by 2035.

Market growth is fueled by the rising incidence of prostate cancer, the increasing prevalence of male stress urinary incontinence (SUI), and continuous innovation in medical devices and surgical procedures. As prostate cancer remains one of the most frequently diagnosed cancers among men, the number of patients experiencing urinary control complications following treatment continues to grow. The expanding aging male population worldwide further contributes to higher diagnosis rates and subsequent incontinence management needs. As awareness surrounding post-treatment urinary complications improves, demand for both interventional and non-invasive management solutions is steadily increasing. The market encompasses specialized medical technologies developed to manage involuntary urine leakage associated with physical exertion. Core product categories include artificial urinary sphincters and male sling systems designed to restore continence and significantly enhance patient quality of life. Additionally, the expansion of urology-focused specialty centers and the advancement of next-generation artificial urinary sphincter designs are reinforcing long-term industry demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $834.7 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 6.7% |

The surgical treatment segment held a 66.2% share in 2025, supported by the growing number of outpatient and ambulatory surgical center-based procedures. Surgical intervention remains the preferred approach for moderate to severe male SUI cases. Artificial urinary sphincter systems are widely recognized as the clinical benchmark due to their strong long-term efficacy data and consistent continence outcomes. Male sling systems also represent an important therapeutic option, particularly for patients with less severe symptoms and preserved urethral function. Clinical recommendations and established treatment protocols continue to reinforce surgical adoption rates across healthcare systems.

The hospitals segment captured 48.6% share in 2025. These institutions serve as primary centers for complex surgical procedures, including artificial urinary sphincter implantation, which requires experienced surgical teams and advanced operating facilities. Hospital-based urology departments frequently manage more complicated post-treatment incontinence cases and provide comprehensive patient care through multidisciplinary collaboration. Even as outpatient surgical models expand, hospitals remain central to delivering advanced male SUI interventions.

North America Male Stress Urinary Incontinence Market held 46.6% share in 2025 and is expected to witness steady growth throughout the forecast period. Regional expansion is supported by strong awareness of urinary incontinence following prostate-related treatments and high adoption of advanced therapeutic technologies. A well-established urology infrastructure enables timely diagnosis, structured referral pathways, and access to both surgical and conservative management strategies, strengthening overall treatment accessibility.

Key companies operating in the Global Male Stress Urinary Incontinence Market include Boston Scientific, Coloplast, Becton, Dickinson and Company, Teleflex, and A.M.I. GmbH, Promedon, Rigicon, Inc., Zephyr Surgical Implants (ZSI), Neomedic, and CL Medical. These organizations compete through technological innovation, clinical validation, and expansion of global distribution networks. Companies in the Global Male Stress Urinary Incontinence Market are strengthening their competitive positions through continuous product development and clinical research investments. Manufacturers are focusing on enhancing device durability, ease of implantation, and patient comfort to improve long-term treatment outcomes. Strategic partnerships with urology centers and surgeon training programs help expand procedural adoption and build physician confidence. Firms are also pursuing geographic expansion strategies to penetrate emerging markets while reinforcing their presence in established regions. Regulatory compliance, post-market surveillance programs, and real-world clinical data generation further strengthen brand credibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of male stress urinary incontinence (post-prostatectomy dominance)

- 3.2.1.2 Technological advancements in devices and surgical techniques

- 3.2.1.3 Growing incidence of prostate cancer

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procedural cost

- 3.2.3 Opportunities

- 3.2.3.1 Large untreated moderate-to-severe SUI population

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Consumer insights

- 3.7 Investment landscape

- 3.8 Number of procedures, by region, 2025

- 3.8.1 Male slings

- 3.8.2 Artificial urinary sphincters (AUS)

- 3.9 Epidemiology scenario by severity of incontinence

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical

- 5.2.1 Artificial Urinary Sphincter (AUS)

- 5.2.2 Male slings

- 5.2.3 Adjustable continence balloons

- 5.3 Non-Surgical

- 5.3.1 Condom catheters

- 5.3.2 Penile clamps

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Urology clinics

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 A.M.I. GmbH

- 8.2 Becton, Dickinson and Company

- 8.3 Boston Scientific

- 8.4 CL Medical

- 8.5 Coloplast

- 8.6 Neomedic

- 8.7 Promedon

- 8.8 Rigicon, Inc.

- 8.9 Teleflex

- 8.10 Zephyr Surgical Implants (ZSI)