|

市场调查报告书

商品编码

1998678

兽医电子病历市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Veterinary EHR Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

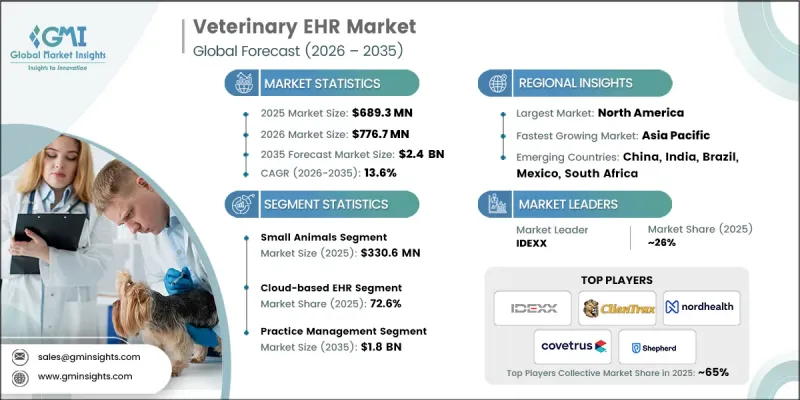

预计到 2025 年,全球兽医电子健康记录 (EHR) 市场价值将达到 6.893 亿美元,年复合成长率为 13.6%,预计到 2035 年将达到 24 亿美元。

随着兽医医院和诊所加速采用数位化技术以提高营运效率和患者照护,兽医电子病历(EHR)市场呈现强劲成长动能。人们对动物预防医学日益增长的兴趣、与饲主沟通的加强以及远距医疗能力的提升,正在推动兽医医院病历管理系统的现代化。向数位化解决方案的转型使兽医医院能够更有效率地管理大量临床讯息,同时改善兽医团队与饲主之间的协作。发展中地区数位平台的日益普及也促进了产业成长,使兽医专业人员能够更方便地使用简化临床管理的软体工具。同时,透过持续投资于诊断设备整合、影像设备整合和财务处理解决方案的软体开发,兽医EHR平台的技术能力也在不断增强。云端技术的进步和兽医系统间互通性也有助于诊所更有效地管理病患资料。人们对动物健康和福祉的日益关注,进一步促进了数位记录系统的普及,从而支持了全球兽医电子健康记录市场的长期成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 6.893亿美元 |

| 预测金额 | 24亿美元 |

| 复合年增长率 | 13.6% |

兽医电子健康记录 (EHR) 系统作为数位平台,旨在储存和管理动物健康讯息,同时支援兽医机构的临床运作。这些平台将病历、治疗记录和管理数据整合到一个集中式系统中,帮助兽医更有效率地监测动物健康状况。除了改善记录组织方式外,兽医 EHR 系统还透过与实验室服务、影像系统和客户沟通管道集成,简化工作流程。动物慢性病盛行率的不断上升也推动了对数位记录管理系统的需求成长。长期健康状况通常需要持续监测、治疗协调和详细记录,因此数位记录系统对于有效的护理管理至关重要。

2025年,小型动物市场规模达3.306亿美元。该市场保持主导的主要原因是宠物数量持续增长以及对专业兽医服务的需求不断增加。治疗宠物的兽医诊所高度依赖电子健康记录(EHR)来管理病患资讯、治疗方案和后续护理需求。透过使用EHR平台,兽医专业人员可以维护有序的病历、追踪预防保健计划并更有效地监测治疗效果。随着宠物饲主对兽医护理和动物保健管理的要求越来越高,动物医院正在采用先进的数位系统来支援高效的病患记录管理。小型动物专科医院和诊所正在利用EHR的功能来简化行政任务、管理医疗记录并提高诊所的整体工作流程效率。

到2025年,基于云端的电子病历(EHR)解决方案将占据72.6%的市场。随着兽医院寻求灵活且经济高效的病患资料管理技术解决方案,基于云端的系统越来越受欢迎。这些平台使兽医专业人员能够远端存取关键的健康讯息,从而加强兽医团队之间的协作,并加快临床决策速度。此外,基于云端的部署减少了对大规模本地IT基础设施的需求,并降低了兽医院的营运成本。这些系统还提供自动更新、增强的网路安全保护和安全的资料备份功能,从而满足监管合规性和资料保护要求。远距医疗和行动兽医服务的日益普及进一步加速了基于云端的EHR平台的采用。

预计到2025年,北美兽医电子病历(EHR)市占率将达到40%,并在2035年之前以13.4%的复合年增长率成长。北美市场成长的主要驱动力是兽医诊所和医院积极采用数位化医疗技术。宠物拥有率高以及对先进兽医服务的需求不断增长,并持续推动数位化健康管理系统的应用。该地区的兽医专业人员正越来越多地采用EHR平台,以简化临床工作流程、改善数据存取并支援更有效率的患者照护管理。美国是该地区的主要市场,因为其拥有大量需要持续医疗监测和系统健康记录的伴侣动物。美国和加拿大的兽医机构正在迅速转向基于云端的解决方案,以增强诊断资讯的整合、改善与饲主的沟通并支援不断发展的远端医疗服务模式。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 影响产业的因素

- 成长驱动因素

- 宠物饲养量增加

- 对先进兽医护理的需求日益增长

- 将远端医疗融入兽医实践

- 产业潜在风险与挑战

- 高昂的实施和维护成本

- 网路安全与资料外洩风险

- 市场机会

- 兽医院云端电子病历系统应用扩展

- 整合人工智慧驱动的诊断和工作流程自动化工具

- 成长驱动因素

- 成长潜力分析

- 监理情势(基于初步调查)

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 北美洲

- 科技趋势

- 目前技术

- 新兴技术

- 未来市场趋势(基于初步研究)

- 人工智慧/基因工程:人工智慧的影响(基于初步研究)

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依服务类型划分,2022-2035年

- 小动物

- 混合治疗

- 马

- 用于肉类的牲畜

- 其他医学领域

第六章 市场估算与预测:以交付方式划分,2022-2035年

- 基于云端的电子健康记录

- 本地部署的电子健康记录系统

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 医疗管理

- 诊断影像

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 兽医医院和诊所

- 移动兽医诊所/移动动物医院

- 其他最终用户

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- AcuroVet

- Animal Intelligence Software

- ClienTrax

- Covetrus

- DaySmart Software

- Digitail

- IDEXX

- Instinct Science

- Nordhealth

- Onward

- OSP

- Shepherd Veterinary Software

The Global Veterinary EHR Market was valued at USD 689.3 million in 2025 and is estimated to grow at a CAGR of 13.6% to reach USD 2.4 billion by 2035.

The veterinary EHR market is gaining strong momentum as veterinary clinics and hospitals increasingly adopt digital technologies to improve operational efficiency and patient care. Growing attention to preventive animal healthcare, enhanced client communication, and remote consultation capabilities is encouraging veterinary practices to modernize their record-keeping systems. The shift toward digital solutions allows clinics to manage large volumes of clinical information more efficiently while improving coordination between veterinary teams and pet owners. Expanding availability of digital platforms in developing regions is also supporting industry growth, as veterinary professionals gain greater access to software-based tools that streamline practice management. At the same time, ongoing investment in software development for diagnostic integration, imaging connectivity, and financial processing solutions is strengthening the technological capabilities of veterinary EHR platforms. Improvements in cloud-based technologies and better interoperability between veterinary healthcare systems are also helping clinics manage patient data more effectively. Rising awareness regarding animal health and wellness further contributes to increased adoption of digital record systems, supporting long-term expansion of the veterinary EHR market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $689.3 Million |

| Forecast Value | $2.4 Billion |

| CAGR | 13.6% |

Veterinary electronic health record systems function as digital platforms designed to store and manage animal health information while supporting clinical operations within veterinary facilities. These platforms consolidate patient histories, treatment records, and administrative data into a centralized system that helps veterinary professionals monitor health conditions more efficiently. In addition to improving record organization, veterinary EHR systems enhance workflow efficiency by integrating with laboratory services, diagnostic imaging systems, and client communication channels. The growing occurrence of chronic health conditions among animals is also contributing to the rising demand for digital record management systems. Long-term health conditions often require continuous monitoring, treatment adjustments, and detailed documentation, making digital record systems essential for effective care management.

The small animals segment generated USD 330.6 million in 2025. This segment maintains a dominant position largely due to the steady increase in companion animal ownership and the growing demand for specialized veterinary services. Veterinary practices treating companion animals rely heavily on digital health records to manage patient information, treatment plans, and ongoing care requirements. The use of EHR platforms allows veterinary professionals to maintain organized medical histories, track preventive care schedules, and monitor treatment outcomes more effectively. As pet owners increasingly seek higher standards of veterinary care and improved medical management for their animals, veterinary clinics are adopting advanced digital systems that support efficient patient record management. Small animal veterinary hospitals and clinics benefit from EHR features that streamline administrative tasks, manage medical records, and improve overall workflow efficiency within the practice.

The cloud-based EHR solutions segment held a 72.6% share in 2025. The popularity of cloud-based systems continues to grow as veterinary clinics seek flexible and cost-effective technology solutions for managing patient data. These platforms allow veterinary professionals to access critical health information remotely, enabling improved collaboration among veterinary teams and faster decision-making in clinical environments. Cloud-based deployment also reduces the need for extensive on-site IT infrastructure, which lowers operational costs for veterinary facilities. In addition, these systems provide automated updates, enhanced cybersecurity protections, and secure data backup capabilities that support regulatory compliance and data protection requirements. The increasing popularity of remote consultations and mobile veterinary services has further accelerated the adoption of cloud-based EHR platforms.

North America Veterinary EHR Market accounted for 40% share in 2025 and is projected to grow at a CAGR of 13.4% throughout 2035. Market growth in North America is supported by strong adoption of digital healthcare technologies across veterinary clinics and hospitals. High levels of companion animal ownership and increasing demand for advanced veterinary services continue to encourage the use of digital health management systems. Veterinary professionals across the region are increasingly implementing EHR platforms to streamline clinical workflows, improve data accessibility, and support more efficient patient care management. The United States represents the leading market within the region due to the large population of companion animals requiring consistent medical monitoring and well-structured health records. Veterinary facilities in both the United States and Canada are rapidly transitioning toward cloud-based solutions that enhance diagnostic integration, improve communication with pet owners, and support evolving telehealth service models.

Prominent companies operating in the Global Veterinary EHR Market include IDEXX, Covetrus, Digitail, DaySmart Software, Shepherd Veterinary Software, Nordhealth, Instinct Science, ClienTrax, AcuroVet, Animal Intelligence Software, OSP, and Onward. Companies participating in the Global Veterinary EHR Market are implementing multiple strategies to strengthen their competitive position and expand their global presence. Many organizations are prioritizing software innovation by enhancing platform functionality, improving user interfaces, and integrating advanced diagnostic and practice management tools within their systems. Expanding cloud-based capabilities remains a key focus, enabling veterinary clinics to access secure and scalable digital platforms. Strategic partnerships with veterinary clinics, hospitals, and diagnostic service providers help companies broaden their customer base and improve interoperability between healthcare systems. Businesses are also investing in artificial intelligence, data analytics, and automated workflow solutions to improve clinical decision-making and operational efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Practice type trends

- 2.2.3 Delivery mode trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing pet adoption rates

- 3.2.1.2 Growing demand for advanced veterinary care

- 3.2.1.3 Integration of telemedicine in veterinary practices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and maintenance costs

- 3.2.2.2 Cybersecurity and data breach risks

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of cloud based EHR adoption in veterinary clinics

- 3.2.3.2 Integration of AI powered diagnostic and workflow automation tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technology

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI/GEN AI (Driven by primary research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Practice Type, 2022-2035 ($ Mn)

- 5.1 Key trends

- 5.2 Small animals

- 5.3 Mixed animals

- 5.4 Equine

- 5.5 Food-producing animals

- 5.6 Other practice types

Chapter 6 Market Estimates and Forecast, By Delivery Mode, 2022-2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cloud-based EHR

- 6.3 On-premise EHR

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 ($ Mn)

- 7.1 Key trends

- 7.2 Practice management

- 7.3 Imaging

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 Ambulatory and mobile veterinary practices

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AcuroVet

- 10.2 Animal Intelligence Software

- 10.3 ClienTrax

- 10.4 Covetrus

- 10.5 DaySmart Software

- 10.6 Digitail

- 10.7 IDEXX

- 10.8 Instinct Science

- 10.9 Nordhealth

- 10.10 Onward

- 10.11 OSP

- 10.12 Shepherd Veterinary Software