|

市场调查报告书

商品编码

1998681

2026 年至 2035 年足踝医疗设备市场的商业机会、成长要素、产业趋势与预测。Foot and Ankle Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

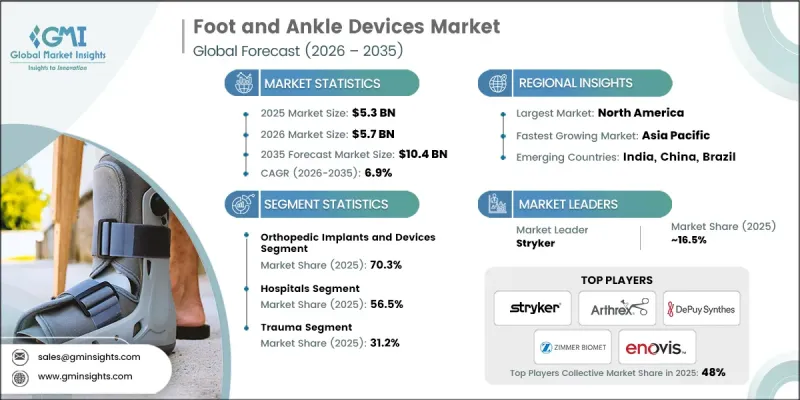

预计到 2025 年,全球足踝医疗设备市场价值将达到 53 亿美元,并预计以 6.9% 的复合年增长率成长,到 2035 年达到 104 亿美元。

整形外科疾病发生率上升、创伤病例增加以及足踝医疗设备技术的进步是推动该市场成长的主要因素。糖尿病患者数量及其相关足部併发症的增加,加上患者客製化植入和微创手术的创新发展,正在加速市场需求。老化和生活方式相关的风险因素也加剧了足踝疾病的发生。此外,全球交通事故和高能量创伤病例的增加,也推动了对用于治疗骨折、韧带断裂、脱位和其他下肢损伤的医疗设备的需求。包括材料科学和医疗设备工程在内的技术创新,正在显着改善患者的治疗效果,进一步促进市场扩张。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 53亿美元 |

| 预计金额 | 104亿美元 |

| 复合年增长率 | 6.9% |

预计到2025年,整形外科植入和医疗设备领域将占据70.3%的市场。这一增长主要得益于3D列印整形外科植入的应用以及创伤、畸形矫正和退化性关节疾病手术量的激增。骨科植入仍是治疗足踝疾病(包括创伤固定、关节重组和畸形矫正)的主要选择。下肢骨折、糖尿病足併发症、老龄化相关性肌肉骨骼退化以及运动伤害的发生率不断上升,正在推动全球整形外科植入物的需求。

预计到2025年,门诊手术中心(ASC)市场规模将达到13亿美元,并在2026年至2035年间以6.7%的复合年增长率成长。门诊手术中心受益于整形外科和微创手术转移到门诊的全球趋势。麻醉、疼痛管理和手术器械的进步使得门诊手术中心能够安全地进行拇趾滑液囊炎矫正、韧带重组和内固定等手术,推动了市场成长。

美国足踝医疗设备市场预计到2025年将达到26亿美元。这一增长主要得益于个人化植入的研发、完善的医疗基础设施、大量的手术量、全面的医保报销机制、积极的研发投入以及便捷的整形外科专家资源。美国在创新方面也处于领先地位,诸如全踝关节置换系统、先进的固定螺丝、人工软骨植入和外固定架等新技术,通常在进入全球市场之前,先在国内进行临床检验。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策及对资料完整性的承诺

- 资讯来源一致性通讯协定

- GMI人工智慧政策及对资料完整性的承诺

- 调查过程和可靠性评分

- 研究路径的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 整形外科疾病盛行率增加

- 创伤和交通事故发生率增加

- 足踝装置的技术进步

- 产业潜在风险与挑战

- 足部及踝部医疗设备高成本

- 熟练医护人员短缺

- 机会

- 数位健康与智慧矫正器具的融合

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 北美洲

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 救赎方案

- 北美洲

- 欧洲

- 亚太地区

- 消费行为分析

- 环形天线固定器竞争格局分析(依公司划分)

- 六足机器人类别及技术差异化

- 产品特定价格趋势

- 差距分析

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 打击者公司

- 德普合成(强生公司)

- Earthrex有限公司

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 整形外科植入和医疗设备

- 关节移植

- 足关节移植

- 其他关节移植

- 固定装置

- 内固定装置

- 盘子

- 拧紧

- 固定钉

- 其他内部固定装置

- 外固定装置

- 环形固定係统

- 销钉桿系统

- 六足系统

- 其他外固定装置

- 内固定装置

- 软组织整形外科器械

- 关节移植

- 矫正器具和支撑装置

- 柔性矫正器具和支撑器具

- 刚性矫正器具和支撑装置

- 铰炼式矫正器具和支撑器具

- 义肢

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 创伤

- 锤状趾

- 骨关节炎

- 类风湿性关节炎

- 神经系统疾病

- 骨质疏鬆症

- 其他用途

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 整形外科诊所

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- aap implantate AG

- Acumed LLC

- Arthrex, Inc.

- CONMED Corporation

- DePuy Synthes(Johnson & Johnson)

- Embla Medical Corporation

- Enovis Corporation

- Fillauer LLC

- Medartis

- Orthofix Medical Inc.

- Ottobock SE & Co KGaA

- Smith & Nephew plc

- Stryker Corporation

- VILEX, LLC

- Zimmer Biomet Holdings, Inc.

The Global Foot and Ankle Devices Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 10.4 billion by 2035.

The market's growth is driven by the rising prevalence of orthopedic disorders, an increasing number of trauma cases, and advancements in foot and ankle device technologies. A growing diabetic population with related foot complications, coupled with the development of patient-specific implants and minimally invasive surgical innovations, is accelerating demand. Aging populations and lifestyle-related risk factors are also contributing to the rise in foot and ankle disorders. Furthermore, the global increase in road traffic accidents and high-impact trauma cases is boosting the need for devices that manage fractures, ligament tears, dislocations, and other lower extremity injuries. Technological innovation, including improvements in material science and device engineering, has significantly enhanced patient outcomes, further supporting market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 6.9% |

The orthopedic implants and devices segment held 70.3% share in 2025. Growth is being fueled by the adoption of 3D-printed orthopedic implants and the high procedural volume for trauma, deformity correction, and degenerative joint conditions. Orthopedic implants remain the primary treatment option for surgical management of foot and ankle conditions, including trauma fixation, joint reconstruction, and deformity correction. Rising incidences of lower extremity fractures, diabetes-related foot complications, age-related musculoskeletal degeneration, and sports injuries are driving demand globally.

The ambulatory surgical centers (ASCs) segment was valued at USD 1.3 billion in 2025 and is expected to grow at a CAGR of 6.7% during 2026-2035. ASCs are benefiting from the global shift toward outpatient orthopedic surgeries and minimally invasive procedures. Technological advancements in anesthesia, pain management, and surgical instrumentation have enabled ASCs to perform procedures such as bunion corrections, ligament reconstructions, and fixation surgeries safely in outpatient settings, supporting market growth.

U.S. Foot and Ankle Devices Market was valued at USD 2.6 billion in 2025. Growth is supported by the development of patient-specific implants, well-established healthcare infrastructure, high procedure volumes, comprehensive reimbursement frameworks, robust R&D activities, and accessible orthopedic specialists. The U.S. is also a leader in innovation, with new technologies such as total ankle replacement systems, advanced fixation screws, synthetic cartilage implants, and external fixation frames often launched and clinically validated domestically before global commercialization.

Prominent companies in the Global Foot and Ankle Devices Market include Acumed LLC, Embla Medical Corporation, Enovis Corporation, Arthrex, Inc., Medartis, Smith & Nephew plc, Stryker Corporation, VILEX, LLC, Zimmer Biomet Holdings, Inc., DePuy Synthes (Johnson & Johnson), CONMED Corporation, Ottobock SE & Co KGaA, Fillauer LLC, and aap implantate AG. Companies in the Global Foot and Ankle Devices Market strengthen their position by investing heavily in R&D for patient-specific implants, advanced fixation systems, and minimally invasive solutions. They pursue strategic partnerships with hospitals, surgical centers, and orthopedic clinics to integrate their devices into standard care pathways. Expanding geographically into emerging markets helps tap into growing patient populations. Firms also focus on product differentiation through innovative materials, 3D printing, and smart implant technologies. Comprehensive after-sales support, physician training programs, and collaborations with research institutions further solidify their market presence and enhance brand credibility.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of orthopedic disorders

- 3.2.1.2 Rising incidence of trauma and road accidents

- 3.2.1.3 Technological advancements in foot and ankle devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of foot and ankle devices

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.3 Opportunities

- 3.2.3.1 Integration of digital health and smart orthotics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Consumer behavior analysis

- 3.9 Ring fixator competitive mapping, by company

- 3.10 Hexapod categories and technology differentiation

- 3.11 Price trends, by products

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.1.1 Stryker Corporation

- 4.1.2 DePuy Synthes (Johnson & Johnson)

- 4.1.3 Arthrex Inc.

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Orthopedic implants and devices

- 5.2.1 Joint implants

- 5.2.1.1 Ankle implants

- 5.2.1.2 Other joint implants

- 5.2.2 Fixation devices

- 5.2.2.1 Internal fixation devices

- 5.2.2.1.1 Plates

- 5.2.2.1.2 Screws

- 5.2.2.1.3 Fusion nails

- 5.2.2.1.4 Other internal fixation devices

- 5.2.2.2 External fixation devices

- 5.2.2.2.1 Ring fixation systems

- 5.2.2.2.2 Pin-to-bar systems

- 5.2.2.2.3 Hexapod systems

- 5.2.2.2.4 Other external fixators

- 5.2.2.1 Internal fixation devices

- 5.2.3 Soft tissue orthopedic devices

- 5.2.1 Joint implants

- 5.3 Bracing and support devices

- 5.3.1 Soft bracing & support devices

- 5.3.2 Hard braces & support devices

- 5.3.3 Hinged braces & support devices

- 5.4 Prostheses

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma

- 6.3 Hammertoe

- 6.4 Osteoarthritis

- 6.5 Rheumatoid Arthritis

- 6.6 Neurological Disorders

- 6.7 Osteoporosis

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Orthopedic clinics

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 aap implantate AG

- 9.2 Acumed LLC

- 9.3 Arthrex, Inc.

- 9.4 CONMED Corporation

- 9.5 DePuy Synthes (Johnson & Johnson)

- 9.6 Embla Medical Corporation

- 9.7 Enovis Corporation

- 9.8 Fillauer LLC

- 9.9 Medartis

- 9.10 Orthofix Medical Inc.

- 9.11 Ottobock SE & Co KGaA

- 9.12 Smith & Nephew plc

- 9.13 Stryker Corporation

- 9.14 VILEX, LLC

- 9.15 Zimmer Biomet Holdings, Inc.

足踝支援市场:按类型、材料、价格范围、应用、最终用户和分销管道划分-2026-2032年全球市场预测

足踝支援市场:按类型、材料、价格范围、应用、最终用户和分销管道划分-2026-2032年全球市场预测 2026年全球足踝器材市场报告

2026年全球足踝器材市场报告 足踝医疗设备市场-全球产业规模、份额、趋势、机会及预测(依产品类型、手术、应用、最终用户、地区及竞争格局划分),2021-2031年踝关节融合板市场 - 全球产业规模、份额、趋势、机会及预测(按骨折部位、骨折类型、最终用户、地区和竞争格局划分,2021-2031年)3D列印踝足矫正器具市场:按技术、材料、客製化程度、经营模式、最终用户和应用划分,全球预测(2026-2032年)儿童踝关节矫正器具市场按产品类型、材质类型、应用、最终用户和分销管道划分-2026-2032年全球预测足部手术復健鞋市场(按产品类型、材质、足部部位、闭合方式、最终用户和分销管道划分),全球预测,2026-2032年铰链踝关节矫正器具市场:按铰链类型、材质、患者类型、通路和最终用户划分 - 全球预测 2026-2032

足踝医疗设备市场-全球产业规模、份额、趋势、机会及预测(依产品类型、手术、应用、最终用户、地区及竞争格局划分),2021-2031年踝关节融合板市场 - 全球产业规模、份额、趋势、机会及预测(按骨折部位、骨折类型、最终用户、地区和竞争格局划分,2021-2031年)3D列印踝足矫正器具市场:按技术、材料、客製化程度、经营模式、最终用户和应用划分,全球预测(2026-2032年)儿童踝关节矫正器具市场按产品类型、材质类型、应用、最终用户和分销管道划分-2026-2032年全球预测足部手术復健鞋市场(按产品类型、材质、足部部位、闭合方式、最终用户和分销管道划分),全球预测,2026-2032年铰链踝关节矫正器具市场:按铰链类型、材质、患者类型、通路和最终用户划分 - 全球预测 2026-2032 踝关节医疗设备市场规模、份额及成长分析(按类型、应用、最终用途和地区划分)-2026-2033年产业预测

踝关节医疗设备市场规模、份额及成长分析(按类型、应用、最终用途和地区划分)-2026-2033年产业预测 踝关节重组器材市场规模、份额和趋势分析报告:按应用、最终用途、地区和细分市场预测(2025-2033 年)

踝关节重组器材市场规模、份额和趋势分析报告:按应用、最终用途、地区和细分市场预测(2025-2033 年)