|

市场调查报告书

商品编码

1998684

电池隔膜市场机会、成长要素、产业趋势分析及2026-2035年预测。Battery Separators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

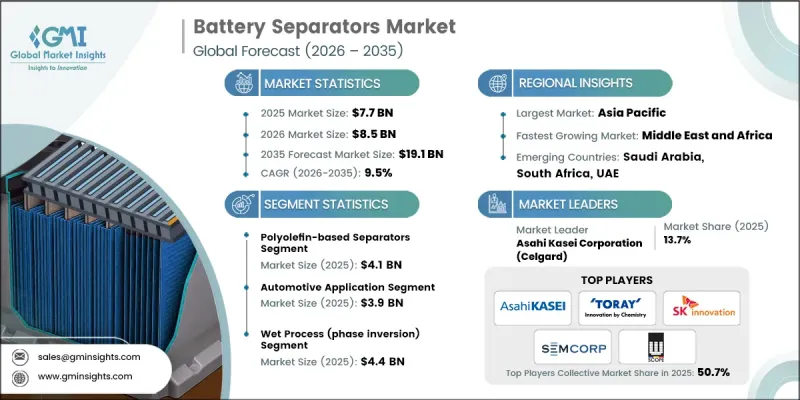

全球电池隔膜市场预计到 2025 年价值 77 亿美元,预计到 2035 年将以 9.5% 的复合年增长率增长至 191 亿美元。

市场成长的驱动力来自于电动车、家用电子电器和工业应用领域对高性能、安全储能解决方案日益增长的需求。电池隔膜作为一种薄膜,能够防止正负极之间直接接触,同时允许离子在正负极之间流动,从而确保安全运行并防止可能导致过热或电池故障的短路。这些隔膜通常由聚乙烯、聚丙烯和复合材料等聚合物材料製成,旨在维持锂离子电池、铅酸电池和镍氢电池的热稳定性、耐化学性和机械强度。采用陶瓷涂层和奈米结构的高级隔膜可提高热稳定性和电解润湿性,而超薄设计则可降低内阻,从而在不影响安全性的前提下实现更高的输出功率。对高能量密度电池、快速充电功能和柔性穿戴应用的需求不断增长,进一步加速了全球技术的进步和应用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 77亿美元 |

| 预测金额 | 191亿美元 |

| 复合年增长率 | 9.5% |

预计到2025年,聚烯隔膜市场规模将达41亿美元,优势在于价格实惠且化学稳定性佳。同时,由于陶瓷涂层隔膜和聚合物涂层隔膜具有更佳的热保护性能和更高的安全性,市场需求也不断成长。芳香聚酰胺和不织布隔膜因其优异的性能和长寿命,在高性能电池中的应用日益广泛。静电纺丝隔膜作为尖端材料,正逐渐成为支持高能量密度、快速充电和柔性电池应用的新兴材料。

预计到2025年,锂离子电池隔膜市场规模将达到10亿美元,反映出其在电动车、能源储存系统和家用电子电器的广泛应用。铅酸电池隔膜因其成本效益和可靠的性能,在汽车起动电池和工业备用电源应用中仍然至关重要。

受电动车普及、超级工厂建设、供应链重组以及政府主导的电池製造扶持政策等因素的推动,北美电池隔膜市场预计将从2025年的10亿美元增长到2035年的27亿美元。高安全性隔膜和全固体隔膜的研发正在将该地区打造成为下一代储能解决方案的中心。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 消费者对富含胶原蛋白的机能性食品的兴趣日益浓厚

- 原始人饮食法和生酮饮食法的传播

- 对不含乳製品的蛋白质替代品的需求

- 产业潜在风险与挑战

- 高昂的生产和采购成本

- 它对素食者和纯素食消费者的吸引力有限。

- 市场机会

- 拓展至即饮饮品及便利商店领域

- 风味增强和掩味技术的创新

- 新兴健康和保健市场的成长

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 来源

- 未来市场趋势

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依材料类型划分,2022-2035年

- 聚烯分离器

- 聚丙烯(PP)隔膜

- 聚乙烯(PE)隔膜

- 多层PP/PE/PP隔膜

- 陶瓷涂层隔膜

- 氧化铝(Al₂O₃)涂层隔膜

- 二氧化硅(SiO2)涂层隔膜

- 氧化锆(ZrO2)涂层隔膜

- 博米特涂层分离器

- 聚合物涂层隔膜

- PVDF涂层隔膜

- PMMA涂层隔膜

- PVA涂层隔膜

- 芳香聚酰胺分离器

- 芳香聚酰胺奈米纤维(ANF)隔膜

- 间位芳香聚酰胺不织布隔膜

- 对位芳香聚酰胺复合隔膜

- 不织布隔膜

- 纤维素基不织布隔膜

- PET不织布隔膜

- 玻璃纤维不织布隔膜

- 静电纺丝分离器

- 奈米纤维静电纺丝膜

- 复合静电纺丝分离器

- 其他的

第六章 市场估价与预测:依製造流程划分,2022-2035年

- 湿式製程(相变)

- 热致相分离(TIPS)

- 非溶剂诱导相分离(NIPS)

- 干法(拉伸)

- 单轴拉伸

- 双轴拉伸

- 其他的

第七章 市场估计与预测:依厚度划分,2022-2035年

- 超薄隔膜(小于12µm)

- 标准厚度隔膜(12–20µm)

- 厚隔膜(超过 20µm)

第八章 市场估计与预测:依电池化学品划分,2022-2035年

- 锂离子电池隔膜

- 铅酸电池隔板

- 钠离子电池隔膜

- 全固态电池隔离膜

- 锂硫电池隔离膜

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 汽车应用

- 电池式电动车(BEV)

- 插电式混合动力汽车(PHEV)

- 混合动力电动车(HEV)

- 电动摩托车

- 电动商用车辆(巴士、卡车)

- 用于非公路用途的电动车

- 其他的

- 家用电子电器

- 智慧型手机

- 笔记型电脑和平板电脑

- 穿戴式装置(智慧型手錶、健身追踪器)

- 行动电池

- 电子烟和电子烟设备

- 其他的

- 能源储存系统(ESS)

- 电网级储能

- 住宅储能

- 商用和工业储能

- 公用事业规模储能

- 其他的

- 工业应用

- 物料搬运设备(堆高机)

- UPS(不断电系统)

- 通讯备用电源

- 医疗设备

- 其他的

- 电动工具和设备

- 无线电动工具

- 园艺设备

- 其他的

- 船舶/航太

- 船舶电力推进系统

- 航太应用

- 其他的

- 可再生能源的整合

- 太阳能发电+储能係统

- 风力发电+储能係统

- 其他的

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十一章:公司简介

- Asahi Kasei Corporation(Celgard)

- Toray Industries, Inc.

- SK Innovation Co., Ltd.(SK On)

- W-SCOPE Corporation

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- ENTEK International LLC

- SEMCORP Co., Ltd.

- Arkema SA

- Solvay SA

- Hollingsworth &Vose Company

- Dreamweaver International

- Blue Solutions(Bollore Group)

- Cangzhou Mingzhu Plastic Co., Ltd.

- Xinxiang Zhongke Science &Technology Co., Ltd.

- Shenzhen Senior Technology Material Co., Ltd.

The Global Battery Separators Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 19.1 billion by 2035.

Market growth is driven by the increasing demand for high-performance and safe energy storage solutions across electric vehicles, consumer electronics, and industrial applications. Battery separators act as thin membranes that allow ion flow between anode and cathode while preventing direct electrical contact, ensuring safe operation and preventing short circuits that could lead to overheating or battery failure. These separators are typically made from polymeric materials such as polyethylene, polypropylene, and composite blends, designed to maintain thermal stability, chemical resistance, and mechanical strength across lithium-ion, lead-acid, and nickel-metal hydride batteries. Advanced separators incorporating ceramic coatings or nanostructures enhance thermal stability and electrolyte wettability, while ultra-thin designs reduce internal resistance, enabling higher power output without compromising safety. The push for high-energy-density batteries, fast-charging capabilities, and flexible wearable applications is further accelerating technological advancements and adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $19.1 Billion |

| CAGR | 9.5% |

The polyolefin-based separators segment reached USD 4.1 billion in 2025, offering affordability and chemical stability. Meanwhile, ceramic-coated and polymer-coated separators are gaining traction due to enhanced thermal protection and improved safety features. Aramid-based and nonwoven separators are increasingly used in high-performance batteries requiring long-lasting durability. Electrospun separators are emerging as advanced materials to support higher energy density, rapid charging, and flexible battery applications.

The lithium-ion battery separators segment generated USD 1 billion in 2025, reflecting their widespread use in electric vehicles, energy storage systems, and consumer electronics. Lead-acid battery separators remain essential for automotive starter batteries and industrial backup applications due to their cost-effectiveness and reliable performance.

North America Battery Separators Market is expected to grow from USD 1 billion in 2025 to USD 2.7 billion by 2035, driven by electric vehicle adoption, gigafactory development, supply chain restructuring, and government-backed initiatives supporting battery manufacturing. Research and development in high-safety and solid-state separators is positioning the region as a hub for next-generation energy storage solutions.

Prominent players in the Global Battery Separators Market include Asahi Kasei Corporation (Celgard), Toray Industries, Inc., SK Innovation Co., Ltd. (SK On), W-SCOPE Corporation, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, UBE Corporation, ENTEK International LLC, SEMCORP Co., Ltd., Arkema S.A., Solvay, Hollingsworth & Vose Company, Dreamweaver International, Blue Solutions (Bollore Group), Cangzhou Mingzhu Plastic Co., Ltd., Xinxiang Zhongke Science & Technology Co., Ltd., Shenzhen Senior Technology Material Co., Ltd. Key strategies employed by companies in the Global Battery Separators Market include investing in R&D to develop ultra-thin and high-safety separators, launching ceramic-coated and polymer-coated products, focusing on advanced lithium-ion and solid-state battery technologies, expanding manufacturing capacities through strategic partnerships and joint ventures, enhancing supply chain localization to ensure steady raw material availability, entering emerging markets with cost-effective solutions, providing technical support and training for battery manufacturers, integrating IoT-enabled monitoring for smart energy management, and promoting environmentally friendly and recyclable separator materials to align with sustainability trends.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material Type

- 2.2.2 Manufacturing Process

- 2.2.3 Thickness

- 2.2.4 Battery Chemistry

- 2.2.5 Application

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer interest in collagen-rich functional nutrition

- 3.2.1.2 Increasing adoption of paleo and keto lifestyles

- 3.2.1.3 Demand for dairy-free protein alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and sourcing costs

- 3.2.2.2 Limited appeal among vegetarian and vegan consumers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into ready-to-drink and convenience formats

- 3.2.3.2 Innovation in flavor enhancement and masking technologies

- 3.2.3.3 Growth in emerging health and wellness markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.1.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyolefin-based separators

- 5.2.1 Polypropylene (PP) separators

- 5.2.2 Polyethylene (PE) separators

- 5.2.3 Multi-layer PP/PE/PP separators

- 5.3 Ceramic-coated separators

- 5.3.1 Alumina (Al2O3) coated separators

- 5.3.2 Silica (SiO2) coated separators

- 5.3.3 Zirconia (ZrO2) coated separators

- 5.3.4 Boehmite coated separators

- 5.4 Polymer-coated separators

- 5.4.1 PVDF coated separators

- 5.4.2 PMMA coated separators

- 5.4.3 PVA coated separators

- 5.5 Aramid-based separators

- 5.5.1 Aramid nanofiber (ANF) separators

- 5.5.2 Meta-aramid nonwoven separators

- 5.5.3 Para-aramid composite separators

- 5.6 Nonwoven separators

- 5.6.1 Cellulose-based nonwoven separators

- 5.6.2 PET nonwoven separators

- 5.6.3 Glass fiber nonwoven separators

- 5.7 Electrospun separators

- 5.7.1 Nanofiber electrospun membranes

- 5.7.2 Composite electrospun separators

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Wet process (phase inversion)

- 6.2.1 Thermally induced phase separation (TIPS)

- 6.2.2 Non-solvent induced phase separation (NIPS)

- 6.3 Dry process (stretching)

- 6.3.1 Uniaxial stretching

- 6.3.2 Biaxial stretching

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Thickness, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ultra-thin separators (<12 µm)

- 7.3 Standard thickness separators (12-20 µm)

- 7.4 Thick separators (>20 µm)

Chapter 8 Market Estimates and Forecast, By Battery Chemistry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Lithium-ion battery separators

- 8.3 Lead-acid battery separators

- 8.4 Sodium-ion battery separators

- 8.5 Solid-state battery separators

- 8.6 Lithium-sulfur battery separators

Chapter 9 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Automotive applications

- 9.2.1 Battery electric vehicles (BEV)

- 9.2.2 Plug-in hybrid electric vehicles (PHEV)

- 9.2.3 Hybrid electric vehicles (HEV)

- 9.2.4 Electric two-wheelers

- 9.2.5 Electric commercial vehicles (buses, trucks)

- 9.2.6 Electric off-highway vehicles

- 9.2.7 Others

- 9.3 Consumer electronics

- 9.3.1 Smartphones

- 9.3.2 Laptops and tablets

- 9.3.3 Wearables (smartwatches, fitness trackers)

- 9.3.4 Power banks

- 9.3.5 E-cigarettes and vaping devices

- 9.3.6 Others

- 9.4 Energy storage systems (ESS)

- 9.4.1 Grid-scale energy storage

- 9.4.2 Residential energy storage

- 9.4.3 Commercial and industrial (C&I) storage

- 9.4.4 Utility-scale storage

- 9.4.5 Others

- 9.5 Industrial applications

- 9.5.1 Material handling equipment (forklifts)

- 9.5.2 UPS (uninterruptible power supply)

- 9.5.3 Telecom backup power

- 9.5.4 Medical devices

- 9.5.5 Others

- 9.6 Power tools and equipment

- 9.6.1 Cordless power tools

- 9.6.2 Garden equipment

- 9.6.3 Others

- 9.7 Marine and aerospace

- 9.7.1 Electric marine propulsion

- 9.7.2 Aerospace applications

- 9.7.3 Others

- 9.8 Renewable energy integration

- 9.8.1 Solar + storage systems

- 9.8.2 Wind + storage systems

- 9.8.3 Others

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Asahi Kasei Corporation (Celgard)

- 11.2 Toray Industries, Inc.

- 11.3 SK Innovation Co., Ltd. (SK On)

- 11.4 W-SCOPE Corporation

- 11.5 Sumitomo Chemical Co., Ltd.

- 11.6 Mitsubishi Chemical Group Corporation

- 11.7 UBE Corporation

- 11.8 ENTEK International LLC

- 11.9 SEMCORP Co., Ltd.

- 11.10 Arkema S.A.

- 11.11 Solvay S.A.

- 11.12 Hollingsworth & Vose Company

- 11.13 Dreamweaver International

- 11.14 Blue Solutions (Bollore Group)

- 11.15 Cangzhou Mingzhu Plastic Co., Ltd.

- 11.16 Xinxiang Zhongke Science & Technology Co., Ltd.

- 11.17 Shenzhen Senior Technology Material Co., Ltd.

2026年全球工业分离器市场报告2026年全球电池隔离膜市场报告

2026年全球工业分离器市场报告2026年全球电池隔离膜市场报告 电池隔膜市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、最终用途产业、地区和竞争格局划分,2021-2031年)

电池隔膜市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、最终用途产业、地区和竞争格局划分,2021-2031年) 软包电池用铝塑薄膜市场:按产品类型、阻隔材料、厚度范围、製造流程和应用分類的全球预测(2026-2032年)锂电池以湿式加工PO隔膜市场:依电池形状、厚度、应用及通路-2026年至2032年全球预测锂陶瓷电池模组市场(按产品类型、应用和销售管道),全球预测(2026-2032年)

软包电池用铝塑薄膜市场:按产品类型、阻隔材料、厚度范围、製造流程和应用分類的全球预测(2026-2032年)锂电池以湿式加工PO隔膜市场:依电池形状、厚度、应用及通路-2026年至2032年全球预测锂陶瓷电池模组市场(按产品类型、应用和销售管道),全球预测(2026-2032年) 电池隔膜市场规模、份额及成长分析(按电池类型、材料类型、最终用户和地区划分)-2026-2033年产业预测

电池隔膜市场规模、份额及成长分析(按电池类型、材料类型、最终用户和地区划分)-2026-2033年产业预测 电池密封件:全球市场份额和排名、总收入和需求预测(2025-2031年)PVC电池隔膜市场-全球产业规模、份额、趋势、机会及预测(按类型、技术、应用、地区及竞争情况细分,2020-2030年)

电池密封件:全球市场份额和排名、总收入和需求预测(2025-2031年)PVC电池隔膜市场-全球产业规模、份额、趋势、机会及预测(按类型、技术、应用、地区及竞争情况细分,2020-2030年) 不织布电池隔膜的全球市场的未来(~2030年)

不织布电池隔膜的全球市场的未来(~2030年)