|

市场调查报告书

商品编码

1998689

十二指肠内视镜市场机会、成长要素、产业趋势分析及2026-2035年预测Duodenoscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

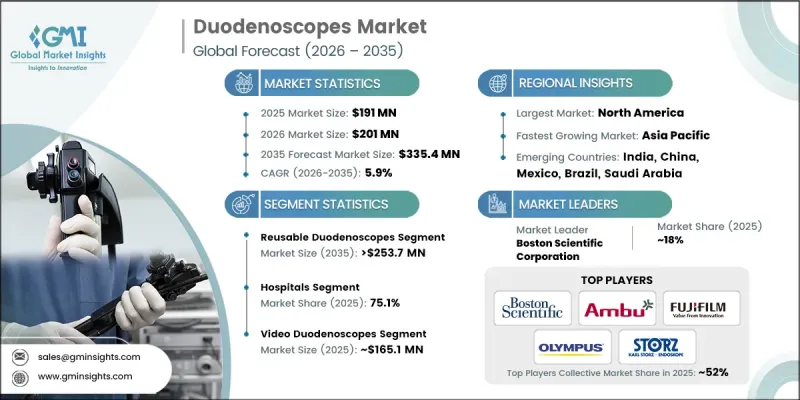

全球十二指肠内视镜市场预计到 2025 年价值 1.91 亿美元,预计到 2035 年将以 5.9% 的复合年增长率增长至 3.354 亿美元。

十二指肠内视镜产业的成长主要受以下因素驱动:对微创医疗程序的需求不断增长、消化器官系统疾病盛行率上升以及内视镜技术在治疗领域的应用日益广泛。十二指肠内视镜是一种专门设计的柔软性医疗器械,用于评估和治疗影响小肠上段的疾病。医生广泛使用这些器械来诊断和治疗与胃肠道及其相关器官有关的疾病。人们对胃肠道健康的日益重视以及早期筛检工作的持续发展,促使患者接受诊断性检查。此外,许多已开发地区医疗保险覆盖范围的扩大,也使得患者更容易获得先进的诊断技术。同时,全球人口老化增加了消化器官系统和肝胰腺疾病的风险,这也持续推高了对专用诊断设备的需求。此外,十二指肠内视镜在治疗性介入的应用日益广泛,也使其临床意义更加深远。成像能力、安全机制和仪器人体工学的持续技术进步也在改善检查结果,并加速医疗机构的采用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 1.91亿美元 |

| 预测金额 | 3.354亿美元 |

| 复合年增长率 | 5.9% |

预计到2035年,可重复使用十二指肠镜市场将以5.6%的复合年增长率成长,达到2.537亿美元。由于初始投资可透过长期重复使用来抵消,可重复使用设备在医疗服务量大的机构中仍广泛应用。预算有限的医疗机构也常因其成本效益而选择可重复使用型号。现代可重复使用十二指肠镜设计采用可拆卸组件,简化了清洁流程,并有助于降低污染风险。此外,配备高清视觉化技术和先进影像处理功能的可重复使用设备在复杂的诊断和治疗过程中继续发挥至关重要的作用。

预计到2025年,视讯十二指肠镜市场规模将达到1.651亿美元。视讯十二指肠镜能够增强消化道的可视性,使临床医生能够进行更精准的检查和操作。先进的影像技术使医护人员能够即时评估解剖结构,从而提高手术过程中临床决策的准确性。高品质的可视化功能也促进了微创内视镜手术的广泛应用。此外,影像技术和智慧诊断工具的创新正在不断提高视讯十二指肠镜系统的准确性和可靠性。同时,新型设备设计更加轻巧、符合人体工学,从而延长了手术时间,并提高了医护人员的操作便利性。

预计2025年,美国十二指肠内视镜市场规模将达7,450万美元。美国市场强劲的需求主要源自于消化器官系统疾病的高发生率,这些疾病需要专业的诊断和治疗。美国医疗机构正越来越多地采用先进的内视镜技术来提高诊断准确性和治疗效果。成像技术的持续创新以及先进可视化功能的集成,进一步推动了医院和专科医疗中心对尖端十二指肠内视镜系统的需求。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策和资料完整性倡议

- 资讯来源一致性通讯协定

- GMI人工智慧政策和资料完整性倡议

- 调查过程和可靠性评分

- 调查过程的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 每种方法中基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 胃肠道疾病盛行率增加

- 医疗设备的技术进步

- 提高认知度和诊断率

- 产业潜在风险与挑战

- 高成本和严格的监管要求

- 市场机会

- 人工智慧和数据分析的融合激增

- 促进因素

- 成长潜力分析

- 监理情势

- 管道分析

- 2025年价格分析(基于初步调查)

- 救赎方案

- 消费者洞察(基于初步研究)

- 科技趋势

- 目前技术

- 新兴技术

- 差距分析

- 人工智慧和生成式人工智慧对市场的影响

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- LAMEA

- 竞争定位矩阵

- 主要市场公司的竞争分析

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品类型发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 可重复使用的十二指肠镜

- 免洗十二指肠镜

第六章 市场估计与预测:依类别划分,2022-2035年

- 影片十二指肠镜

- 光纤十二指肠内视镜

第七章 市场估价与预测:依销售管道划分,2022-2035年

- 直销

- 销售代理

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 其他最终用户

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Ambu

- Boston Scientific Corporation

- Fujifilm Holdings Corporation

- Olympus Corporation

- Ottomed Endoscopy

- PENTAX MEDICAL

- SonoScape

- STORZ

The Global Duodenoscopes Market was valued at USD 191 million in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 335.4 million by 2035.

Growth across the duodenoscope industry is supported by the rising demand for minimally invasive medical procedures, the growing prevalence of digestive system disorders, and expanding therapeutic applications of endoscopic technologies. Duodenoscopes are specialized flexible medical instruments designed to evaluate and treat conditions affecting the upper section of the small intestine. These devices are widely used in procedures that allow physicians to diagnose and manage disorders related to the digestive tract and associated organs. Increasing awareness regarding digestive health and the expansion of early screening initiatives are encouraging patients to undergo diagnostic examinations. In addition, improved access to healthcare coverage in many developed regions allows patients to utilize advanced diagnostic technologies more easily. The global aging population is also more susceptible to digestive and hepatopancreatic conditions, which continues to increase the need for specialized diagnostic equipment. Furthermore, the growing use of duodenoscopes for therapeutic interventions has expanded their clinical significance. Continuous technological improvements in imaging capabilities, safety mechanisms, and device ergonomics are also enhancing procedure outcomes and increasing adoption across healthcare facilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $191 Million |

| Forecast Value | $335.4 Million |

| CAGR | 5.9% |

The reusable duodenoscopes segment is expected to grow at a CAGR of 5.6% and is projected to reach USD 253.7 million by 2035. Reusable devices remain widely utilized in healthcare facilities with high procedural volumes because the initial investment can be offset through repeated usage over time. Medical institutions operating with constrained budgets often rely on reusable models due to their cost efficiency. Modern reusable duodenoscope designs incorporate detachable components that simplify cleaning processes and help reduce contamination risks. In addition, reusable devices equipped with high-definition visualization technologies and advanced imaging capabilities continue to play a crucial role in complex diagnostic and therapeutic procedures.

The video duodenoscopes segment generated USD 165.1 million in 2025. Video-based duodenoscopes provide enhanced visualization of the digestive tract, enabling clinicians to perform more accurate examinations and interventions. Advanced imaging technologies allow healthcare professionals to assess anatomical structures in real time, supporting improved clinical decision-making during procedures. High-quality visualization capabilities also contribute to the increased adoption of minimally invasive endoscopic procedures. Furthermore, innovations in imaging technologies and intelligent diagnostic tools are improving the precision and reliability of video duodenoscope systems. Newer device designs are also lighter and more ergonomic, which supports longer procedures and improves usability for medical professionals.

U.S. Duodenoscopes Market generated USD 74.5 million in 2025. The strong demand in the United States is supported by the high occurrence of digestive system disorders that require specialized diagnostic and therapeutic procedures. Healthcare providers in the country are increasingly adopting advanced endoscopic technologies to improve diagnostic accuracy and treatment outcomes. Continuous innovation in imaging technologies and the integration of advanced visualization capabilities are further supporting the demand for modern duodenoscope systems across hospitals and specialized medical centers.

Key companies operating in the Global Duodenoscopes Market include Olympus Corporation, Boston Scientific Corporation, Fujifilm Holdings Corporation, PENTAX MEDICAL, Ambu, Ottomed Endoscopy, SonoScape, and STORZ. Companies in the Global Duodenoscopes Market are implementing several strategic initiatives to strengthen their competitive position and expand market reach. Leading manufacturers are investing significantly in research and development to introduce advanced endoscopic technologies that improve imaging quality, safety features, and overall device performance. Many organizations are focusing on developing innovative designs that enhance infection control and simplify device reprocessing. Strategic partnerships with healthcare institutions and medical technology providers are also helping companies accelerate product adoption and expand clinical applications. In addition, manufacturers are increasing their global distribution networks and strengthening service support for healthcare facilities. Continuous product innovation, regulatory approvals in multiple regions, and the introduction of next-generation endoscopic imaging technologies are enabling companies to reinforce their presence in the duodenoscopes market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key Market Trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Category trends

- 2.2.4 Sales channel trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of gastrointestinal diseases

- 3.2.1.2 Technological advancements in devices

- 3.2.1.3 Rising awareness and diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Surge in integrated AI and data analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Pricing analysis, 2025 (Driven by primary research)

- 3.7 Reimbursement scenario

- 3.8 Consumer insights (Driven by primary research)

- 3.9 Technology landscape

- 3.9.1 Current technologies

- 3.9.2 Emerging technologies

- 3.10 Gap analysis

- 3.11 Impact of AI and generative AI on the market

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Reusable duodenoscopes

- 5.3 Single-use duodenoscopes

Chapter 6 Market Estimates and Forecast, By Category, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Video duodenoscopes

- 6.3 Fiber optic duodenoscopes

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Distributors

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 Boston Scientific Corporation

- 10.3 Fujifilm Holdings Corporation

- 10.4 Olympus Corporation

- 10.5 Ottomed Endoscopy

- 10.6 PENTAX MEDICAL

- 10.7 SonoScape

- 10.8 STORZ

全球十二指肠内视镜市场规模、份额、趋势和成长分析报告(2026-2034年)

全球十二指肠内视镜市场规模、份额、趋势和成长分析报告(2026-2034年) 十二指肠镜市场 - 全球产业规模、份额、趋势、机会及预测(按产品、应用、最终用户、地区和竞争格局划分),2021-2031年

十二指肠镜市场 - 全球产业规模、份额、趋势、机会及预测(按产品、应用、最终用户、地区和竞争格局划分),2021-2031年 十二指肠镜市场按产品类型、应用、最终用户和地区划分

十二指肠镜市场按产品类型、应用、最终用户和地区划分 全球十二指肠镜市场规模、份额、趋势分析报告:2025 年至 2032 年按应用、产品、最终用途和地区分類的展望和预测

全球十二指肠镜市场规模、份额、趋势分析报告:2025 年至 2032 年按应用、产品、最终用途和地区分類的展望和预测 十二指肠镜市场规模、份额、趋势分析报告:按产品、应用、最终用途、地区和细分市场预测,2025 年至 2030 年

十二指肠镜市场规模、份额、趋势分析报告:按产品、应用、最终用途、地区和细分市场预测,2025 年至 2030 年 日本的十二指肠内视镜市场:2033年前预测 - 软性影音十二指肠内视镜

日本的十二指肠内视镜市场:2033年前预测 - 软性影音十二指肠内视镜