|

市场调查报告书

商品编码

1998693

胶印层压包装市场机会、成长要素、产业趋势分析及 2026-2035 年预测。Litho Laminated Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

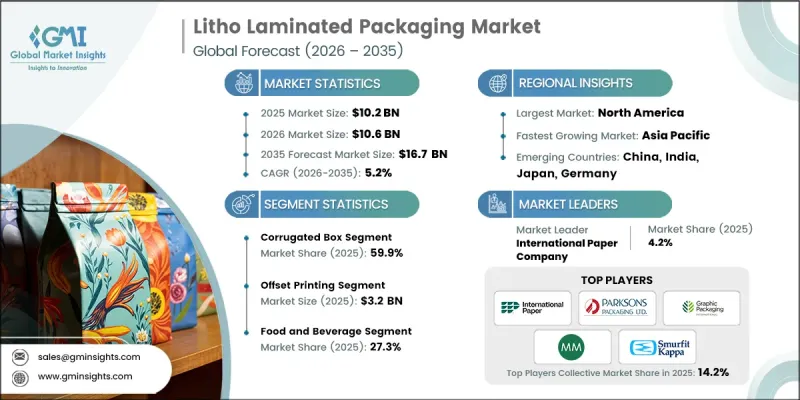

全球胶印复合包装市场预计到 2025 年将价值 102 亿美元,预计到 2035 年将以 5.2% 的复合年增长率增长至 167 亿美元。

胶印复合包装市场的成长主要受零售业趋势变化、高端产品展示需求成长以及视觉吸引力包装在多个消费品领域日益重要等因素的驱动。包装已成为重要的品牌元素,使企业能够区分产品并有效地向消费者传达品牌形象。随着全球有组织的零售和现代分销管道的扩张,企业越来越依赖兼具耐用性和强烈视觉衝击力的包装形式。数位零售通路和直销模式的兴起也影响包装需求,企业寻求既能保护产品在运输过程中不受损坏,又能保持引人注目的品牌形象的解决方案。同时,永续性考量正在推动包装创新,促使企业采用可回收纤维基结构,以兼顾结构强度和环境责任。胶印复合包装的优势在于将高品质的图像与耐用的瓦楞纸板材料相结合,使其成为希望提升产品保护和商店可见度的企业的理想选择。这些因素共同推动了全球胶印复合包装市场的持续成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 102亿美元 |

| 预测金额 | 167亿美元 |

| 复合年增长率 | 5.2% |

随着零售商和产品製造商越来越重视能够提升产品展示效果和品牌传播的包装,胶印覆膜包装市场持续成长。现代零售环境需要既能吸引消费者眼球,又能在整个分销和搬运过程中保持结构可靠性的包装解决方案。胶印覆膜技术能够在瓦楞纸板上实现高解析度印刷,从而呈现鲜艳的色彩、精緻的细节和优质的视觉效果。这种兼具视觉品质和实体耐久性的包装能够提升产品在零售环境中的可见度,并有助于提高品牌知名度。同时,线上零售和直邮管道的快速发展也催生了对兼顾运输保护和视觉吸引力的包装形式的需求。尤其是在产品展示至关重要的数位商务环境中,包装已成为客户体验不可或缺的一部分。

预计2025年,瓦楞纸箱市占率将达到59.9%。瓦楞纸箱凭藉其卓越的结构性能、承重能力和高效的运输性能,仍然是首选的包装解决方案。其独特的设计使其能够承载更重的货物,并满足大规模分销网络的搬运需求。此外,精细印刷的衬纸板与瓦楞纸板的结合,使製造商能够兼顾结构耐久性和视觉吸引力。这项特性使得企业可以将瓦楞纸箱用于产品运输和零售展示。这些包装形式在应对大规模分销的同时,也能维持强大的品牌推广能力,这将巩固其在胶印复合包装市场中的重要地位。

预计到2025年,胶印市场规模将达32亿美元。胶印技术凭藉其即使在大规模生产中也能提供高清印刷品质和稳定色彩还原的能力,持续保持强劲的市场地位。这种印刷方式能够呈现复杂的设计元素和高端的表面处理效果,进而提升包装产品的视觉吸引力。由于其与大规模胶印覆膜製程的兼容性,胶印在高品质二次包装和零售展示解决方案的生产中仍被广泛应用。製造商也青睐这种印刷技术在大规模生产中的成本效益,使其成为追求视觉效果出色且品质始终如一的包装产品的可靠选择。

到2025年,北美胶印复合包装市占率将达到35.7%。该地区市场扩张的原因在于,有组织的零售环境和整合的分销网络对高品质零售包装的需求不断增长。在北美营运的公司非常重视耐用包装形式,这些包装形式兼具出色的图形表现力,能够在竞争激烈的零售环境中提升产品辨识度。该地区拥有完善的瓦楞纸包装基础设施,能够支援复合包装材料的大规模生产和分销。美国和加拿大的包装加工商正加大对先进製造技术的投资,旨在提高生产效率并减少材料废弃物。这些技术进步不仅帮助製造商增强了营运能力,也支持了全部区域永续包装实践的发展。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 零售包装对优质展示效果的需求

- 电子商务市场正在成长,需要耐用的、带有品牌识别的瓦楞纸箱。

- 全球速食连锁店的扩张

- 过渡到可回收纸板包装

- 推出适用于超级市场。

- 产业潜在风险与挑战

- 工艺衬里和波纹管的价格波动

- 与数位印刷瓦楞纸板的竞争

- 市场机会

- 永续纺织包装的成长

- 客製化胶印贴合加工电商运输箱

- 促进因素

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与发展(R&D)

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 业务拓展与投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 瓦楞纸箱

- 纸盒

第六章 市场估算与预测:依笛型划分,2022-2035年

- 低音长笛

- C调长笛

- E 长笛

- F调长笛

- 公元前长笛

- BE 长笛

- 其他的

第七章 市场估价与预测:依印刷技术划分,2022-2035年

- 胶印

- 柔版印刷

- 凹版印刷

- 数位印刷

第八章 市场估算与预测:依最终用途产业划分,2022-2035年

- 食品/饮料

- 製药和医疗保健

- 消费品

- 工业包装

- 电子与电机工程

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 主要企业

- International Paper Company

- Smurfit Kappa Group

- Graphic Packaging International, LLC

- Mayr-Melnhof Karton AG

- 按地区分類的主要企业

- 北美洲

- Accurate Box Company, Inc.

- Brandon Packaging, LLC

- Frankston Packaging

- Infinity Packaging Solutions

- Grief, Inc.

- The Cardboard Box Company

- 亚太地区

- Parksons Packaging Ltd.

- Shanghai DE Printed Box

- SK Offset

- PM Packaging

- 欧洲

- Jaymar Packaging Ltd

- LGR Packaging

- ALLIANCE PACKAGING

- 北美洲

- 特殊玩家/干扰者

- Platypus Print Packaging

The Global Litho Laminated Packaging Market was valued at USD 10.2 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 16.7 billion by 2035.

Growth of the litho laminated packaging market is strongly supported by evolving retail dynamics, increasing demand for premium product presentation, and the rising importance of visually appealing packaging across multiple consumer industries. Packaging has become a crucial branding element that enables companies to differentiate their products and effectively communicate their brand identity to consumers. As organized retail and modern distribution channels expand globally, businesses increasingly rely on packaging formats that combine durability with strong visual impact. The growth of digital retail channels and direct shipping models is also influencing packaging requirements, as companies seek solutions that protect products during transit while maintaining attractive branding. At the same time, sustainability considerations are shaping packaging innovation, encouraging the adoption of recyclable fiber-based structures that balance structural integrity with environmental responsibility. Litho laminated packaging offers the advantage of combining high-quality graphics with durable corrugated materials, making it an effective solution for companies aiming to enhance both product protection and shelf visibility. These factors collectively support the continued expansion of the global litho laminated packaging market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.2 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 5.2% |

The litho laminated packaging market continues to gain momentum as retailers and product manufacturers place greater emphasis on packaging that enhances product presentation and brand communication. Modern retail environments require packaging solutions capable of attracting consumer attention while maintaining structural reliability throughout distribution and handling processes. Lithographic lamination technology allows high-resolution printed graphics to be applied to corrugated boards, enabling vibrant colors, refined detailing, and premium visual finishes. This combination of visual quality and physical durability strengthens product visibility in retail environments and supports stronger brand recognition. At the same time, the rapid growth of online retail and direct shipping channels has created demand for packaging formats that offer both protective strength and visual appeal during delivery. Packaging has become an important part of the customer experience, especially in digital commerce environments where product presentation remains critical.

The corrugated box segment accounted for 59.9% share in 2025. Corrugated boxes remain a preferred packaging solution due to their strong structural properties, stacking strength, and efficient transportation capabilities. Their design allows them to support heavier loads and withstand the handling demands associated with large-scale distribution networks. In addition, the integration of finely printed linerboards with corrugated materials enables manufacturers to combine structural durability with visually appealing graphics. This feature allows companies to use corrugated boxes for both product transportation and retail display purposes. The ability of these packaging formats to support large-volume distribution while maintaining strong branding capabilities ensures their continued importance in the litho laminated packaging market.

The offset printing segment generated USD 3.2 billion in 2025. Offset printing technology continues to maintain a strong position due to its ability to deliver high-definition print quality and consistent color reproduction across large production volumes. The printing method supports intricate design elements and premium finishing effects that enhance the visual appeal of packaging products. Because of its compatibility with large-scale lithographic lamination processes, offset printing remains widely adopted for producing high-quality secondary packaging and retail display solutions. Manufacturers also favor this printing technology for its cost efficiency when operating at high production volumes, making it a reliable option for companies seeking visually striking packaging with consistent quality standards.

North America Litho Laminated Packaging Market accounted for 35.7% share in 2025. The market in this region is expanding due to increasing demand for high-quality retail packaging across organized retail environments and integrated distribution networks. Businesses operating in North America are placing strong emphasis on packaging formats that combine durability with advanced graphic presentation to improve product visibility in competitive retail settings. The region benefits from a well-established corrugated packaging infrastructure that supports large-scale manufacturing and distribution of laminated packaging materials. Packaging converters across the United States and Canada are increasingly investing in advanced manufacturing technologies designed to improve production efficiency and reduce material waste. These technological improvements are helping manufacturers enhance operational capacity while supporting sustainable packaging practices across the region.

Key companies operating in the Global Litho Laminated Packaging Market include Smurfit Kappa Group, International Paper Company, Graphic Packaging International, LLC, Mayr-Melnhof Karton AG, Greif, Inc., Accurate Box Company, Inc., Parksons Packaging Ltd., Brandon Packaging, LLC, Frankston Packaging, LGR Packaging, Infinity Packaging Solutions, Jaymar Packaging Ltd., Platypus Print Packaging, PM Packaging, SK Offset, Shanghai DE Printed Box, Alliance Packaging, and The Cardboard Box Company. Companies participating in the Global Litho Laminated Packaging Market are implementing several strategies to strengthen their competitive position and expand their global footprint. Many manufacturers are investing in advanced lamination technologies and automated production lines to improve operational efficiency and maintain consistent product quality. Expanding sustainable packaging solutions has also become a major strategic priority, with companies developing recyclable fiber-based materials and lightweight structures that reduce environmental impact. Strategic partnerships with consumer goods companies and retail brands allow packaging providers to develop customized packaging formats tailored to specific branding and distribution needs. Businesses are also focusing on enhancing printing capabilities and graphic finishing technologies to meet the growing demand for visually impactful packaging.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Flute type trends

- 2.2.3 Printing technology trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Premium shelf-appeal demand in retail packaging

- 3.2.1.2 E-commerce growth requiring durable branded cartons

- 3.2.1.3 Expansion of quick-service restaurant chains globally

- 3.2.1.4 Shift toward recyclable corrugated-based packaging

- 3.2.1.5 Retail-ready packaging adoption by supermarkets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile kraft liner and fluting prices

- 3.2.2.2 Competition from digitally printed corrugated

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in sustainable fiber-based packaging

- 3.2.3.2 Custom litho-laminated e-commerce shipper boxes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Corrugated box

- 5.3 Cartons

Chapter 6 Market Estimates and Forecast, By Flute Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 B Flute

- 6.3 C Flute

- 6.4 E Flute

- 6.5 F Flute

- 6.6 BC Flute

- 6.7 BE Flute

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Offset printing

- 7.3 Flexographic printing

- 7.4 Gravure printing

- 7.5 Digital printing

Chapter 8 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.3 Pharmaceutical and healthcare

- 8.4 Consumer goods

- 8.5 Industrial packaging

- 8.6 Electronics and electrical

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 International Paper Company

- 10.1.2 Smurfit Kappa Group

- 10.1.3 Graphic Packaging International, LLC

- 10.1.4 Mayr-Melnhof Karton AG

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Accurate Box Company, Inc.

- 10.2.1.2 Brandon Packaging, LLC

- 10.2.1.3 Frankston Packaging

- 10.2.1.4 Infinity Packaging Solutions

- 10.2.1.5 Grief, Inc.

- 10.2.1.6 The Cardboard Box Company

- 10.2.2 Asia Pacific

- 10.2.2.1 Parksons Packaging Ltd.

- 10.2.2.2 Shanghai DE Printed Box

- 10.2.2.3 SK Offset

- 10.2.2.4 PM Packaging

- 10.2.3 Europe

- 10.2.3.1 Jaymar Packaging Ltd

- 10.2.3.2 LGR Packaging

- 10.2.3.3 ALLIANCE PACKAGING

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Platypus Print Packaging

包装复合材料市场规模、份额、成长和行业分析:按材料(聚乙烯、聚丙烯、聚酯、铝箔、纸张、其他)、应用和地区划分(至2034年)

包装复合材料市场规模、份额、成长和行业分析:按材料(聚乙烯、聚丙烯、聚酯、铝箔、纸张、其他)、应用和地区划分(至2034年) 积层软管市场机会、成长要素、产业趋势分析及2026年至2035年预测

积层软管市场机会、成长要素、产业趋势分析及2026年至2035年预测 铝阻隔积层软管市场(按应用、层数、管径、装饰和封闭类型)—2025-2032 年全球预测

铝阻隔积层软管市场(按应用、层数、管径、装饰和封闭类型)—2025-2032 年全球预测 全球积层软管市场

全球积层软管市场 全球包装层压板市场:市场规模、份额和趋势分析(按材料、厚度、最终用途和地区),按细分市场预测(2025-2030 年)

全球包装层压板市场:市场规模、份额和趋势分析(按材料、厚度、最终用途和地区),按细分市场预测(2025-2030 年) 2032 年积层软管市场预测:按类型、瓶盖类型、材料、印刷技术、产能、最终用户、地区进行的全球分析

2032 年积层软管市场预测:按类型、瓶盖类型、材料、印刷技术、产能、最终用户、地区进行的全球分析 全球铝阻隔层压管市场规模研究,按应用、产能、材料和区域预测 2022-2032 年

全球铝阻隔层压管市场规模研究,按应用、产能、材料和区域预测 2022-2032 年