|

市场调查报告书

商品编码

1998698

汽车控制电缆市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Automotive Control Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

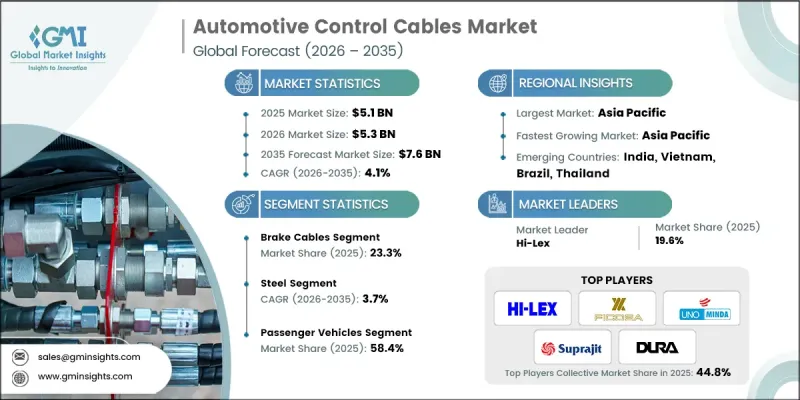

全球汽车控制电缆市场预计到 2025 年将价值 51 亿美元,预计到 2035 年将以 4.1% 的复合年增长率增长至 76 亿美元。

儘管汽车电气化进程不断推进,但对汽车控制电缆的需求仍保持稳定。这是因为各种机械系统仍然需要基于电缆的机构来实现运作功能。即使是配备电动驱动系统的车辆,许多内部机械运动仍然依赖控制电缆系统来确保运动的稳定性和功能性。除了新车生产之外,全球车辆老化也是维持替换零件需求的重要因素。 2023年,全球道路上行驶的车辆平均车龄超过12年,导致控制电缆等机械零件的损耗率增加。随着车辆运作的延长,维护和更换工作在已开发和开发中国家中汽车市场的重要性日益凸显。因此,在成熟市场,替换零件约占汽车控制电缆总销售额的40%,这进一步提升了售后市场与OEM(原厂设备製造商)需求在全球汽车控制电缆市场中的重要性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 51亿美元 |

| 预测金额 | 76亿美元 |

| 复合年增长率 | 4.1% |

儘管汽车产业正逐步采用先进的电子变速箱技术和数位控制系统,但手排变速箱车辆在全球汽车产量中仍占据相当大的份额。预计到2024年,配备手排变速箱的车辆将占全球总产量的近30%。这种持续的市场份额支撑着乘用车和轻型商用车对离合器和变速控制线的稳定需求。虽然车辆电子和自动化系统的进步正在影响零件设计,但预计这些发展不会显着减少汽车产业对控制线材的整体需求量。

预计到2025年,煞车拉索市场占有率将达到23.3%,并在2026年至2035年间以5%的复合年增长率成长。煞车拉索系统仍然是车辆安全机制的重要组成部分,其在全球乘用车和商用车领域的重要性持续凸显。以车辆安全标准为重点的法规结构,促使市场对可靠煞车系统(需要耐用的控制拉索)的需求保持稳定。除了作为原厂配套零件的需求外,煞车拉索还会因日常车辆运作而频繁磨损,从而增加了车辆整个生命週期内更换零件的需求。因此,煞车拉索系统在汽车控制拉索市场的原厂配套和售后市场中,对控制拉索的总销量贡献巨大。

按材料类型,预计到2025年,钢缆将占据44.6%的市场份额,并在2026年至2035年间以3.7%的复合年增长率增长。钢缆在汽车应用中仍然备受青睐,因为汽车应用需要高抗拉强度和承载能力来维持可靠的机械运作。这些特性在车辆系统中尤其重要,因为车辆系统需要在较长的运作週期内保持耐久性和稳定的性能。钢缆还具有很高的抗机械应力和环境适应性,使其适用于各种汽车平臺的长期使用。由于其可靠的性能和优异的性能,汽车製造商在多个汽车细分市场的大规模车辆生产中继续依赖钢製控制缆。

中国汽车控制线束市场占53%的全球份额,预计2025年市场规模将达到14亿美元。中国是汽车製造的重要中心,拥有庞大的生产能力和大规模的汽车保有量。乘用车、商用车和摩托车领域的高产量支撑了对原厂配套(OEM)控制线束系统的持续需求。车辆数量的持续成长也带动了售后市场替换件的庞大需求。在人口密集的都市区行驶的车辆频繁启停,加速了机械线束系统的磨损。因此,替换需求仍然强劲,巩固了中国作为亚太地区最重要的汽车控制线束生产和消费市场之一的地位。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 成长驱动因素

- 全球汽车拥有量增加

- 对机械系统的持续需求

- 车辆平均年龄增加

- 新兴汽车市场的成长

- 产业潜在风险与挑战

- 向电子作业系统过渡

- 售后市场的价格敏感性

- 市场机会

- 电动车产量增加

- 有组织的售后市场的扩张

- 零件製造本地化

- 成长驱动因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国有关汽车安全和机械控制部件的法规

- 与煞车和控制系统相关的联邦机动车辆安全标准

- 车辆耐久性和性能合规性要求

- 加拿大汽车零件安全和品质法规

- 欧洲

- 欧盟汽车安全和零件相容性框架

- 关于煞车和机械控制系统的ECE法规

- 各国汽车零件认证要求

- 汽车电缆的环境和材料合规性法规

- 亚太地区

- 中国汽车零件标准和品质法规

- 印度汽车安全和零件认证标准

- 日本汽车安全与机械控制系统指南

- 韩国汽车零件的品质和耐久性标准

- 东协区域汽车零件法规结构

- 拉丁美洲

- 巴西汽车安全和零件合规法规

- 阿根廷汽车零件品质要求

- 墨西哥汽车製造和安全标准

- 区域汽车零件法律规范

- 中东和非洲

- 阿联酋汽车安全和车辆零件法规

- 沙乌地阿拉伯的车辆安全和机械系统合规性

- 南非汽车零件标准和道路安全要求

- 法律规范

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产基地

- 消费者群体

- 出口和进口

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 碳足迹考量

- 线传技术的其他风险

- 电子节气门控制的采用率

- 电子驻车煞车普及率

- 线传换檔变速箱系统

- 机械和电子系统的成本效益分析

- 製造群分析:按地区

- 主要製造地:依地区划分

- 靠近接近性设备製造商 (OEM) 工厂的要求

- 生产能力分布:按地区

- 集中式和分散式製造地模式的比较

- 专利货币化与智慧财产权价值创造

- 授权收入机会

- 专利组合评估

- 交叉授权协议

- 防御性专利策略

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依电缆类型划分,2022-2035年

- 离合器拉索

- 加速器电缆

- 煞车线

- 换檔线缆

- 手煞车拉索

- 油门线

- 其他的

第六章 市场估计与预测:依材料划分,2022-2035年

- 钢

- PVC(聚氯乙烯)

- 尼龙

- 橡胶涂层

- 其他的

第七章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

- 摩托车

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 引擎控制

- 变速箱控制

- 煞车系统

- 暖通空调系统

- 其他的

第九章 市场估价与预测:依销售管道划分,2022-2035年

- OEM

- 售后市场

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 挪威

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

第十一章:公司简介

- 世界公司

- Atsumitec

- Cofle

- Dura Automotive Systems

- Ficosa International

- Hi-Lex

- Kuster

- Kyung Chang Industrial

- Nippon Cable System

- Sila

- Suprajit Engineering

- 当地公司

- Cable Manufacturing &Assembly

- Cablecraft Motion Controls

- Chuo Spring

- GEMO

- Grand Rapids Controls

- Minda

- Tata AutoComp Systems

- Thai Steel Cable

- WR Controls

- 新兴企业/颠覆者

- Acey Engineering

- Kalpa Industries

- KALTROL

- Premier Auto Cables

- Remsons Industries

- Silco Automotive Solutions

The Global Automotive Control Cables Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 7.6 billion by 2035.

Despite the increasing shift toward vehicle electrification, the demand for automotive control cables remains stable because various mechanical systems still require cable-based mechanisms for operational functionality. Even in vehicles powered by electric drivetrains, several internal mechanical operations continue to rely on control cable systems to enable consistent movement and functionality. In addition to new vehicle production, the global aging vehicle fleet is playing a significant role in sustaining demand for replacement components. The average age of vehicles in circulation worldwide surpassed twelve years in 2023, which has contributed to higher wear rates for mechanical components such as control cables. As vehicles remain in service for longer periods, maintenance and replacement activities have become increasingly important across both developed and developing automotive markets. Consequently, replacement parts account for roughly forty percent of total automotive control cable sales in mature markets, reinforcing the importance of the aftermarket segment alongside original equipment manufacturing demand within the global automotive control cables market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 4.1% |

Although the automotive industry is gradually adopting advanced electronic transmission technologies and digital control systems, manual transmission vehicles continue to maintain a meaningful share of global vehicle production. In 2024, vehicles equipped with manual transmissions accounted for nearly thirty percent of total global production. This continued presence supports consistent demand for clutch and gear control cables across passenger vehicles and light-duty vehicle categories. While advancements in vehicle electronics and automated systems are influencing component design, these developments are not expected to significantly reduce the overall volume of control cables required within the automotive sector.

The brake cables segment held 23.3% share in 2025 and is expected to grow at a CAGR of 5% from 2026 to 2035. Brake cable systems remain a fundamental component in vehicle safety mechanisms, which supports their continued importance across passenger and commercial vehicle categories worldwide. Regulatory frameworks focused on vehicle safety standards contribute to consistent demand for reliable braking systems that require durable control cables. In addition to original equipment demand, brake cables experience frequent wear due to regular vehicle operation, which increases the need for replacement parts throughout the lifespan of vehicles. As a result, brake cable systems contribute significantly to the overall volume of control cables sold across both OEM and aftermarket segments within the automotive control cables market.

Based on material type, the steel segment held a 44.6% share in 2025 and is projected to grow at a CAGR of 3.7% between 2026 and 2035. Steel cables remain widely preferred for automotive applications that require strong tensile performance and high load-bearing capacity to maintain reliable mechanical operation. These characteristics are particularly important in vehicle systems where durability and consistent performance are required over extended operating cycles. Steel-based cables also demonstrate strong resistance to mechanical stress and environmental conditions, making them suitable for long-term use in various vehicle platforms. Due to their established reliability and performance characteristics, automotive manufacturers continue to rely on steel control cables for large-scale vehicle production across multiple automotive segments.

China Automotive Control Cables Market held 53% share, generating USD 1.4 billion in 2025. The country represents a critical hub for automotive manufacturing due to its extensive vehicle production capacity and large installed vehicle base. High production volumes across passenger vehicles, commercial vehicles, and two-wheeler segments contribute to sustained demand for original equipment control cable systems. The continuous expansion of the vehicle population also creates substantial demand for aftermarket replacement components. Vehicles operating in densely populated urban and semi-urban environments often experience frequent start-and-stop driving conditions, which can accelerate wear in mechanical cable systems. As a result, replacement demand remains strong, reinforcing China's position as one of the most significant markets for automotive control cable production and consumption within the Asia Pacific region.

Major companies operating in the Global Automotive Control Cables Market include Atsumitec, Chuo Spring, Dura Automotive Systems, Ficosa International, Grand Rapids Controls, Hi-Lex, Kuster, Minda, Suprajit Engineering, and TSC. Companies competing in the Automotive Control Cables Market are adopting a range of strategic initiatives to strengthen their competitive positions and expand global market presence. Manufacturers are focusing on product innovation by developing advanced cable systems that offer improved durability, flexibility, and performance across diverse vehicle applications. Many companies are also investing in expanding production facilities and strengthening supply chain capabilities to support growing demand from automotive manufacturers worldwide. Strategic collaborations with vehicle manufacturers are helping suppliers integrate control cable systems into next-generation vehicle platforms. In addition, companies are expanding their aftermarket distribution networks to capture the growing demand for replacement components as the global vehicle fleet ages.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cable

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle parc

- 3.2.1.2 Sustained demand for mechanical systems

- 3.2.1.3 Increasing average vehicle age

- 3.2.1.4 Growth in emerging automotive markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Shift toward electronic actuation systems

- 3.2.2.2 Price sensitivity in aftermarket

- 3.2.3 Market opportunities

- 3.2.3.1 Rising electric vehicle production

- 3.2.3.2 Expansion of organized aftermarket

- 3.2.3.3 Localization of component manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States automotive safety and mechanical control component regulations

- 3.4.1.2 Federal motor vehicle safety standards related to braking and control systems

- 3.4.1.3 Vehicle durability and performance compliance requirements

- 3.4.1.4 Canada automotive component safety and quality regulations

- 3.4.2 Europe

- 3.4.2.1 European Union automotive safety and component compliance framework

- 3.4.2.2 ECE regulations for braking and mechanical control systems

- 3.4.2.3 Country level automotive component certification requirements

- 3.4.2.4 Environmental and material compliance rules for automotive cables

- 3.4.3 Asia Pacific

- 3.4.3.1 China automotive component standards and quality regulations

- 3.4.3.2 India automotive safety and component homologation standards

- 3.4.3.3 Japan vehicle safety and mechanical control system guidelines

- 3.4.3.4 South Korea automotive component quality and durability standards

- 3.4.3.5 ASEAN regional automotive component regulatory frameworks

- 3.4.4 Latin America

- 3.4.4.1 Brazil automotive safety and component compliance regulations

- 3.4.4.2 Argentina vehicle component quality requirements

- 3.4.4.3 Mexico automotive manufacturing and safety standards

- 3.4.4.4 Regional automotive component regulatory frameworks

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE automotive safety and vehicle component regulations

- 3.4.5.2 Saudi Arabia vehicle safety and mechanical system compliance

- 3.4.5.3 South Africa automotive component standards and road safety requirements

- 3.4.5.4 Regional automotive regulatory frameworks

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Drive by Wire Technology Substitution Threat

- 3.13.1 Electronic Throttle Control Penetration

- 3.13.2 Electronic Parking Brake Adoption Rates

- 3.13.3 Shift by Wire Transmission Systems

- 3.13.4 Cost Benefit Analysis Mechanical versus Electronic Systems

- 3.14 Geographic Manufacturing Cluster Analysis

- 3.14.1 Major Manufacturing Hubs by Region

- 3.14.2 Proximity to OEM Facility Requirements

- 3.14.3 Regional Production Capacity Distribution

- 3.14.4 Manufacturing Consolidation versus Distributed Models

- 3.15 Patent Monetization and IP Value Creation

- 3.15.1 Licensing Revenue Opportunities

- 3.15.2 Patent Portfolio Valuation

- 3.15.3 Cross Licensing Agreements

- 3.15.4 Defensive Patent Strategies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Cable, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Clutch cables

- 5.3 Accelerator cables

- 5.4 Brake cables

- 5.5 Gear shift cables

- 5.6 Handbrake cables

- 5.7 Throttle cables

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 PVC (Polyvinyl Chloride)

- 6.4 Nylon

- 6.5 Rubber coated

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

- 7.4 Two-wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Engine control

- 8.3 Transmission control

- 8.4 Braking system

- 8.5 HVAC system

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Atsumitec

- 11.1.2 Cofle

- 11.1.3 Dura Automotive Systems

- 11.1.4 Ficosa International

- 11.1.5 Hi-Lex

- 11.1.6 Kuster

- 11.1.7 Kyung Chang Industrial

- 11.1.8 Nippon Cable System

- 11.1.9 Sila

- 11.1.10 Suprajit Engineering

- 11.2 Regional Players

- 11.2.1 Cable Manufacturing & Assembly

- 11.2.2 Cablecraft Motion Controls

- 11.2.3 Chuo Spring

- 11.2.4 GEMO

- 11.2.5 Grand Rapids Controls

- 11.2.6 Minda

- 11.2.7 Tata AutoComp Systems

- 11.2.8 Thai Steel Cable

- 11.2.9 WR Controls

- 11.3 Emerging Players / Disruptors

- 11.3.1 Acey Engineering

- 11.3.2 Kalpa Industries

- 11.3.3 KALTROL

- 11.3.4 Premier Auto Cables

- 11.3.5 Remsons Industries

- 11.3.6 Silco Automotive Solutions

电动车电缆市场:依导体材料、绝缘材料、车辆类型、电压等级及应用划分-2026-2032年全球市场预测汽车电缆市场:2026年至2032年全球市场预测(依电缆类型、车辆类型、绝缘方式、导体材料、电压等级、应用领域及销售管道)高压汽车市场:按组件类型、推进系统、车辆类型、应用、应用领域和最终用户划分-2026年至2032年全球预测

电动车电缆市场:依导体材料、绝缘材料、车辆类型、电压等级及应用划分-2026-2032年全球市场预测汽车电缆市场:2026年至2032年全球市场预测(依电缆类型、车辆类型、绝缘方式、导体材料、电压等级、应用领域及销售管道)高压汽车市场:按组件类型、推进系统、车辆类型、应用、应用领域和最终用户划分-2026年至2032年全球预测 2026年全球汽车电缆市场报告2026年全球高清多媒体介面(HDMI)汽车线市场报告

2026年全球汽车电缆市场报告2026年全球高清多媒体介面(HDMI)汽车线市场报告 中重型商用车点火电缆市场-全球产业规模、份额、趋势、机会及预测(依燃料类型、需求类别、地区及竞争格局划分,2021-2031年)乘用车点火电缆市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)摩托车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)汽车油门拉索市场 - 全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、销售管道类型、地区和竞争格局划分,2021-2031年汽车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、燃料类型、需求类别、地区和竞争格局划分,2021-2031年)

中重型商用车点火电缆市场-全球产业规模、份额、趋势、机会及预测(依燃料类型、需求类别、地区及竞争格局划分,2021-2031年)乘用车点火电缆市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)摩托车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)汽车油门拉索市场 - 全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、销售管道类型、地区和竞争格局划分,2021-2031年汽车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、燃料类型、需求类别、地区和竞争格局划分,2021-2031年)