|

市场调查报告书

商品编码

1998699

冠状动脉支架市场机会、成长要素、产业趋势分析及2026-2035年预测。Coronary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

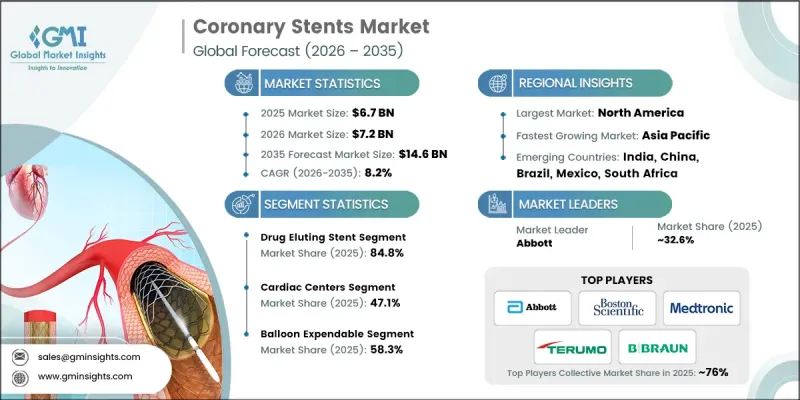

预计到 2025 年,全球冠状动脉支架市场价值将达到 67 亿美元,并有望以 8.2% 的复合年增长率成长,到 2035 年达到 146 亿美元。

市场成长主要受心血管疾病盛行率上升、人口老化、支架技术进步、微创手术日益普及等因素所驱动。冠状动脉支架是一种管状医疗设备,植入狭窄或阻塞的冠状动脉,在维持血管通畅性、改善血流和预防心肌梗塞方面发挥重要作用。冠状动脉疾病是全球主要死因之一,其发生率的不断上升正在推动市场需求。药物释放型支架、生物可吸收支架和无聚合物支架等技术创新透过最大限度地减少血管再阻塞和血栓症形成,改善了长期治疗效果。患者意识的提高、临床医生信心的增强以及血管重建手术的扩展进一步推动了支架的普及。药物释放型支架和生物可降解支架的普及以及以患者为中心的治疗方法等趋势正在塑造全球重组行业的成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 67亿美元 |

| 预计金额 | 146亿美元 |

| 复合年增长率 | 8.2% |

预计到2025年,药物释放型支架市场份额将达到84.8%,这主要得益于其能够最大限度地减少血管再阻塞、改善患者长期预后并支持微创治疗。药物释放型支架透过释放药物来抑制组织过度增生,与裸金属支架相比,可带来更优的长期疗效,这也推动了其在临床实践中的广泛应用。

预计2035年,钴铬合金支架市场规模将达75亿美元。钴铬合金支架具有高抗拉强度和耐久性,即使在动脉受压的情况下也能保持血管扩张,从而实现更细的支架梁设计。这些更细的支架梁透过减少动脉损伤、改善血流、促进癒合以及最大限度地降低血管再阻塞和血栓症形成的风险,推动了该细分市场的成长。

预计到2025年,北美冠状动脉支架市占率将达到39.6%。在美国,由于久坐不动的生活方式、高脂肪饮食和压力等因素,心血管疾病负担日益加重,这推动了冠状动脉支架置入术的需求。该地区先进的医疗基础设施、专业的冠心病中心和技术精湛的医务人员使得支架置入术得以广泛开展。医院和介入性冠心病中心对创新支架技术的应用,进一步促进了该地区的市场成长。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策和资料完整性倡议

- 资讯来源一致性通讯协定

- GMI人工智慧政策和资料完整性倡议

- 调查过程和可靠性评分

- 调查过程的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 每种方法中基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 冠状动脉疾病盛行率上升

- 对微创手术的需求日益增长

- 开发中国家的技术进步

- 人们对心臟病预防保健的认识和关注度不断提高

- 产业潜在风险与挑战

- 产品缺陷和召回

- 严格的监管核准

- 开发中国家缺乏熟练的医护人员

- 市场机会

- 生物可吸收支架和下一代支架的研发

- 数位健康与医学影像技术的融合

- 促进因素

- 成长潜力分析

- 监理情势(基于初步调查)

- 北美洲

- 欧洲

- 亚太地区

- 科技趋势

- 当前技术趋势

- 新兴技术

- 还款方案(基于初步调查)

- 未来市场趋势

- 价格分析(2025 年)(基于初步调查)

- 波特五力分析

- PESTEL 分析

- 客户洞察(基于初步研究)

- Start-Ups场景

- 人工智慧和生成式人工智慧对市场的影响

- 投资环境

- 差距分析

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析(基于初步研究)

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 竞争定位矩阵

- 主要市场公司的竞争分析

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 药物释放型支架

- 生物可吸收血管支架(BVS)

- 裸金属支架

第六章 市场估计与预测:依类型划分,2022-2035年

- 球囊式一次性支架

- 自吸收支架

第七章 市场估计与预测:依材料划分,2022-2035年

- 钴铬合金

- 不銹钢

- 其他材料

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 心臟中心

- 医院

- 门诊手术中心

- 其他最终用户

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Abbott

- Andramed

- B. Braun

- Biosensors International Group

- Biotronik

- Boston Scientific

- Cook Medical

- Elixir Medical

- GENOSS

- Medtronic

- Meril Life Science

- MicroPort Scientific

- Sahajanand Laser Technology Limited

- Stryker

- Terumo

The Global Coronary Stents Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 14.6 billion by 2035.

Market growth is driven by the rising prevalence of cardiovascular diseases, an aging population, advancements in stent technologies, and the increasing adoption of minimally invasive procedures. Coronary stents are tubular devices inserted into narrowed or blocked coronary arteries to maintain vessel patency, enhance blood flow, and prevent heart attacks. The growing incidence of coronary artery disease, a leading cause of mortality worldwide, is fueling demand. Technological innovations such as drug-eluting stents, bioresorbable scaffolds, and polymer-free stents improve long-term outcomes by minimizing restenosis and thrombosis. Rising patient awareness, clinician confidence, and the expansion of revascularization procedures further support adoption. Trends such as the shift toward drug-eluting and biodegradable stents, as well as patient-centric approaches, are shaping industry growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 8.2% |

The drug-eluting stent segment held a share of 84.8% in 2025 owing to its ability to minimize restenosis, enhance long-term patient outcomes, and support minimally invasive interventions. Drug-eluting stents release medication to prevent excessive tissue growth, providing superior long-term results compared to bare-metal stents, which reinforces their widespread clinical adoption.

The cobalt-chromium alloy segment is expected to reach USD 7.5 billion by 2035. Cobalt-chromium stents offer high tensile strength and durability, maintaining vessel expansion under arterial pressure while allowing thinner strut designs. These thinner struts reduce arterial injury, improve blood flow, and accelerate healing, while minimizing the risk of restenosis and thrombosis, driving segment growth.

North America Coronary Stents Market held a 39.6% share in 2025. The U.S. faces a significant burden of cardiovascular diseases, driven by sedentary lifestyles, high-fat diets, and stress, which increases the demand for coronary stent procedures. The region's advanced healthcare infrastructure, specialized cardiac centers, and skilled medical professionals ensure widespread availability of stenting procedures. The adoption of innovative stent technologies across hospitals and interventional cardiology centers further fuels regional growth.

Prominent players in the Global Coronary Stents Market include Abbott, Medtronic, Boston Scientific, Biotronik, MicroPort Scientific, Stryker, Terumo, B. Braun, Biosensors International Group, Cook Medical, GENOSS, Elixir Medical, Andramed, Meril Life Science, and Sahajanand Laser Technology Limited. Companies in the Global Coronary Stents Market are strengthening their positions through continuous research and development to enhance stent safety, performance, and drug delivery capabilities. Firms are expanding their global footprint by entering emerging markets and forging partnerships with hospitals and healthcare providers. They focus on patient-centric and minimally invasive solutions, including bioresorbable and polymer-free stents, while integrating digital monitoring and smart stent technologies. Strategic marketing campaigns, clinician training programs, and collaborations with leading cardiac centers help companies improve adoption, build brand trust, and maintain a competitive edge in the global coronary stents industry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Material trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of coronary artery disease

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancement in developing economies

- 3.2.1.4 Increasing awareness and focus on preventive cardiac care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Product failure and recall

- 3.2.2.2 Stringent regulatory approvals

- 3.2.2.3 Dearth of skilled healthcare professional in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Development of bioresorbable and next-generation stents

- 3.2.3.2 Integration of digital health & imaging technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends

- 3.8 Pricing analysis, 2025 (Driven by primary research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Customer insights (Driven by primary research)

- 3.12 Start-up scenarios

- 3.13 Impact of AI and generative AI on the market

- 3.14 Investment landscape

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Drug eluting stent

- 5.3 Bioresorbable vascular scaffold (BVS)

- 5.4 Bare metal stent

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Balloon expendable stent

- 6.3 Self-expendable stent

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cobalt-chromium alloy

- 7.3 Stainless steel

- 7.4 Other materials

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Cardiac centers

- 8.3 Hospitals

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 Andramed

- 10.3 B. Braun

- 10.4 Biosensors International Group

- 10.5 Biotronik

- 10.6 Boston Scientific

- 10.7 Cook Medical

- 10.8 Elixir Medical

- 10.9 GENOSS

- 10.10 Medtronic

- 10.11 Meril Life Science

- 10.12 MicroPort Scientific

- 10.13 Sahajanand Laser Technology Limited

- 10.14 Stryker

- 10.15 Terumo

全球冠状动脉支架市场规模、份额、趋势和成长分析报告(2026-2034年)

全球冠状动脉支架市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球冠状动脉支架市场报告

2026年全球冠状动脉支架市场报告 冠状动脉支架市场分析及预测(至2035年):类型、产品类型、技术、材质类型、应用、最终用户、器材、製程、安装方式全球冠状动脉支架市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034)

冠状动脉支架市场分析及预测(至2035年):类型、产品类型、技术、材质类型、应用、最终用户、器材、製程、安装方式全球冠状动脉支架市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034) 日本冠状动脉支架市场报告(按类型、生物材料、输送方式、最终用户和地区划分,2026-2034 年)

日本冠状动脉支架市场报告(按类型、生物材料、输送方式、最终用户和地区划分,2026-2034 年) 冠状动脉支架市场规模、份额和成长分析(按类型、输送方式、材料、最终用户和地区划分)—产业预测(2026-2033 年)

冠状动脉支架市场规模、份额和成长分析(按类型、输送方式、材料、最终用户和地区划分)—产业预测(2026-2033 年) 冠状动脉支架市场按产品类型、材料、最终用户和地区划分

冠状动脉支架市场按产品类型、材料、最终用户和地区划分 冠状动脉支架市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035)

冠状动脉支架市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035) 冠状动脉支架市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年

冠状动脉支架市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年 冠状动脉支架的开发平台 - 开发阶段,市场区隔,地区和国家,法规途径,主要企业(2024年版)

冠状动脉支架的开发平台 - 开发阶段,市场区隔,地区和国家,法规途径,主要企业(2024年版)