|

市场调查报告书

商品编码

1998700

心房颤动治疗设备市场:商业机会、成长要素、产业趋势分析及 2026-2035 年预测。Atrial Fibrillation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

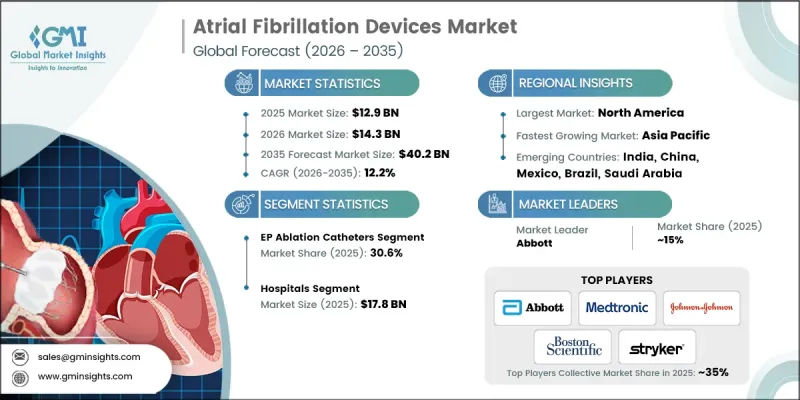

2025 年全球心房颤动治疗设备市场规模预估为 129 亿美元,预计到 2035 年将达到 402 亿美元,年复合成长率为 12.2%。

心房颤动治疗设备的持续技术创新、心房颤动盛行率的上升、心导管电气烧灼术手术的日益普及以及人们对早期诊断和治疗意识的提高,共同推动了市场扩张。心房颤动治疗设备,例如消融导管、植入式心臟监测器、心律调节器和去心房颤动,旨在恢復正常心率、预防中风并缓解心房颤动相关症状。公共卫生宣传活动和患者教育计画正在推广早期发现和及时干预,从而增加了对诊断和监测设备的需求。微创手术、穿戴式和远端监测技术以及混合治疗方法的日益普及,进一步加速了市场成长。能量输送系统、精准标靶和设备小型化的持续创新,正在拓展心房颤动的治疗选择并改善治疗效果。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 129亿美元 |

| 预测金额 | 402亿美元 |

| 复合年增长率 | 12.2% |

至2025年,电生理消融导管市占率将达到30.6%,在导管消融手术中扮演核心角色。这些器械能够实现精准的病灶形成、提高组织标靶精度并提升手术成功率,使其成为电生理医师的首选。灌注导管尖端、接触力感测技术和增强型能量输送系统等创新技术正在提高病患安全性、提升手术效率、缩短治疗时间,并促进其进一步普及应用。

预计到2025年,医院市场将占据43.7%的份额,到2035年将达到178亿美元。这项需求主要由医院内专门的心房颤动治疗中心推动,这些中心需要配备全面的医疗设备,用于诊断、治疗和病患监测。认证项目和品质改进计划正在促进医院采购先进的房颤治疗设备,并提高市场渗透率。

预计到2025年,北美心房颤动治疗设备市占率将达到40.6%。这一增长主要受心房颤动高发生率、人口老化以及高血压、糖尿病和肥胖等心血管危险因子发病率上升的推动。该地区高昂的医疗费用支出支持了对先进心房颤动技术的投资,包括消融导管、心律调节器和诊断设备。医疗机构对创新解决方案的早期应用,以及人均心臟护理支出,进一步促进了该地区市场的成长。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策和资料完整性倡议

- 资讯来源一致性通讯协定

- GMI人工智慧政策和资料完整性倡议

- 调查过程和可靠性评分

- 调查过程的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 每种方法中基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 先进技术的高普及率和先进医疗基础设施的发展

- 心血管疾病盛行率增加

- 有利的赎回环境

- 风湿性心臟瓣膜疾病盛行率增加

- 产业潜在风险与挑战

- 心房颤动治疗设备高成本

- 开发中国家对先进医疗技术的认知度较低

- 市场机会

- 微创和导管介入治疗方法的扩展

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 技术趋势(基于初步调查)

- 当前技术趋势

- 新兴技术

- 未来市场趋势(基于初步研究)

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 区域心导管电气烧灼术中心,2022-2025 年

- 专利分析

- 价格分析(2025 年)(基于初步调查)

- 客户洞察

- 人工智慧和生成式人工智慧对市场的影响

- 波特五力分析

- PESTEL 分析

- 差距分析

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 竞争定位矩阵

- 主要市场公司的竞争分析

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品类型发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 电生理消融导管

- 射频(RF)

- 雷射

- 冷冻消融术

- 超音波

- 微波

- 其他电生理消融导管

- 心臟监测仪或植入式循环记录仪

- 电生理诊断导管

- 进阶标测导管

- 可插入导管

- 固定弯曲导管

- 地图绘製与记录系统

- 存取装置

- 心内超音波心动图(ICE)

- 左心耳封堵器

- 其他产品

第六章 市场估算与预测:依最终用途划分,2022-2035年

- 医院

- 心臟中心

- 门诊手术中心

- 其他最终用户

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章:公司简介

- Abbott

- Acutus Medical

- AtriCure

- Biotronik

- Boston Scientific Corporation

- CardioFocus

- CathRx

- Hansen Medical

- Imricor

- Johnson and Johnson

- Medtronic

- MicroPort Scientific Corporation

- OSYPKA MEDICAL

- Stryker Corporation

- Synaptic Medical

The Global Atrial Fibrillation Devices Market was valued at USD 12.9 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 40.2 billion by 2035.

Market expansion is driven by ongoing technological innovations in AF devices, the rising prevalence of atrial fibrillation, increasing adoption of cardiac ablation procedures, and heightened awareness about early diagnosis and management. AF devices, including ablation catheters, implantable cardiac monitors, pacemakers, and defibrillators, are designed to restore normal heart rhythm, prevent stroke, and reduce AF-related symptoms. Public health campaigns and patient education programs are promoting early detection and timely intervention, boosting demand for diagnostic and monitoring tools. Minimally invasive procedures, wearable and remote monitoring technologies, and hybrid treatment approaches are gaining traction, further accelerating market growth. Continuous innovation in energy delivery systems, precision targeting, and device miniaturization is expanding AF treatment options and improving procedural outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.9 Billion |

| Forecast Value | $40.2 Billion |

| CAGR | 12.2% |

The EP ablation catheters segment held a 30.6% share in 2025 owing to their central role in catheter-based ablation procedures. These devices allow precise lesion formation, improved tissue targeting, and higher procedural success rates, making them the preferred choice among electrophysiologists. Innovations such as irrigated tip catheters, contact force-sensing technology, and enhanced energy delivery systems are improving patient safety, increasing procedural efficiency, reducing treatment time, and driving further adoption.

The hospitals segment captured a 43.7% share in 2025 and is expected to reach USD 17.8 billion by 2035. Demand is being fueled by specialized AF treatment centers within hospitals, which require comprehensive device inventories for diagnosis, treatment, and patient monitoring. Accreditation programs and quality improvement initiatives motivate hospitals to procure advanced AF devices, increasing market uptake.

North America Atrial Fibrillation Devices Market held a 40.6% share in 2025, driven by a high prevalence of atrial fibrillation, an aging population, and the rising incidence of cardiovascular risk factors such as hypertension, diabetes, and obesity. The region's substantial healthcare expenditure supports investment in advanced AF technologies, including ablation catheters, pacemakers, and diagnostic devices. Early adoption of innovative solutions by healthcare providers, along with per capita spending on cardiac care, further strengthens regional growth.

Prominent players in the Global Atrial Fibrillation Devices Market include Abbott, Acutus Medical, AtriCure, Biotronik, Boston Scientific Corporation, CardioFocus, CathRx, Hansen Medical, Imricor, Johnson and Johnson, Medtronic, MicroPort Scientific Corporation, OSYPKA MEDICAL, Stryker Corporation, and Synaptic Medical. Key strategies adopted by companies in minimally invasive, energy-efficient, and precision ablation technologies; expanding product portfolios to include remote monitoring and wearable solutions; forming strategic partnerships with hospitals, clinics, and diagnostic centers; pursuing regulatory approvals and certifications to enter new markets; enhancing global distribution networks to improve accessibility; and implementing patient awareness campaigns to drive early diagnosis. Firms also focus on clinician training programs, after-sales service, and hybrid procedural solutions to strengthen their market footprint, build brand loyalty, and maintain competitive advantage.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High adoption rate of advanced technologies and presence of sophisticated healthcare infrastructure

- 3.2.1.2 Increase in prevalence of cardiovascular diseases

- 3.2.1.3 Favorable reimbursement scenario

- 3.2.1.4 Rise in prevalence of rheumatic valvular heart diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with atrial fibrillation devices

- 3.2.2.2 Lack of awareness regarding enhanced medical technologies in developing countries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of minimally invasive and catheter-based therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Atrial fibrillation devices market, 2022 -2035 (Units)

- 3.7.1 Global

- 3.7.2 North America

- 3.7.3 Europe

- 3.7.4 Asia Pacific

- 3.7.5 Latin America

- 3.7.6 MEA

- 3.8 Catheter ablation centres, by region, 2022 - 2025

- 3.9 Patent analysis

- 3.10 Pricing analysis, 2025 (Driven by Primary Research)

- 3.11 Customer insights

- 3.12 Impact of AI and generative AI on the market

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 EP ablation catheters

- 5.2.1 Radiofrequency (RF)

- 5.2.2 Laser

- 5.2.3 Cryoablation

- 5.2.4 Ultrasound

- 5.2.5 Microwave

- 5.2.6 Other EP ablation catheters

- 5.3 Cardiac monitors or implantable loop recorder

- 5.4 EP diagnostic catheters

- 5.4.1 Advanced mapping catheters

- 5.4.2 Steerable catheters

- 5.4.3 Fixed curve catheters

- 5.5 Mapping and recording systems

- 5.6 Access devices

- 5.7 Intracardiac echocardiography (ICE)

- 5.8 Left atrial appendage (LAA) closure devices

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Cardiac centers

- 6.4 Ambulatory surgical centers

- 6.5 Other end-users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Acutus Medical

- 8.3 AtriCure

- 8.4 Biotronik

- 8.5 Boston Scientific Corporation

- 8.6 CardioFocus

- 8.7 CathRx

- 8.8 Hansen Medical

- 8.9 Imricor

- 8.10 Johnson and Johnson

- 8.11 Medtronic

- 8.12 MicroPort Scientific Corporation

- 8.13 OSYPKA MEDICAL

- 8.14 Stryker Corporation

- 8.15 Synaptic Medical

2026-2034年全球心房颤动治疗设备市场规模、份额、趋势和成长分析报告

2026-2034年全球心房颤动治疗设备市场规模、份额、趋势和成长分析报告 穿戴式心房颤动监测设备市场(按设备类型、技术、最终用户、分销管道和应用划分),全球预测(2026-2032年)

穿戴式心房颤动监测设备市场(按设备类型、技术、最终用户、分销管道和应用划分),全球预测(2026-2032年) 2026年全球心房颤动治疗设备市场报告2026-2034年全球心房颤动市场规模、份额、趋势和成长分析报告2026-2034年全球心房颤动治疗市场规模、份额、趋势和成长分析报告心房颤动市场-2026-2031年预测心房颤动治疗设备市场按产品类型、技术、最终用户和分销管道划分-2026年至2032年全球预测全球心房颤动市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034 年)

2026年全球心房颤动治疗设备市场报告2026-2034年全球心房颤动市场规模、份额、趋势和成长分析报告2026-2034年全球心房颤动治疗市场规模、份额、趋势和成长分析报告心房颤动市场-2026-2031年预测心房颤动治疗设备市场按产品类型、技术、最终用户和分销管道划分-2026年至2032年全球预测全球心房颤动市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034 年) 心房颤动市场规模、份额和趋势分析报告:按疗法、最终用途、地区和细分市场预测(2026-2033 年)

心房颤动市场规模、份额和趋势分析报告:按疗法、最终用途、地区和细分市场预测(2026-2033 年) 心房颤动市场规模、份额和成长分析(按治疗类型、最终用途和地区划分)—产业预测,2026-2033年

心房颤动市场规模、份额和成长分析(按治疗类型、最终用途和地区划分)—产业预测,2026-2033年