|

市场调查报告书

商品编码

1998723

防潮层市场商机、成长要素、产业趋势分析及2026-2035年预测。Vapor Barriers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

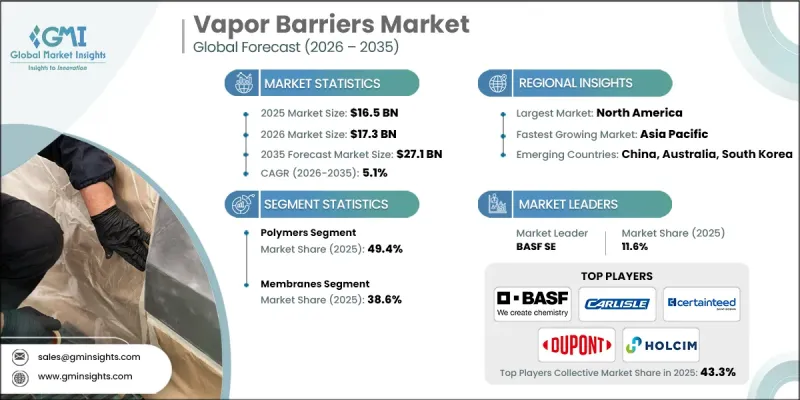

全球防潮材料市场预计到 2025 年将价值 165 亿美元,预计到 2035 年将以 5.1% 的复合年增长率增长至 271 亿美元。

住宅和商业建筑对高效防潮解决方案的需求日益增长,推动了防潮屏障市场的发展。建筑商和开发人员越来越重视那些有助于维持室内空气品质、降低能耗和提高建筑耐久性的建筑材料。防潮屏障在实现这些目标中发挥着至关重要的作用,它可以防止水分渗入,从而避免影响保温性能和结构完整性。人们对永续建筑实践的日益关注也促进了对先进防潮屏障的需求成长。绿建筑框架(包括LEED认证标准等措施)的推广,正在推动防潮节能建筑材料的使用。业界的技术进步,例如引入旨在提升性能和简化安装的创新材料技术,进一步促进了市场发展。此外,新兴国家建设活动的活性化以及老旧建筑为符合现代能源效率标准而进行的维修,也为市场扩张创造了巨大的机会。随着永续性意识的不断提高和建筑法规的不断完善,预计全球建筑市场对环保防潮解决方案的需求将保持强劲。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 165亿美元 |

| 预测金额 | 271亿美元 |

| 复合年增长率 | 5.1% |

预计到2025年,聚合物产业将占据49.4%的市场份额,并在2035年之前以5.2%的复合年增长率成长。聚合物基材料凭藉其耐久性、成本效益和卓越的防潮性能,保持着市场主导地位。这些材料具有高度的柔软性和适应性,使承包商能够将其应用于各种建筑环境中。此外,其轻质结构简化了安装过程,製造商还可以生产多种厚度的防潮解决方案,以满足不同的施工需求。这些优势持续推动聚合物基防潮材料在现代建筑计划中的广泛应用。

到2025年,膜材将占据38.6%的市场。膜材防潮层因其高效的防水防潮性能而被广泛应用。其结构特性确保了在住宅和产业建设环境中的可靠性能,在这些环境中,湿度控制对于维持建筑性能至关重要。此外,膜材的轻量特性使其安装过程更加快速且有效率。随着节能建筑解决方案和环保建筑方法的需求不断增长,膜材防潮系统越来越能满足现代建筑技术不断发展的需求。

预计2026年至2035年,北美防潮层市场将以4.8%的复合年增长率成长。随着建设公司采用先进的防潮层系统来改善隔热性能并增强建筑耐久性,全部区域的需求正在不断增长。人们对环保施工实践和节能建筑设计的日益关注,也持续推动高性能防潮层的应用。此外,建筑法规和环境标准的修订正在促进使用符合永续建筑目标的材料,进一步推动了全部区域市场的扩张。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 人们越来越意识到节能和永续建筑的重要性

- 政府对计划中的能源效率和湿度控制制定相关法规

- 绿建筑认证(例如 LEED)鼓励使用防潮层等材料来满足环境标准。

- 产业潜在风险与挑战

- 必须仔细选择防潮层,并考虑其与各种建筑材料的兼容性。

- 市场机会

- 对永续和环保防潮层的需求日益增长

- 新兴市场建设活动增加

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 材料

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依材料划分,2022-2035年

- 聚合物

- 聚乙烯

- 聚丙烯

- 聚氯乙烯

- 其他的

- 玻璃

- 玻璃纤维

- 玻璃纤维增强材料

- 金属

- 铝箔

- 金属化薄膜

- 铁和铜

- 石膏板

- 其他的

第六章 市场估算与预测:依设备类型划分,2022-2035年

- 电影

- 涂层

- 水泥基防水材料

- 层压和填充

第七章 市场估价与预测:依通路划分,2022-2035年

- 隔热材料

- 空腔隔热

- 连续隔热材料

- 喷涂泡沫隔热材料

- 硬质板隔热材料

- 防水的

- 耐腐蚀性

- 金属结构的保护

- 钢筋混凝土防护

- 工业设备的保护

- 其他的

第八章 市场估算与预测:依最终用途划分,2022-2035年

- 建造

- 住宅

- 商业建筑

- 产业建设

- 包装

- 车

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- BASF SE

- 凯雷集团

- CertainTeed Corporation

- DuPont

- GAF Materials LLC

- GCP Applied Technologies

- Holcim

- Johns Manville

- Polyguard

- Sika AG

- Soprema Group

- Tremco

- VaproShield

- WR Meadows

The Global Vapor Barriers Market was valued at USD 16.5 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 27.1 billion by 2035.

Growth in the vapor barriers market is driven by the increasing need for effective moisture management solutions in both residential and commercial construction. Builders and developers are increasingly prioritizing materials that help maintain indoor air quality, reduce energy consumption, and improve building durability. Vapor barriers play an important role in achieving these goals by preventing moisture infiltration that can compromise insulation performance and structural integrity. Rising awareness regarding sustainable construction methods is also contributing to the growing demand for advanced vapor barrier materials. The adoption of green building frameworks, including initiatives such as LEED certification standards, is encouraging the use of moisture-resistant and energy-efficient construction components. Technological progress within the industry is further supporting market development through the introduction of innovative material technologies designed to enhance performance and ease of installation. In addition, increasing construction activity in developing economies and the renovation of aging buildings to comply with modern energy efficiency standards are creating significant opportunities for market expansion. As sustainability awareness continues to grow and building regulations evolve, demand for environmentally responsible moisture control solutions is expected to remain strong across global construction markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.5 Billion |

| Forecast Value | $27.1 Billion |

| CAGR | 5.1% |

The polymer segment accounted for 49.4% share in 2025 and is anticipated to grow at a CAGR of 5.2% through 2035. Polymer-based materials maintain a leading position in the market due to their durability, cost efficiency, and effective moisture resistance. These materials provide strong flexibility and adaptability, allowing contractors to apply them across a wide range of construction environments. Their lightweight structure also simplifies installation processes while enabling manufacturers to produce vapor barrier solutions in multiple thicknesses that suit varying construction requirements. These advantages continue to support the widespread use of polymer-based vapor barrier materials in modern building projects.

The membrane segment held 38.6% share in 2025. Membrane-based vapor barriers are widely used because they provide highly effective waterproofing and moisture protection capabilities. Their structural properties allow them to perform reliably in both residential and industrial construction environments where moisture control is essential for maintaining building performance. In addition, the lightweight composition of membrane materials allows for faster and more efficient installation processes. As demand for energy-efficient construction solutions and environmentally responsible building practices continues to grow, membrane-based vapor barrier systems are increasingly aligned with the evolving needs of modern construction technologies.

North America Vapor Barriers Market will grow at a CAGR of 4.8% between 2026 and 2035. Demand across the region is rising as construction companies adopt advanced moisture protection systems that improve insulation performance and enhance building durability. Increasing interest in environmentally responsible construction methods and energy-efficient building designs continues to encourage the adoption of high-performance vapor barrier materials. Furthermore, updated building regulations and environmental standards are promoting the use of materials that support sustainable construction objectives, which is further contributing to market expansion across the region.

Key companies operating in the Global Vapor Barriers Market include DuPont, BASF SE, Carlisle Companies, Sika AG, Holcim, CertainTeed Corporation, Johns Manville, GAF Materials LLC, Soprema Group, Polyguard, Tremco, GCP Applied Technologies, VaproShield, and W.R. Meadows. Companies operating in the Global Vapor Barriers Market are focusing on multiple strategic initiatives to strengthen their market position and expand their global presence. Leading manufacturers are investing in research and development to introduce advanced materials that provide improved moisture resistance, durability, and energy efficiency. Many firms are also emphasizing environmentally sustainable product development by incorporating recyclable materials and low-emission manufacturing processes into their product portfolios. Strategic collaborations with construction companies and infrastructure developers are helping manufacturers integrate vapor barrier solutions into large-scale building projects. In addition, companies are expanding production capabilities and strengthening distribution networks to ensure a consistent supply across regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Installation

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing awareness of energy conservation and sustainable building

- 3.2.1.2 Government regulations on energy efficiency and moisture control in construction projects

- 3.2.1.3 Green building certifications (e.g., LEED) is encouraging the adoption of materials like vapor barriers to meet environmental standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Vapor barriers must be carefully selected for compatibility with various construction materials

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable and eco-friendly vapor barrier materials

- 3.2.3.2 Increasing construction activities in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material, 2022-2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Polymers

- 5.2.1 Polyethylene

- 5.2.2 Polypropylene

- 5.2.3 Polyvinyl chloride

- 5.2.4 Others

- 5.3 Glass

- 5.3.1 Fiberglass

- 5.3.2 Glass fiber reinforced materials

- 5.4 Metal

- 5.4.1 Aluminum foil

- 5.4.2 Metallized films

- 5.4.3 Steel & copper

- 5.5 Drywall

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Installation, 2022-2035 (USD Billion) ( Tons)

- 6.1 Key trends

- 6.2 Membranes

- 6.3 Coatings

- 6.4 Cementitious waterproofing

- 6.5 Stacking and filling

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Insulation

- 7.2.1 Cavity insulation

- 7.2.2 Continuous insulation

- 7.2.3 Spray foam insulation

- 7.2.4 Rigid board insulation

- 7.3 Waterproofing

- 7.4 Corrosion resistance

- 7.4.1 Metal structure protection

- 7.4.2 Concrete reinforcement protection

- 7.4.3 Industrial equipment protection

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Construction

- 8.2.1 Residential construction

- 8.2.2 Commercial construction

- 8.2.3 Industrial construction

- 8.3 Packaging

- 8.4 Automotive

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Carlisle Companies

- 10.3 CertainTeed Corporation

- 10.4 DuPont

- 10.5 GAF Materials LLC

- 10.6 GCP Applied Technologies

- 10.7 Holcim

- 10.8 Johns Manville

- 10.9 Polyguard

- 10.10 Sika AG

- 10.11 Soprema Group

- 10.12 Tremco

- 10.13 VaproShield

- 10.14 W.R. Meadows

环境雾化器市场:2026-2032年全球市场预测(依产品类型、技术、应用、最终用户及销售管道)

环境雾化器市场:2026-2032年全球市场预测(依产品类型、技术、应用、最终用户及销售管道) 防潮层市场分析与预测(至2035年):类型、材质类型、应用、技术、安装方式、功能、组件、最终用户、形式和解决方案

防潮层市场分析与预测(至2035年):类型、材质类型、应用、技术、安装方式、功能、组件、最终用户、形式和解决方案