|

市场调查报告书

商品编码

1998725

医用胶带及绷带市场:商机、成长要素、产业趋势分析及2026-2035年预测Medical Tapes and Bandages Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

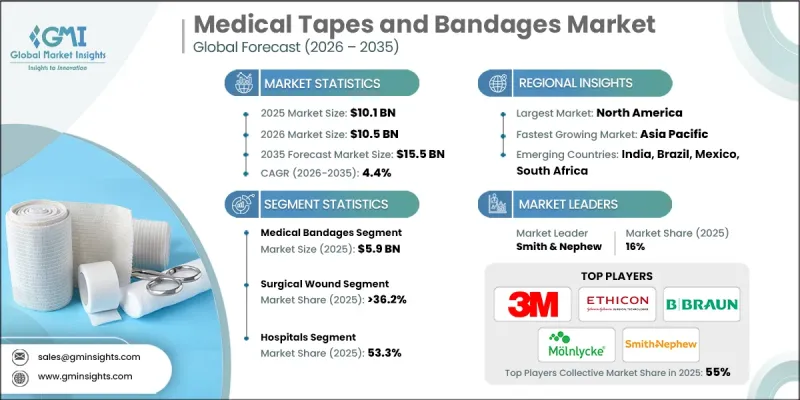

全球医用胶带和绷带市场预计到 2025 年将达到 101 亿美元,年复合成长率为 4.4%,到 2035 年将达到 155 亿美元。

推动市场成长的因素包括运动伤害增加、身体活动参与度提高、外科手术量增加以及糖尿病足併发症、压疮和其他慢性疾病等慢性病的普遍存在。人们对创伤护理、感染预防和先进医用黏合剂的日益重视也促进了市场需求。医用胶带和绷带是用于伤口保护、固定受伤部位和固定医疗设备的重要医疗产品。各公司正致力于为运动员和活跃人群开发亲肤黏合剂、透气材料和耐用绷带,同时也努力满足需要长期照护慢性伤口的患者的需求。压疮和癒合缓慢的伤口仍然是亟待解决的难题,因此,高效能伤口管理解决方案的需求日益增长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 101亿美元 |

| 预测金额 | 155亿美元 |

| 复合年增长率 | 4.4% |

预计到2025年,医用绷带市场规模将达到59亿美元,其中包括棉布绷带、弹性绷带、整形外科绷带、黏性绷带、止血绷带和其他特殊类型的绷带。这些绷带对于急性和慢性伤口的加压、固定和保护至关重要。绷带广泛应用于急诊和创伤护理、术后復原以及糖尿病足溃疡等难癒合伤口的治疗,从而有效预防感染并促进復原。

到2025年,外科性创伤护理市场将占据36.2%的市场。慢性病、创伤和择期手术病例的增加推动了外科手术量的激增,进而带动了对有效伤口管理的需求。由于外科性创伤感染风险较高,因此使用能够促进伤口癒合并降低併发症风险的先进抗菌敷料和绷带至关重要。

到2025年,北美医用胶带和绷带市占率将达到39.8%。该地区完善的医疗保健基础设施、慢性伤口的高发生率以及糖尿病患者数量的不断增长,都推动了对先进创伤护理产品的稳定需求。医院和医疗机构越来越依赖创新胶带和绷带,以确保病人安全、降低感染率并改善復原效果。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 运动伤害和增加的身体活动

- 手术数量增加

- 压疮、糖尿病足併发症和其他疾病导致的负担加重。

- 人们对先进的创伤护理和感染控制产品的认识不断提高

- 产业潜在风险与挑战

- 市场价格敏感度面临的主要挑战

- 市场竞争激烈

- 市场机会

- 拓展门诊与居家照护领域

- 非处方(OTC)创伤护理产品电子商务平台的成长

- 促进因素

- 成长潜力分析

- 监理情势

- 技术进步

- 当前技术趋势

- 新兴技术

- 供应链分析

- 救赎方案

- 2024年价格分析

- 人工智慧和生成式人工智慧对市场的影响

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 医用胶带

- 布料胶带

- 纸胶带

- 塑胶胶带

- 其他磁带

- 医用绷带

- 棉布绷带

- 弹性绷带

- 整形外科绷带

- OK绷

- 止血绷带

- 其他绷带

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 外科性创伤

- 烧伤

- 运动伤害

- 创伤性伤口

- 其他用途

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 诊所

- 居家照护设施

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- 3M

- Johnson &Johnson

- Smith &Nephew

- Hartmann Group

- Covidien(Medtronic)

- Molnlycke Health Care

- Paul Hartmann AG

- Nitto Denko Corporation

- Integra LifeSciences

- B. Braun Melsungen AG

- BSN medical(Essity)

- Ansell

- Dynarex Corporation

- Winner Medical Group

- Cardinal Health AG

The Global Medical Tapes and Bandages Market was valued at USD 10.1 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 15.5 billion by 2035.

The market growth is driven by the rising incidence of sports-related injuries, increased participation in physical activities, growing numbers of surgical procedures, and the prevalence of chronic conditions such as diabetic foot, pressure ulcers, and other long-term ailments. Awareness about wound care, infection prevention, and advanced medical adhesives is also fueling demand. Medical tapes and bandages are critical components in healthcare, used to protect wounds, stabilize injuries, and secure medical devices. Companies are innovating with skin-friendly adhesives, breathable materials, and durable bandages that cater to athletes and active individuals, while also addressing the needs of patients requiring long-term care for chronic wounds. Pressure ulcers and slow-healing injuries continue to pose challenges, driving the adoption of high-performance wound management solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.1 Billion |

| Forecast Value | $15.5 Billion |

| CAGR | 4.4% |

The medical bandages segment generated USD 5.9 billion in 2025 and includes muslin bandages, elastic bandages, orthopedic bandages, adhesive bandages, hemostatic bandages, and other specialized types. These bandages are essential for providing compression, stabilization, and protection for both acute injuries and chronic wounds. Bandages are widely used in emergency and trauma care, post-surgical recovery, and in managing slow-healing wounds like diabetic foot ulcers, ensuring infection prevention and supporting recovery.

The surgical wound care segment held 36.2% share in 2025. The surge in surgical procedures, driven by rising cases of chronic diseases, trauma, and elective surgeries, has increased demand for effective wound management. Surgical wounds are highly susceptible to infections, prompting the use of advanced antimicrobial dressings and bandages that support faster healing and reduce complication risks.

North America Medical Tapes and Bandages Market held 39.8% share in 2025. The region's strong healthcare infrastructure, high prevalence of chronic wounds, and growing diabetes population contribute to consistent demand for advanced wound care products. Hospitals and healthcare providers increasingly rely on innovative tapes and bandages to ensure patient safety, reduce infection rates, and improve recovery outcomes.

Key players in the Global Medical Tapes and Bandages Market include 3M, Johnson & Johnson, Smith & Nephew, Hartmann Group, Covidien (Medtronic), Molnlycke Health Care, Paul Hartmann AG, Nitto Denko Corporation, Integra LifeSciences, B. Braun Melsungen AG, BSN medical (Essity), Ansell, Dynarex Corporation, Winner Medical Group, and Cardinal Health AG. Companies in the Global Medical Tapes and Bandages Market strengthen their position by focusing on product innovation, developing skin-friendly, durable, and antimicrobial tapes and bandages to meet evolving patient needs. Strategic partnerships with hospitals, clinics, and distributors expand their reach and adoption. Investment in R&D ensures advanced wound care solutions that comply with global standards. Firms also emphasize geographic expansion into emerging markets with rising healthcare demand, while digital marketing and educational campaigns increase awareness about infection control and wound management. Offering training programs for healthcare professionals further enhances product utilization and builds long-term loyalty, solidifying competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in number of sports injuries and physical activity

- 3.2.1.2 Increasing number of surgeries/operations

- 3.2.1.3 Growing burden of pressure ulcers, diabetic foot, and other diseases

- 3.2.1.4 Rise in the awareness of advanced wound care and infection control products

- 3.2.2 Industry Pitfalls and Challenges

- 3.2.2.1 High challenges of price sensitivity of the market

- 3.2.2.2 Intense competition in the market

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion in ambulatory and homecare settings

- 3.2.3.2 Growth of e-commerce platforms for OTC wound care products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Impact of AI and generative AI on the market

- 3.10 Future market trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Medical tapes

- 5.2.1 Fabric tapes

- 5.2.2 Paper tapes

- 5.2.3 Plastic tapes

- 5.2.4 Other tapes

- 5.3 Medical bandages

- 5.3.1 Muslin bandages

- 5.3.2 Elastic bandages

- 5.3.3 Orthopedic bandages

- 5.3.4 Adhesive bandages

- 5.3.5 Hemostatic bandages

- 5.3.6 Other bandages

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Surgical wound

- 6.3 Burn injury

- 6.4 Sports injury

- 6.5 Traumatic wound

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Home care settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Johnson & Johnson

- 9.3 Smith & Nephew

- 9.4 Hartmann Group

- 9.5 Covidien (Medtronic)

- 9.6 Molnlycke Health Care

- 9.7 Paul Hartmann AG

- 9.8 Nitto Denko Corporation

- 9.9 Integra LifeSciences

- 9.10 B. Braun Melsungen AG

- 9.11 BSN medical (Essity)

- 9.12 Ansell

- 9.13 Dynarex Corporation

- 9.14 Winner Medical Group

- 9.15 Cardinal Health AG

三角绷带市场报告:趋势、预测及竞争分析(至2035年)宠物绷带市场报告:趋势、预测与竞争分析(至2035年)PCR胶带市场报告:趋势、预测和竞争分析(至2035年)

三角绷带市场报告:趋势、预测及竞争分析(至2035年)宠物绷带市场报告:趋势、预测与竞争分析(至2035年)PCR胶带市场报告:趋势、预测和竞争分析(至2035年) 神经导管、神经绷带和神经移植修復产品市场(按产品类型、材料、应用和最终用户划分),全球预测,2026-2032年

神经导管、神经绷带和神经移植修復产品市场(按产品类型、材料、应用和最终用户划分),全球预测,2026-2032年 2026年全球神经导管、神经绷带和神经移植修復产品市场报告

2026年全球神经导管、神经绷带和神经移植修復产品市场报告 全球医用胶带和绷带市场规模、份额、趋势和成长分析报告(2026-2034年)全球整形外科绷带市场规模、份额、趋势和成长分析报告(2026-2034)

全球医用胶带和绷带市场规模、份额、趋势和成长分析报告(2026-2034年)全球整形外科绷带市场规模、份额、趋势和成长分析报告(2026-2034) 氧化锌糊剂绷带市场:按类型、应用和地区划分

氧化锌糊剂绷带市场:按类型、应用和地区划分 黏合剂市场-全球产业规模、份额、趋势、机会、预测:按应用、类型、形状、地区和竞争格局划分,2021-2031年PCR胶带市场按产品类型、应用、材料和最终用户划分,全球预测(2026-2032)

黏合剂市场-全球产业规模、份额、趋势、机会、预测:按应用、类型、形状、地区和竞争格局划分,2021-2031年PCR胶带市场按产品类型、应用、材料和最终用户划分,全球预测(2026-2032)