|

市场调查报告书

商品编码

1998744

生物柴油市场机会、成长要素、产业趋势分析及2026-2035年预测Biodiesel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

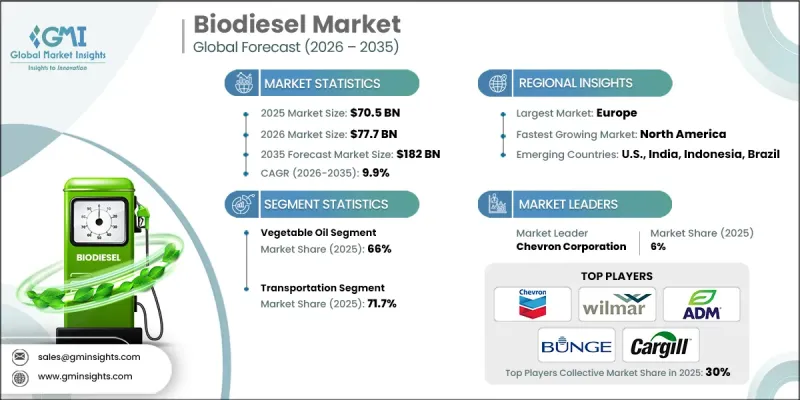

预计到 2025 年,全球生质柴油市场价值将达到 705 亿美元,并有望以 9.9% 的复合年增长率成长,到 2035 年达到 1,820 亿美元。

生物柴油市场正在扩张,这得益于各国加强对交通部燃料掺混规定的力度,以及鼓励使用更清洁替代燃料的法规结构。依赖柴油的经济体政府正在稳步提高生物柴油掺混比例要求,作为其更广泛的重型运输脱碳策略的一部分。随着设备製造商扩大使用高浓度生物柴油混合燃料的引擎的保固范围,运作生物柴油的财务和营运障碍持续降低。这些进展使得车主无需对新车进行大量资本投资即可将生质柴油纳入现有系统。实际上,生物柴油市场正日益从主要受价格优势驱动的市场转向受监管规定的主导的市场,这些规定提供了长期需求前景。这些规定也推动了燃料储存、掺混基础设施和整体供应链系统的升级,并刺激了旨在提高燃料在严苛工业环境下性能的持续研究。清晰的法律规范正在指南未来的投资,以扩大产能、原材料加工设施和供应链网路。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 705亿美元 |

| 预计金额 | 1820亿美元 |

| 复合年增长率 | 9.9% |

预计到2035年,废弃食用油市场将以11.4%的复合年增长率成长。由于废弃食用油在整个生命週期中的碳排放强度低于许多传统石油原料,因此它正迅速成为生物柴油生产中一种极具战略意义的原料。在日益增长的温室排放减排监管压力下,人们正在推广使用能够提升燃料供应链永续性指标的废弃物衍生原料。随着透明度标准的日益严格,原料采购中的可追溯性和监控系统的重要性也日益凸显。法律规范和检验机制的完善增强了人们对国际再生油原料供应网络的信心,进一步提升了废弃食用油在未来生物柴油生产中的作用。

预计到2025年,交通运输领域将占据71.7%的市场份额,并在2035年之前以9%的复合年增长率成长。由于监管政策日益严格,强制要求将可再生燃料与柴油混合,运输业仍然是生物柴油的最大消费产业。政策制定者越来越关註生物柴油,将其视为减少运输业排放的切实可行的解决方案,因为该行业目前仍然严重依赖传统的柴油引擎。由于生质柴油可以直接整合到现有的柴油基础设施中,因此无需对车辆或燃料供应系统进行大规模改造即可实现能源转型目标。这种相容性正在加速其在商用车队和大规模运输网路中的应用,同时保持营运效率。

预计到2025年,美国生质柴油市占率将达到93%,市场规模将达219亿美元。美国市场的发展得益于其健全的法规环境,该环境透过系统性的政策机制促进可再生燃料的使用,这些机制旨在降低碳排放强度并建立合规市场。此外,为了满足日益增长的永续性需求,该地区的生质柴油产业正逐步从传统的农作物衍生原料转向废弃物和残渣衍生原料。同时,美国积极向国际生质柴油市场出口,持续增强了国内生产的稳定性,从而保障了该产业的长期韧性。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监理情势

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新机会和趋势

- 数位化和物联网集成

- 进入新兴市场

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 竞争性标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 市场规模及预测:依原料划分,2022-2035年

- 植物油

- 废弃食用油(UCO)

- 动物脂肪和油脂

- 其他的

第六章 市场规模与预测:依应用领域划分,2022-2035年

- 运输

- 发电

- 其他的

第七章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 印尼

- 澳洲

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- Abellon Clean Energy

- Ag Processing

- Altret Greenfuels

- Anellotech

- Archer Daniels Midland

- Bunge

- Cargill

- Chevron Corporation

- Clariant

- FutureFuel

- G-Energetic Biofuels

- Greenergy

- Grupo Potencial

- Manuelita

- Renewable Biofuels

- TerraVia

- Total Energies

- Universal Biofuels

- Washwell Biodiesel

- Wilmar International

The Global Biodiesel Market was valued at USD 70.5 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 182 billion by 2035.

Expansion across the biodiesel market is supported by strengthening national fuel blending mandates targeting the transportation sector, along with regulatory frameworks encouraging the use of cleaner fuel alternatives. Governments across several diesel-dependent economies are steadily raising required biodiesel blend ratios as part of broader decarbonization strategies for heavy transport operations. As equipment manufacturers broaden warranty coverage for engines operating on higher biodiesel blends, the financial and operational barriers to adoption continue to decline. This dynamic allows fleet operators to integrate biodiesel into existing systems without requiring significant capital investment in new vehicles. In effect, biodiesel is increasingly shifting from a market driven by optional price advantages to one shaped by regulatory obligations with long-term demand visibility. These mandates are also stimulating upgrades across fuel storage, blending infrastructure, and supply chain systems while encouraging continued research aimed at improving fuel performance in demanding industrial environments. Clear regulatory frameworks are providing signals for future investments in production capacity, feedstock processing facilities, and supply network expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.5 Billion |

| Forecast Value | $182 Billion |

| CAGR | 9.9% |

The used cooking oil segment is projected to grow at a CAGR of 11.4% through 2035. Used cooking oil has rapidly emerged as a highly strategic feedstock within biodiesel production due to its ability to deliver lower lifecycle carbon intensity compared with many traditional oil sources. The increasing regulatory focus on reducing greenhouse gas emissions is encouraging the use of waste-derived feedstocks that can improve sustainability metrics within fuel supply chains. As transparency standards continue to strengthen, traceability and monitoring systems for feedstock sourcing have become increasingly important. Improved regulatory oversight and verification mechanisms are helping create stronger confidence in international supply networks for recycled oil feedstocks, further supporting the role of used cooking oil in future biodiesel production.

The transportation application segment accounted for 71.7% share in 2025 and is projected to grow at a CAGR of 9% through 2035. Transportation remains the largest area of biodiesel consumption due to the growing number of regulatory policies that mandate renewable fuel blending in diesel supplies. Policymakers increasingly view biodiesel as a practical solution for reducing emissions from transportation sectors that remain heavily dependent on conventional diesel engines. Since biodiesel can be integrated directly into existing diesel infrastructure, it enables energy transition goals without requiring large-scale modifications to vehicles or fuel distribution systems. This compatibility supports faster adoption across commercial fleets and large transportation networks while maintaining operational efficiency.

U.S. Biodiesel Market held 93% share in 2025 and generated USD 21.9 billion. Market development in the United States is supported by a robust regulatory environment that promotes renewable fuel usage through structured policy mechanisms and compliance markets focused on reducing carbon intensity. The regional industry is also undergoing a gradual shift away from traditional crop-based feedstocks toward waste-based and residue-derived raw materials to meet evolving sustainability expectations. In addition, strong export activity from the United States toward international biodiesel markets continues to strengthen domestic production stability and supports the long-term resilience of the sector.

Major companies operating across the Global Biodiesel Market include Wilmar International, Archer Daniels Midland, Cargill, Bunge, Chevron, Total Energies, Clariant, FutureFuel, Greenergy, Grupo Potencial, Manuelita, Universal Biofuels, Renewable Biofuels, Washwell Biodiesel, TerraVia, Ag Processing, Abellon Clean Energy, Altret Greenfuels, Anellotech, and G-Energetic Biofuels. Companies participating in the Global Biodiesel Market are strengthening their competitive position through a combination of capacity expansion, feedstock diversification, and strategic partnerships across the fuel value chain. Many producers are investing in advanced processing technologies to improve production efficiency while enabling the use of alternative feedstocks derived from waste oils and agricultural residues. Strategic collaborations with feedstock suppliers, logistics providers, and energy distributors are helping companies secure reliable supply networks and expand market access. Several firms are also focusing on developing integrated biofuel platforms that combine refining, storage, and distribution capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Feedstock trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million, Mtoe)

- 5.1 Key trends

- 5.2 Vegetable oils

- 5.3 Used cooking oil (UCO)

- 5.4 Animal fats

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, Mtoe)

- 6.1 Key trends

- 6.2 Transportation

- 6.3 Power generation

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Mtoe)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Abellon Clean Energy

- 8.2 Ag Processing

- 8.3 Altret Greenfuels

- 8.4 Anellotech

- 8.5 Archer Daniels Midland

- 8.6 Bunge

- 8.7 Cargill

- 8.8 Chevron Corporation

- 8.9 Clariant

- 8.10 FutureFuel

- 8.11 G-Energetic Biofuels

- 8.12 Greenergy

- 8.13 Grupo Potencial

- 8.14 Manuelita

- 8.15 Renewable Biofuels

- 8.16 TerraVia

- 8.17 Total Energies

- 8.18 Universal Biofuels

- 8.19 Washwell Biodiesel

- 8.20 Wilmar International

生质柴油市场:依原料、纯度等级、应用、通路和技术划分-2026-2032年全球市场预测可再生柴油市场:2026-2032年全球市场预测(依来源、生产技术、产能及终端用户产业划分)

生质柴油市场:依原料、纯度等级、应用、通路和技术划分-2026-2032年全球市场预测可再生柴油市场:2026-2032年全球市场预测(依来源、生产技术、产能及终端用户产业划分) 生质柴油市场规模、份额、趋势和预测:按原材料、应用、类型、製造技术和地区划分,2026-2034年

生质柴油市场规模、份额、趋势和预测:按原材料、应用、类型、製造技术和地区划分,2026-2034年 可再生柴油市场规模、份额和趋势分析报告:按来源、应用、地区和细分市场预测(2026-2033 年)

可再生柴油市场规模、份额和趋势分析报告:按来源、应用、地区和细分市场预测(2026-2033 年) 2026-2034年全球生物柴油催化剂市场规模、份额、趋势和成长分析报告全球生物柴油市场规模、份额、趋势和成长分析报告(2026-2034年)

2026-2034年全球生物柴油催化剂市场规模、份额、趋势和成长分析报告全球生物柴油市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球绿色柴油市场报告2026年全球可再生柴油市场报告2026年全球生质柴油市场报告生质柴油市场-2026-2031年预测

2026年全球绿色柴油市场报告2026年全球可再生柴油市场报告2026年全球生质柴油市场报告生质柴油市场-2026-2031年预测