|

市场调查报告书

商品编码

1998750

舰载通讯与控制系统市场:市场机会、成长要素、产业趋势分析及2026-2035年预测Marine Onboard Communication and Control Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

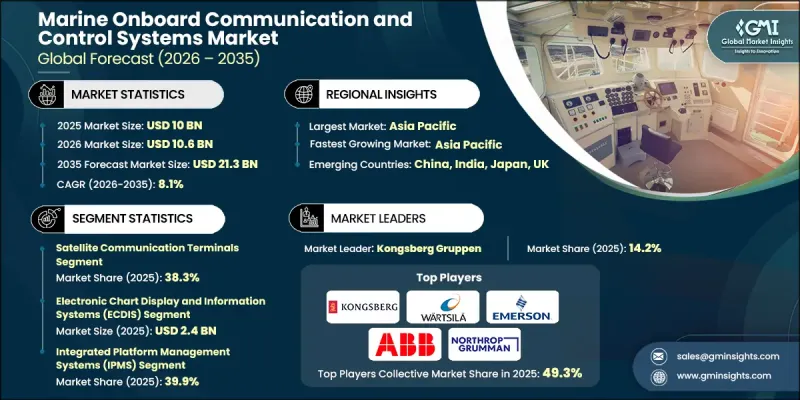

全球船舶通讯和控制系统市场预计到 2025 年将达到 100 亿美元,预计到 2035 年将以 8.1% 的复合年增长率增长至 213 亿美元。

智慧船舶自动化平台的日益普及、对可靠海事卫星通讯需求的成长以及全球商船队的持续扩张,共同推动了市场的扩张。数位导航和海事安全框架的进步,以及即时船舶监控和船队管理系统的集成,进一步促进了市场成长。航运公司越来越依赖整合导航、推进和操作控制的互联船载系统,从而提高效率、营运安全性和合规性。政府对数位海事基础设施的投资以及旨在提升船队监控、海事态态感知和运营安全性的各项倡议,也促进了先进船载通讯和控制解决方案的普及。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 100亿美元 |

| 预计金额 | 213亿美元 |

| 复合年增长率 | 8.1% |

预计到2025年,卫星通讯终端市占率将达到38.3%,这主要得益于其能够提供船舶与陆地基地之间不间断的远端通讯。这些系统支援即时航线更新、营运管理以及跨越广阔海域的船员之间的无缝通信,从而推动了市场需求的持续成长。

电子海图显示与资讯系统(ECDIS)市场预计到2025年将达到24亿美元,其在数位导航和海上安全方面发挥的关键作用是推动市场成长的主要因素。 ECDIS透过提供即时导航资料、提高情境察觉并确保符合监管要求,正在取代传统的纸质海图。 ECDIS与雷达、AIS和GNSS系统的整合进一步提升了其在商业船队中的重要性和普及性。

到2025年,北美船上通讯和控制系统市场份额将达到28.3%。这一区域成长主要得益于海军现代化、海上作业以及数位化船舶技术的广泛应用方面的大量投资。商船公司和海军当局正日益采用船上自动化、整合舰桥系统和卫星通讯解决方案,以提高营运安全性和效率。政府在海上情境察觉、海军通讯和舰队监视方面的倡议也持续推动先进船上系统的应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 扩大智慧船舶和互联船舶的应用。

- 对海上卫星通讯的需求不断增长

- 全球海运贸易与船队规模的扩张

- 对即时船舶监控系统的需求日益增长

- 国际海事组织(IMO)的规定促进了数位导航系统的应用。

- 产业潜在风险与挑战

- 老旧车队的引进和维修成本高昂

- 车载网路的网路安全风险

- 市场机会

- 自主和遥控船舶的开发

- 扩大卫星宽频在海上船舶的应用

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与开发

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴竞争对手和Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依通讯系统划分,2022-2035年

- 卫星通讯终端

- VSAT终端

- L波段终端

- 船舶无线电系统

- 甚高频无线电系统

- 中频/高频无线系统

- GMDSS设备

- 车上网路基础设施

- 路由器和交换机

- 车载宽频骨干系统

- 舰载通讯系统

- 广播/通用警报(PA/GA)系统

- 对讲系统

第六章 市场估算与预测:依导航与定位系统划分,2022-2035年

- 电子海图显示与资讯系统(ECDIS)

- 雷达系统

- X波段雷达

- S臂雷达

- 自动辨识系统(AIS)

- 全球导航卫星系统(GNSS/GPS)

- 导航资料记录器(VDR)

- 动态定位系统

第七章 市场估算与预测:依控制与自动化系统划分,2022-2035年

- 推进控制系统

- 引擎自动化系统

- 推进器控制系统

- 电源管理系统

- 整合平台管理系统(IPMS)

第八章 市场估算与预测:依监控系统应用领域划分,2022-2035年

- 火灾侦测系统

- 气体检测系统

- CCTV和车载安全系统

- 船体应力监测系统

- 状态监控系统

第九章 市场估计与预测:依平台划分,2022-2035年

- 商船

- 客船

- 货船

- 远洋船舶和特种船舶

- 防御舰

- 航空母舰

- 驱逐舰

- 护卫舰

- 克尔维特

- 潜水艇

- 两栖攻击舰

第十章 市场估价与预测:依最终用户划分,2022-2035年

- OEM

- 售后市场

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 主要企业

- ABB Group

- Kongsberg

- Wartsila

- Northrop Grumman Corporation

- Honeywell International Inc.

- 按地区分類的主要企业

- 北美洲

- Emerson Electric Co.

- L3Harris Technologies, Inc.

- Viasat, Inc.

- 亚太地区

- Furuno Electric Co., Ltd.

- Japan Radio Co., Ltd.

- Raymarine

- 欧洲

- Saab AB

- ST Engineering

- 北美洲

- 特殊玩家/干扰者

- Navico Group

The Global Marine Onboard Communication and Control Systems Market was valued at USD 10 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 21.3 billion by 2035.

The market expansion is driven by the increasing adoption of smart vessel automation platforms, rising demand for reliable maritime satellite connectivity, and the continuous growth of global commercial shipping fleets. The integration of real-time vessel monitoring and fleet management systems, alongside the advancement of digital navigation and maritime safety frameworks, is further supporting market growth. Shipping companies are increasingly relying on connected onboard systems that integrate navigation, propulsion, and operational control, enhancing efficiency, operational safety, and regulatory compliance. Government investments in digital maritime infrastructure and initiatives aimed at improving fleet monitoring, maritime domain awareness, and operational safety are also contributing to the widespread adoption of advanced onboard communication and control solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10 Billion |

| Forecast Value | $21.3 Billion |

| CAGR | 8.1% |

The satellite communication terminals segment held 38.3% share in 2025, owing to their capability to provide uninterrupted long-range communication between ships and shore-based operations. These systems support real-time route updates, operational management, and seamless crew communication across vast maritime distances, driving sustained demand.

The electronic chart display and information systems (ECDIS) segment was valued at USD 2.4 billion in 2025 and dominated the market due to its crucial role in digital navigation and maritime safety. ECDIS replaces traditional paper charts by providing real-time navigational data, enhancing situational awareness, and complying with regulatory mandates. The integration of ECDIS with radar, AIS, and GNSS systems further strengthens its relevance and adoption across commercial fleets.

North America Marine Onboard Communication and Control Systems Market accounted for 28.3% share in 2025. The region's growth is supported by substantial investment in naval modernization, offshore maritime operations, and the deployment of digital vessel technologies. Commercial shipping companies and naval authorities are increasingly implementing onboard automation, integrated bridge systems, and satellite communication solutions to enhance operational safety and efficiency. Government initiatives focused on maritime domain awareness, naval communications, and fleet monitoring continue to encourage the adoption of advanced onboard systems.

Prominent players in the Global Marine Onboard Communication and Control Systems Market include L3Harris Technologies, Inc., Raymarine, Viasat, Inc., Northrop Grumman Corporation, Furuno Electric Co., Ltd., Kongsberg, ABB Group, ST Engineering, Wartsila, Honeywell International Inc., Navico Group, Emerson Electric Co., Saab Ab, and Japan Radio Co., Ltd. Companies in the Global Marine Onboard Communication and Control Systems Market are adopting multiple strategies to solidify their presence and expand market share. They are investing in research and development to deliver advanced, integrated communication, navigation, and control solutions. Strategic collaborations with shipbuilders, naval authorities, and fleet operators enhance technology adoption and service reach. Firms are diversifying product portfolios to include satellite communication terminals, ECDIS, integrated bridge systems, and fleet management solutions, enabling comprehensive offerings. Expanding regional operations, enhancing after-sales support, and ensuring regulatory compliance are also key strategies for strengthening market footholds and building long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Communication systems trends

- 2.2.2 Navigation & positioning systems trends

- 2.2.3 Control & automation systems trends

- 2.2.4 Monitoring & surveillance systems trends

- 2.2.5 Platform trends

- 2.2.6 End-User trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of smart and connected vessels

- 3.2.1.2 Growing maritime satellite communication demand

- 3.2.1.3 Expansion of global seaborne trade and fleet size

- 3.2.1.4 Rising need for real-time vessel monitoring systems

- 3.2.1.5 IMO regulations driving digital navigation systems adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and retrofitting costs for legacy fleets

- 3.2.2.2 Cybersecurity risks in connected shipboard networks

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous and remotely operated vessel development

- 3.2.3.2 Expansion of satellite broadband for offshore vessels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Communication Systems, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Satellite communication terminals

- 5.2.1 VSAT terminals

- 5.2.2 L-band terminals

- 5.3 Marine Radio Systems

- 5.3.1 VHF radio systems

- 5.3.2 MF/HF radio systems

- 5.3.3 GMDSS equipment

- 5.4 Onboard network infrastructure

- 5.4.1 Routers & switches

- 5.4.2 Onboard broadband backbone systems

- 5.5 Internal communication systems

- 5.5.1 Public address / general alarm (PA/GA) systems

- 5.5.2 Intercom systems

Chapter 6 Market Estimates and Forecast, By Navigation & Positioning Systems, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Electronic chart display & information systems (ECDIS)

- 6.3 Radar systems

- 6.3.1 X-Band radar

- 6.3.2 S-Band radar

- 6.4 Automatic identification systems (AIS)

- 6.5 Global navigation satellite systems (GNSS/GPS)

- 6.6 Voyage data recorders (VDR)

- 6.7 Dynamic positioning systems

Chapter 7 Market Estimates and Forecast, By Control & Automation Systems, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Propulsion control systems

- 7.3 Engine automation systems

- 7.4 Thruster control systems

- 7.5 Power management systems

- 7.6 Integrated platform management systems (IPMS)

Chapter 8 Market Estimates and Forecast, By Monitoring & Surveillance Systems Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fire detection systems

- 8.3 Gas detection systems

- 8.4 CCTV & onboard security systems

- 8.5 Hull stress monitoring systems

- 8.6 Condition-based monitoring systems

Chapter 9 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial vessels

- 9.2.1 Passenger vessels

- 9.2.2 Cargo vessels

- 9.2.3 Offshore & specialized vessels

- 9.3 Defense vessels

- 9.3.1 Aircraft carriers

- 9.3.2 Destroyers

- 9.3.3 Frigates

- 9.3.4 Corvettes

- 9.3.5 Submarines

- 9.3.6 Amphibious assault ships

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 ABB Group

- 12.1.2 Kongsberg

- 12.1.3 Wartsila

- 12.1.4 Northrop Grumman Corporation

- 12.1.5 Honeywell International Inc.

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Emerson Electric Co.

- 12.2.1.2 L3Harris Technologies, Inc.

- 12.2.1.3 Viasat, Inc.

- 12.2.2 Asia Pacific

- 12.2.2.1 Furuno Electric Co., Ltd.

- 12.2.2.2 Japan Radio Co., Ltd.

- 12.2.2.3 Raymarine

- 12.2.3 Europe

- 12.2.3.1 Saab AB

- 12.2.3.2 ST Engineering

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Navico Group

指挥控制系统市场:按组件、平台和应用划分-2026-2032年全球市场预测

指挥控制系统市场:按组件、平台和应用划分-2026-2032年全球市场预测 全球防御型前置控制面板(UFC)市场(2026-2036 年)

全球防御型前置控制面板(UFC)市场(2026-2036 年) 2026年全球太空执法市场报告2026年全球船上通讯与控制系统市场报告舰载通讯与控制系统市场:2026-2032年全球市场预测(依系统类型、组件、通讯介质、安装配置、船舶类型、应用及最终用户划分)2026年全球指挥控制系统市场报告全球国防炮手控製手柄(操纵桿):2026-2036 年

2026年全球太空执法市场报告2026年全球船上通讯与控制系统市场报告舰载通讯与控制系统市场:2026-2032年全球市场预测(依系统类型、组件、通讯介质、安装配置、船舶类型、应用及最终用户划分)2026年全球指挥控制系统市场报告全球国防炮手控製手柄(操纵桿):2026-2036 年 指挥控制系统市场-全球产业规模、份额、趋势、机会、预测:按平台、解决方案、应用、地区和竞争对手划分,2021-2031年海事通讯与控制系统市场-全球产业规模、份额、趋势、机会及预测:按类型、平台、最终用户、地区及竞争格局划分,2021-2031年全球联合全局指挥控制系统市场(按组件、通讯方式、平台、应用和最终用户划分)预测(2026-2032年)

指挥控制系统市场-全球产业规模、份额、趋势、机会、预测:按平台、解决方案、应用、地区和竞争对手划分,2021-2031年海事通讯与控制系统市场-全球产业规模、份额、趋势、机会及预测:按类型、平台、最终用户、地区及竞争格局划分,2021-2031年全球联合全局指挥控制系统市场(按组件、通讯方式、平台、应用和最终用户划分)预测(2026-2032年)