|

市场调查报告书

商品编码

1998757

拦截飞弹市场商业机会、成长要素、产业趋势分析及2026-2035年预测。Interceptor Missiles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

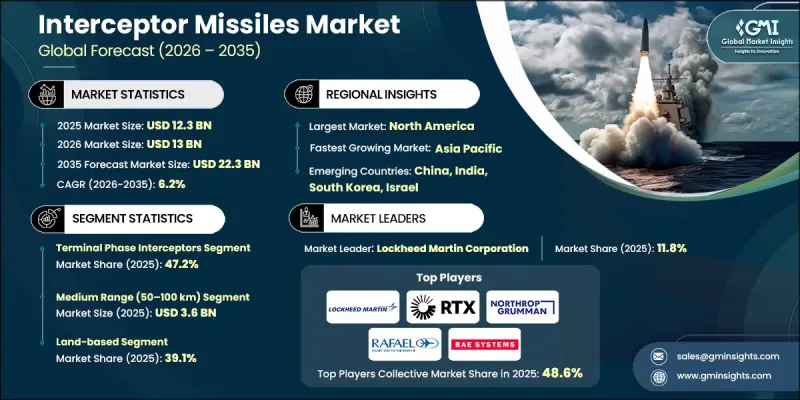

预计到 2025 年,全球拦截飞弹市场价值将达到 123 亿美元,并有望以 6.2% 的复合年增长率成长,到 2035 年达到 223 亿美元。

市场扩张的驱动力来自全球国防预算的成长、弹道飞弹和高超音速飞弹威胁的加剧以及飞弹拦截技术的不断进步。世界各国政府正优先推动防空和飞弹防御系统的现代化,以应对中远程弹道飞弹、巡航飞弹和高超音速滑翔飞行器等新兴威胁。全球防御战略正透过采用结合末段、中段和助推段拦截器的多层飞弹防御架构进行重组。人工智慧导引系统、雷达、红外线感测器和预测演算法的集成,实现了对威胁的即时跟踪,并提高了拦截成功率。对外军售(FMS)和与盟友的国防项目的扩大进一步增强了市场需求,同时,天基和机载预警系统的整合度不断提高,从而提升了探测、协调和作战效率。地缘政治紧张局势的加剧,以及对国家和盟国安全的战略投资,预计将在整个预测期内维持产业的强劲成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 123亿美元 |

| 预测金额 | 223亿美元 |

| 复合年增长率 | 6.2% |

到2025年,末段拦截器将占据47.2%的市场份额,这反映了其在应对短程和中程弹道飞弹威胁方面发挥的关键作用。末段拦截器因其快速反应能力、久经考验的可靠性以及在多层防御网络中的灵活作战柔软性而备受重视。实战演习的高成功率促使其在各国及盟国的项目中广泛部署。推进系统、导引精度和弹头效率的持续发展正在提升其作战效能,使其成为现代飞弹防御战略的核心组成部分。各国政府正日益依赖末段拦截系统来补充中段和助推段系统,从而确保建构多层防空反导体系,有效应对多种攻击手法的风险。

由于中程拦截飞弹(射程50-100公里)在成本、覆盖范围和作战柔软性方面实现了卓越的平衡,预计到2025年,其市场规模将达到36亿美元。这些系统已被广泛应用于区域飞弹防御计画中,保护本国及其盟国免受不断演变的飞弹威胁。整合到多层防御网路中,可实现与末段和中程拦截飞弹的无缝协调,从而优化响应时间和威胁消除效率。对人工智慧驱动的目标捕获、网路化感测器融合以及自动化指挥控制中心的投入不断增加,进一步提升了中程拦截飞弹的效能。对于那些寻求经济高效且技术先进的解决方案来保护关键基础设施、军事资产和都市区的国家而言,这些系统正成为理想之选。

预计到2025年,北美拦截飞弹市占率将达到41.7%,主要得益于对多层防空和飞弹防御计画的战略投资。日益紧张的地缘政治局势以及保护国家和盟国利益的需要,正推动国防预算的大幅成长。先进的研发工作重点在于人工智慧导引目标撷取、多感测器融合以及提升情境察觉,以维持技术优势。天基和网路预警系统的集成,实现了快速响应、增强协调和精准威胁评估。不断扩大的对外军售(FMS)和防务合作项目巩固了北美的区域主导地位,并为系统升级、培训项目和战略伙伴关係创造了机会。强大的国防工业基础和技术领先地位,确保北美继续保持其作为全球拦截飞弹创新中心的地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球增加飞弹防御系统方面的国防费用

- 弹道飞弹和高超音速飞弹的威胁日益加剧

- 拦截飞弹技术和导引系统的进步

- 扩大多层飞弹防御架构的应用

- 扩大对外军售和联盟防御计划

- 产业潜在风险与挑战

- 拦截飞弹系统的高昂研发和采购成本

- 对飞弹技术实施严格的监管和出口管制限制

- 市场机会

- 拦截飞弹与天基预警系统的集成

- 对老旧的防空和飞弹防御系统进行现代化改造和升级

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新经营模式

- 合规要求

- 专利和智慧财产权分析

- 价格分析(基于初步调查)

- 对过去价格趋势的分析

- 按业务类型分類的定价策略

- 贸易数据分析(基于付费资料库)

- 进出口数量和价值的变化趋势

- 主要贸易走廊和关税的影响

- 人工智慧和生成式人工智慧对市场的影响(基于初步研究)

- 利用人工智慧改造现有经营模式

- 细分市场生成式人工智慧用例和实施蓝图

- 风险、局限性和监管考量

- 生产能力和生产趋势(基于初步调查)

- 按地区和主要生产国分類的产能

- 设备运转率和扩建计划

- 国防预算分析

- 全球国防费用趋势

- 区域国防预算分配

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 主要国防现代化项目

- 预算预测(2025-2034 年)

- 对产业成长的影响

- 国防预算

- 分段式国防预算分配

- 人员

- 运作/维护

- 采购

- 研究、开发、测试和评估

- 基础设施和建筑

- 技术与创新

- 供应链韧性

- 地缘政治分析

- 劳动力分析

- 数位转型

- 併购和策略联盟的趋势

- 风险评估与管理

- 重大合约采购(2021-2024)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与开发

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係和联盟

- 技术进步

- 业务拓展与投资策略

- 数位转型计划

- 新兴竞争对手和Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依拦截阶段划分,2022-2035年

- 末级拦截飞弹

- 中段拦截飞弹

- 助推级拦截飞弹

第六章 市场估计与预测:依威胁类型划分,2022-2035年

- 弹道飞弹拦截系统

- 巡航飞弹拦截系统

- 高超音速威胁拦截系统

- 飞机/机载威胁拦截系统

第七章 市场估价与预测:依发布平台划分,2022-2035年

- 地面类型

- 海军/舰载

- 机载

- 太空安装

第八章 市场估计与预测:以续航里程划分,2022-2035年

- 短距离(小于50公里)

- 中距离(50-100公里)

- 长途(100-1000公里)

- 超长距离(超过1000公里)

第九章 市场估算与预测:依感应系统划分,2022-2035年

- 雷达导引系统

- 红外线/热探测系统

- 指挥与导引系统

- GPS导航系统

- 多感测器/混合导引系统

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- RTX Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Boeing Defense, Space &Security

- BAE Systems plc

- MBDA

- Thales Group

- 当地公司

- Rafael Advanced Defense Systems Ltd.

- Israel Aerospace Industries

- Aselsan A.

- Saab AB

- Mitsubishi Heavy Industries

- Hanwha Aerospace

- 利基公司

- Anduril Industries

- BlueHalo

- Dynetics

- Bharat Dynamics Limited

The Global Interceptor Missiles Market was valued at USD 12.3 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 22.3 billion by 2035.

Market expansion is driven by increasing global defense budgets, rising threats from ballistic and hypersonic missiles, and continuous advancements in missile interception technologies. Governments are prioritizing modernization of air and missile defense systems to counter emerging threats, including medium- and long-range ballistic missiles, cruise missiles, and hypersonic glide vehicles. The adoption of multi-layered missile defense architectures, which combine terminal, midcourse, and boost-phase interceptors, is reshaping defense strategies worldwide. Integration of AI-driven guidance, radar, and infrared sensing, and predictive algorithms allows real-time threat tracking, enhancing interception success rates. Expansion of foreign military sales and allied defense programs further strengthens market demand, while space- and airborne-based early warning systems are increasingly being integrated to improve detection, coordination, and operational efficiency. Rising geopolitical tensions, coupled with strategic investments in homeland and allied security, are expected to maintain strong industry growth throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.3 Billion |

| Forecast Value | $22.3 Billion |

| CAGR | 6.2% |

The terminal phase interceptors segment held a 47.2% share in 2025, reflecting their critical role in neutralizing short- and medium-range ballistic missile threats. Terminal interceptors are valued for rapid response capabilities, proven reliability, and operational flexibility in layered defense networks. Their deployment is widespread across national and allied programs due to high success rates in real-world exercises. Continuous development in propulsion systems, guidance accuracy, and warhead efficiency enhances their operational effectiveness, making them central to modern missile defense strategies. Governments are increasingly relying on terminal interceptors to complement midcourse and boost-phase systems, ensuring a multi-layered approach to air and missile defense that mitigates risk across multiple threat vectors.

The Medium-range interceptors (50-100 km) accounted for USD 3.6 billion in 2025, owing to their ability to balance cost, coverage, and operational flexibility. These systems are widely adopted for regional missile defense programs, providing both homeland and allied protection against evolving missile threats. Their integration into multi-tiered defense networks allows seamless coordination with terminal and midcourse interceptors, optimizing response times and threat neutralization. Increasing investment in AI-assisted targeting, networked sensor fusion, and automated command centers is further enhancing medium-range interceptor efficiency. These systems are becoming the preferred choice for countries seeking cost-effective yet technologically advanced solutions to protect critical infrastructure, military assets, and urban centers.

North America Interceptor Missiles Market held 41.7% share in 2025, driven by strategic investments in multi-layered air and missile defense programs. Rising geopolitical tensions and the need to protect both homeland and allied interests are prompting significant defense budget allocations. Advanced R&D initiatives focus on AI-guided targeting, multi-sensor fusion, and enhanced situational awareness to maintain technological superiority. Integration of space- and network-based early warning systems enables rapid response, improved coordination, and accurate threat assessment. The expansion of foreign military sales and cooperative defense programs supports regional dominance and creates opportunities for system upgrades, training programs, and strategic partnerships. Strong defense industrial bases and technological leadership ensure that North America remains a global hub for interceptor missile innovation.

Prominent players in the Global Interceptor Missiles Market include Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, Boeing Defense Space & Security, BAE Systems plc, Thales Group, MBDA, Rafael Advanced Defense Systems Ltd., Israel Aerospace Industries, Aselsan A.S., Saab AB, Mitsubishi Heavy Industries, Hanwha Aerospace, Anduril Industries, BlueHalo, and Dynetics. Companies in the Global Interceptor Missiles Market are strengthening their positions through continuous innovation in propulsion systems, guidance technologies, and sensor integration. Firms are expanding their presence in emerging markets via strategic alliances, joint ventures, and foreign military sales. Investments in AI-assisted targeting, predictive algorithms, and networked command-and-control systems are enhancing operational efficiency and effectiveness. Companies are also focusing on modular and upgradeable systems to extend product lifecycles and meet evolving threat scenarios. Marketing collaborations with governments, military exercises, and training programs help build trust and demonstrate technological superiority. By prioritizing R&D, global footprint expansion, and strategic partnerships, companies are ensuring sustained competitiveness and long-term market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Intercept phase trends

- 2.2.2 Threat type trends

- 2.2.3 Launch platform trends

- 2.2.4 Range trends

- 2.2.5 Guidance system trends

- 2.2.6 Region trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global defense spending on missile defense systems

- 3.2.1.2 Rising ballistic and hypersonic missile threats

- 3.2.1.3 Advancements in interceptor missile technologies and guidance systems

- 3.2.1.4 Growing adoption of multi-layered missile defense architectures

- 3.2.1.5 Expansion of foreign military sales and allied defense programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and procurement costs of interceptor missile systems

- 3.2.2.2 Strict regulatory and export control restrictions on missile technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of interceptor missiles with space-based and early warning systems

- 3.2.3.2 Modernization and replacement of legacy air and missile defense systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Patent and IP analysis

- 3.11 Pricing analysis (Driven by Primary Research)

- 3.11.1 Historical price trend analysis

- 3.11.2 Pricing strategy by player type

- 3.12 Trade Data Analysis (Based on Paid Databases)

- 3.12.1 Import/export volume & value trends

- 3.12.2 Key trade corridors & tariff impact

- 3.13 Impact of AI & generative AI on the market (Driven by Primary Research)

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Production capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Defense budget analysis

- 3.16 Global defense spending trends

- 3.17 Regional defense budget allocation

- 3.17.1 North America

- 3.17.2 Europe

- 3.17.3 Asia Pacific

- 3.17.4 Middle East and Africa

- 3.17.5 Latin America

- 3.18 Key defense modernization programs

- 3.19 Budget forecast (2025-2034)

- 3.19.1 Impact on industry growth

- 3.19.2 Defense budgets by country

- 3.19.3 Defense budget allocation by segment

- 3.19.3.1 Personnel

- 3.19.3.2 Operations and maintenance

- 3.19.3.3 Procurement

- 3.19.3.4 Research, development, test and evaluation

- 3.19.3.5 Infrastructure and construction

- 3.19.3.6 Technology and innovation

- 3.20 Supply chain resilience

- 3.21 Geopolitical analysis

- 3.22 Workforce analysis

- 3.23 Digital transformation

- 3.24 Mergers, acquisitions, and strategic partnerships landscape

- 3.25 Risk assessment and management

- 3.26 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Intercept Phase, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Terminal phase interceptors

- 5.3 Midcourse phase interceptors

- 5.4 Boost phase interceptors

Chapter 6 Market Estimates and Forecast, By Threat Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Ballistic missile interceptors

- 6.3 Cruise missile interceptors

- 6.4 Hypersonic threat interceptors

- 6.5 Aircraft / aerial threat interceptors

Chapter 7 Market Estimates and Forecast, By Launch Platform, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Land-based

- 7.3 Naval / ship-based

- 7.4 Airborne

- 7.5 Space-based

Chapter 8 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Short range (<50 km)

- 8.3 Medium range (50-100 km)

- 8.4 Long range (100-1,000 km)

- 8.5 Extended range (>1,000 km)

Chapter 9 Market Estimates and Forecast, By Guidance System, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Radar-guided systems

- 9.3 Infrared / heat-seeking systems

- 9.4 Command-guided systems

- 9.5 Gps-guided systems

- 9.6 Multi-sensor / hybrid guidance systems

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 RTX Corporation

- 11.1.2 Lockheed Martin Corporation

- 11.1.3 Northrop Grumman Corporation

- 11.1.4 Boeing Defense, Space & Security

- 11.1.5 BAE Systems plc

- 11.1.6 MBDA

- 11.1.7 Thales Group

- 11.2 Regional Players

- 11.2.1 Rafael Advanced Defense Systems Ltd.

- 11.2.2 Israel Aerospace Industries

- 11.2.3 Aselsan A.

- 11.2.4 Saab AB

- 11.2.5 Mitsubishi Heavy Industries

- 11.2.6 Hanwha Aerospace

- 11.3 Niche Players

- 11.3.1 Anduril Industries

- 11.3.2 BlueHalo

- 11.3.3 Dynetics

- 11.3.4 Bharat Dynamics Limited

2026年全球榴弹炮系统市场报告2026年全球防空飞弹市场报告

2026年全球榴弹炮系统市场报告2026年全球防空飞弹市场报告 防空飞弹市场:按组件、飞弹类型、推进系统、导引系统、射程、发射平台、弹头类型和最终用户划分-2026-2032年全球市场预测2026年全球拦截飞弹市场报告

防空飞弹市场:按组件、飞弹类型、推进系统、导引系统、射程、发射平台、弹头类型和最终用户划分-2026-2032年全球市场预测2026年全球拦截飞弹市场报告 全球飞弹复合材料零件市场规模、份额、趋势和成长分析报告(2026-2034年)

全球飞弹复合材料零件市场规模、份额、趋势和成长分析报告(2026-2034年) 拦截飞弹市场规模、份额和成长分析(按发射平台、类型、射程、威胁类型、技术、组件、应用、领域和地区划分)—产业预测(2026-2033 年)

拦截飞弹市场规模、份额和成长分析(按发射平台、类型、射程、威胁类型、技术、组件、应用、领域和地区划分)—产业预测(2026-2033 年) 飞弹推动的全球市场:2025年~2035年

飞弹推动的全球市场:2025年~2035年 飞弹:市场及技术的预测 (~2033年)

飞弹:市场及技术的预测 (~2033年) 飞弹推进系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测2025-2030 年全球飞弹市场预测(按部件、速度、射程、机动性、推进力和最终用途划分)

飞弹推进系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测2025-2030 年全球飞弹市场预测(按部件、速度、射程、机动性、推进力和最终用途划分)