|

市场调查报告书

商品编码

1998767

健康体检市场机会、成长要素、产业趋势分析及2026-2035年预测。Health Check-up Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

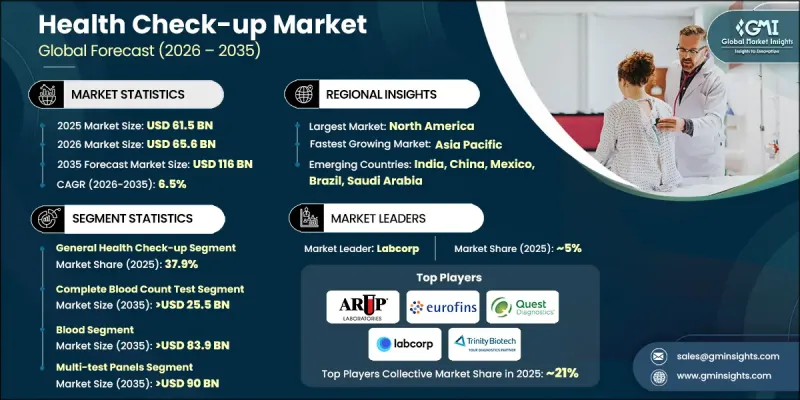

2025年全球健康体检市场价值为615亿美元,预计2035年将以6.5%的复合年增长率成长至1,160亿美元。

健康筛检市场的成长主要受以下因素驱动:国家健康筛检投入的增加、慢性病盛行率的上升以及公众对早期疾病检测重要性的认识不断提高。健康筛检是由训练有素的医疗专业人员进行的全面医学评估,旨在了解个人的整体健康状况。这些检查旨在识别潜在的健康风险、发现疾病的早期征兆,并提供预防保健建议。在许多地区,政府和医疗机构正日益推行相关政策,透过定期健康筛检来推广预防保健服务。这些措施旨在透过促进早期诊断和及时治疗,减轻晚期疾病带来的长期经济负担。此外,许多机构正在将健康筛检服务纳入员工健康计划,以支持员工的健康和生产力。这些计划建议定期进行健康筛检,以便及早发现健康风险并支持长期健康维护。所有这些因素共同推动了全球健康筛检市场的扩张。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 615亿美元 |

| 预测金额 | 1160亿美元 |

| 复合年增长率 | 6.5% |

预计2025年,定期体检及健康体检市场规模将达183亿美元,2035年将达331亿美元。人们对生活方式相关健康风险的认识不断提高,推动了定期体检的普及,旨在监测整体健康状况并及早发现潜在的健康问题。此外,经济实惠的健康套餐日益普及、数位化预约平台蓬勃发展以及个人化预防保健项目的日益流行,都将推动该市场在预测期内持续成长。

血液常规检查市场预计将以6.1%的复合年增长率成长,到2035年达到255亿美元。这项诊断测试透过分析各种血球及其浓度,在评估个体健康状况方面发挥着至关重要的作用。医疗专业人员依靠这项测试来评估生理健康的各个方面,包括有助于识别营养失衡和其他潜在健康问题的指标。此外,血球水平的波动能够提供有价值的讯息,帮助医疗专业人员识别潜在的感染疾病和发炎反应,从而实现及时的临床评估和适当的医疗管理。

美国健康体检市场预计到2025年将达到202亿美元,并在2026年至2035年间以5.6%的复合年增长率成长。人们对预防性健康管理的日益重视,持续推动着美国各地对预防性医疗保健服务的需求。慢性病发病率的上升,促使患者和医疗保健专业人员更加重视定期健康体检,以支持早期发现和持续的健康监测。此外,人口结构变化和人口老化也增加了对更频繁、更全面的健康体检的需求。诊断设备的科技进步也提高了健康体检的准确性和效率,使筛检测试更加普及,并鼓励更多人参与定期健康体检。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 对大规模健康筛检的投资正在激增。

- 疾病盛行率上升

- 人们对预防性医疗保健的认识不断提高

- 数位科技、远端医疗和居家照护服务的广泛应用。

- 产业潜在风险与挑战

- 筛检成本高昂

- 发展中地区意识水平低且基础设施不足

- 市场机会

- 人工智慧驱动的诊断工具和数位健康平台

- 促进因素

- 成长潜力分析

- 监理情势(基于初步调查)

- 北美洲

- 欧洲

- 亚太地区

- 技术趋势(基于初步调查)

- 当前技术趋势

- 新兴技术

- 救赎方案

- 差距分析(基于初步调查)

- 波特五力分析

- PESTEL 分析

- 未来市场趋势

- 人工智慧和生成式人工智慧对市场的影响

- 价值链分析

- 健康体检套餐概述(基于初步调查)

- Start-Ups场景

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- LAMEA

- 竞争定位矩阵

- 主要市场公司的竞争分析

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品类型发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 一般健康检查

- 定期健康检查

- 专业健康检查

- 预防性健康检查

第六章 市场估计与预测:依测试类型划分,2022-2035年

- 血液常规检查

- 血糖测试

- 电解质测试

- 血脂谱检测

- 荷尔蒙和维生素

- 肿瘤标记

- 肝功能检查

- 心臟生物标记

- 肾功能检查

- 骨轮廓检查

- 其他类型的测试

第七章 市场估计与预测:依检体类型划分,2022-2035年

- 血

- 尿

- 唾液

- 其他检体类型

第八章 市场估算与预测:依面板类型划分,2022-2035年

- 多重测试面板

- 单检修面板

第九章 市场估算与预测:依服务供应商,2022-2035年

- 医院检查室

- 独立检查室

- 门诊部

- 中心检查室

- 其他服务供应商

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- ARUP Laboratories

- Cerba Healthcare

- Eurofins

- Exact Sciences

- GRAIL

- INNOVA

- Labcorp

- Natera, Inc.

- OPKO

- Q2 Solutions

- Quest Diagnostics

- Sonic Healthcare

- SYNLAB

- Trinity Biotech

- UNILABS

The Global Health Check-up Market was valued at USD 61.5 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 116 billion by 2035.

Growth in the health check-up market is driven by rising investments in population health screening initiatives, increasing prevalence of chronic diseases, and greater public awareness regarding the importance of early disease detection. A health check-up refers to a comprehensive medical evaluation conducted by trained healthcare professionals to assess an individual's overall health status. These examinations are designed to identify potential health risks, detect early signs of medical conditions, and provide recommendations for preventive care. Governments and healthcare institutions across several regions are increasingly implementing policies that encourage preventive health services through regular medical examinations. Such initiatives aim to reduce the long-term economic burden associated with advanced-stage diseases by promoting early diagnosis and timely treatment. In addition, many organizations are integrating health screening services into employee wellness initiatives designed to support workforce health and improve productivity. These programs encourage regular medical assessments that help identify health risks early and support long-term wellbeing. Together, these factors are significantly contributing to the expansion of the global health check-up market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.5 Billion |

| Forecast Value | $116 Billion |

| CAGR | 6.5% |

The routine and wellness health check-up segment generated USD 18.3 billion in 2025 and is expected to reach USD 33.1 billion by 2035. Increasing awareness of lifestyle-related health risks is encouraging individuals to participate in regular medical screenings designed to monitor overall wellness and detect potential health concerns at an early stage. In addition, the growing availability of cost-effective wellness packages, the expansion of digital appointment scheduling platforms, and the rising popularity of personalized preventive health programs are supporting continued growth in this segment throughout the forecast period.

The complete blood count test segment is anticipated to grow at a CAGR of 6.1% and is projected to reach USD 25.5 billion by 2035. This diagnostic test plays an important role in evaluating an individual's health by analyzing different types of blood cells and their concentrations. Medical professionals rely on this test to assess various aspects of physiological health, including indicators that support the identification of nutritional imbalances and other underlying health conditions. In addition, variations in blood cell levels can provide valuable insights that assist healthcare providers in recognizing potential infections or inflammatory responses, enabling timely clinical evaluation and appropriate medical management.

United States Health Check-up Market was valued at USD 20.2 billion in 2025 and is projected to grow at a CAGR of 5.6% between 2026 and 2035. Increasing awareness regarding proactive health management continues to drive the demand for preventive healthcare services across the country. The rising incidence of chronic health conditions has encouraged both patients and healthcare professionals to prioritize regular medical assessments that support early detection and ongoing health monitoring. In addition, demographic changes and a growing elderly population are increasing the need for more frequent and comprehensive medical evaluations. Technological advancements in diagnostic equipment are also improving the accuracy and efficiency of health assessments, making screening procedures more accessible and encouraging broader participation in routine health examinations.

Major participants operating in the Global Health Check-up Market include Quest Diagnostics, Labcorp, Eurofins, Sonic Healthcare, SYNLAB, Cerba Healthcare, ARUP Laboratories, Exact Sciences, Natera, Inc., GRAIL, OPKO, Q2 Solutions, INNOVA, Trinity Biotech, and UNILABS. Companies operating in the Global Health Check-up Market are adopting a range of strategic initiatives to strengthen their market presence and expand service capabilities. Leading diagnostic service providers are investing in advanced laboratory technologies and digital healthcare platforms to improve the efficiency and accuracy of medical screening services. Many organizations are expanding preventive healthcare packages and personalized health assessment programs to address growing consumer demand for proactive health management. Strategic collaborations with hospitals, healthcare networks, and corporate organizations are helping companies broaden their customer base and enhance service accessibility. Additionally, firms are strengthening their laboratory infrastructure and geographic presence to support large-scale screening programs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key Market Trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Test type trends

- 2.2.4 Sample type trends

- 2.2.5 Panel type trends

- 2.2.6 Service provider trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging investments in population screening

- 3.2.1.2 Increasing prevalence of diseases

- 3.2.1.3 Rising awareness of preventive healthcare

- 3.2.1.4 Increasing adoption of digital technology/telemedicine & home-care services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with screening

- 3.2.2.2 Lack of awareness and proper infrastructure in underdeveloped regions

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven diagnostic tools and digital health platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Gap analysis (Driven by Primary Research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Impact of AI and generative AI on the market

- 3.12 Value chain analysis

- 3.13 Health check-up packages outline (Driven by primary research)

- 3.14 Start-up scenario

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key Developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 General health check-up

- 5.3 Routine and wellness health check-up

- 5.4 Specialized health check-up

- 5.5 Preventive health check-up

Chapter 6 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Complete blood count test

- 6.3 Blood glucose test

- 6.4 Electrolyte test

- 6.5 Lipid profile test

- 6.6 Hormones & vitamins

- 6.7 Tumor markers

- 6.8 Liver function test

- 6.9 Cardiac biomarkers

- 6.10 Kidney function test

- 6.11 Bone profile test

- 6.12 Other test types

Chapter 7 Market Estimates and Forecast, By Sample Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Blood

- 7.3 Urine

- 7.4 Saliva

- 7.5 Other sample types

Chapter 8 Market Estimates and Forecast, By Panel Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Multi-test panels

- 8.3 Single-test panels

Chapter 9 Market Estimates and Forecast, By Service Provider, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital-based laboratories

- 9.3 Standalone laboratories

- 9.4 Ambulatory care centers

- 9.5 Central laboratories

- 9.6 Other service providers

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ARUP Laboratories

- 11.2 Cerba Healthcare

- 11.3 Eurofins

- 11.4 Exact Sciences

- 11.5 GRAIL

- 11.6 INNOVA

- 11.7 Labcorp

- 11.8 Natera, Inc.

- 11.9 OPKO

- 11.10 Q2 Solutions

- 11.11 Quest Diagnostics

- 11.12 Sonic Healthcare

- 11.13 SYNLAB

- 11.14 Trinity Biotech

- 11.15 UNILABS