|

市场调查报告书

商品编码

1998786

无人水面航行器市场机会、成长要素、产业趋势分析及2026-2035年预测Unmanned Marine Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

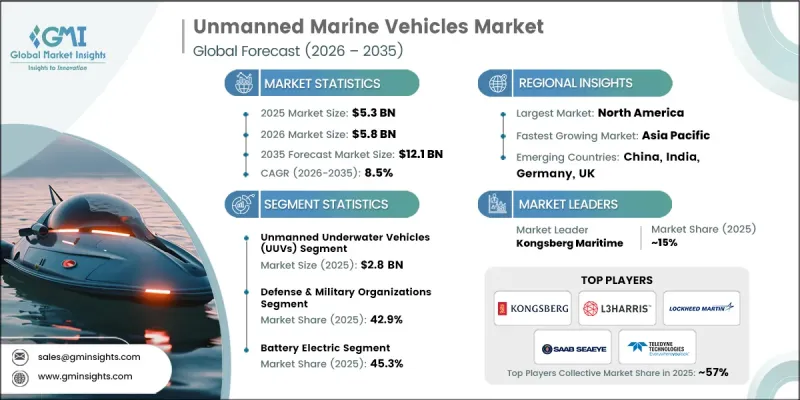

全球无人海上航行器市场预计到 2025 年将价值 53 亿美元,预计到 2035 年将以 8.5% 的复合年增长率增长至 121 亿美元。

市场扩张的驱动力来自不断增加的海军舰队现代化计划、对持续海上边界监视日益增长的需求以及不断增强的反潜作战能力。海上能源设施(尤其是深海油气作业设施)的巡检力度加大,以及离岸风力发电电场的加速开发,进一步推动了相关技术的应用。自主导航、人工智慧任务系统和安全海上通讯技术的进步,正在推动该领域的创新。数位双胞胎整合使操作人员能够即时模拟车辆性能和任务条件,从而提高运行效率。可互通的开放式架构任务系统使多厂商无人平台能够在统一的指挥结构下协同工作。这些趋势在2021年前后开始加速发展,预计将持续到2030年,从而支持灵活的车队扩张和快速的能力提升。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 53亿美元 |

| 预测金额 | 121亿美元 |

| 复合年增长率 | 8.5% |

预计到2025年,无人水下航行器(UUV)市场规模将达28亿美元。 UUV广泛应用于海军反水雷措施、反潜作战、水文测量和海上能源设施巡检等领域。其深海作业能力、在无水面能见度条件下长时间执行任务的能力以及获取高分辨率海底数据的能力,使得UUV在国防和海上能源作业中都不可或缺。

预计到2035年,燃料电池推进领域将以14.6%的复合年增长率成长。燃料电池能够延长无人水面载具的使用寿命,并减少海上维护作业期间的持续监测和频繁燃料补给需求。航运业的脱碳以及对替代推进技术投资的增加,正在加速燃料电池动力海上平台的研发和早期部署。

截至2025年,北美将占据无人海上航行器市场33.1%的份额。该地区市场成长的驱动力在于人们对海上安全、海上资产保护以及海军现代化倡议日益增长的兴趣。持续进行的情报、监视与侦察(ISR)、水雷对抗和环境监测任务正在加速国防机构、海岸防卫队和海上能源营运商对无人海上航行器的应用。先进的自主导航、基于人工智慧的任务系统和模组化无人平台正在提高作战效率,而与科技公司的合作则进一步增强了其能力。预计北美将在2035年之前保持主导地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 海军情报、监视与侦察(ISR)和水雷战现代化计画的扩展

- 海上边界监视和反潜战的需求

- 深海油气资产健康评估

- 对离岸风力发电进行检查和对海底电缆进行监测的需求

- 人工智慧驱动的自主导航系统的集成

- 产业潜在风险与挑战

- 自主海上作业监理方面的不确定性

- 长时间任务期间电池寿命的限制

- 市场机会

- 用于多单元协同任务的丛集控制

- 混合动力推进与氢动力无人水面艇

- 促进因素

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与发展(R&D)

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 业务拓展与投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估价与预测:依车辆类型划分,2022-2035年

- 无人水面载具(USV)

- 无人水下航行器(UUV)

- 一种既可用于水面航行又可用于水下航行的混合动力船。

第六章 市场估算与预测:以初级能源类型划分,2022-2035年

- 电池式电动车

- 内燃机类型

- 燃料电池类型

- 可再生能源驱动

第七章 市场估价与预测:依自动驾驶等级划分,2022-2035年

- 遥控类型

- 自主

第八章 市场估价与预测:依车辆尺寸划分,2022-2035年

- 小型(小于5公尺)

- 中型(5-15公尺)

- 大型(超过15公尺)

第九章 市场估价与预测:依最终用户划分,2022-2035年

- 国防/军事组织

- 海上能源营运商

- 私人海事服务提供者

- 民政海事局

- 研究和学术机构

- 港务局

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- Kongsberg Maritime

- Lockheed Martin Corporation

- Saab Seaeye

- L3Harris Technologies, Inc.

- Teledyne Technologies Incorporated

- 按地区分類的主要企业

- 北美洲

- Saildrone, Inc.

- Elbit Systems Ltd.

- Deep Ocean Engineering, Inc.

- 亚太地区

- Exail Technologies

- International Submarine Engineering Ltd.

- Ocean Aero

- 欧洲

- Maritime Robotics AS

- Ocius Technology Ltd

- AutoNaut Ltd

- 北美洲

- 特殊玩家/干扰者

- BlueZone Group

The Global Unmanned Marine Vehicles Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 12.1 billion by 2035.

Market expansion is fueled by increasing naval fleet modernization programs, growing demand for persistent maritime border surveillance, and heightened anti-submarine warfare capabilities. Rising offshore energy inspections, particularly in deepwater oil and gas operations, alongside accelerating offshore wind farm development, are further strengthening adoption. Advancements in autonomous navigation, AI-driven mission systems, and secure maritime communications are driving technological innovation in the sector. The integration of digital twins allows operators to simulate vehicle performance and mission conditions in real time, improving operational efficiency. Interoperable and open-architecture mission systems enable multi-vendor unmanned platforms to function within unified command structures. These trends, which gained traction around 2021, are expected to continue through 2030, supporting flexible fleet growth and rapid capability upgrades.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $12.1 Billion |

| CAGR | 8.5% |

The unmanned underwater vehicles (UUVs) segment reached USD 2.8 billion in 2025. UUVs are extensively deployed in naval mine countermeasure missions, anti-submarine warfare, hydrographic mapping, and offshore energy inspections. Their ability to operate at significant depths, perform long-endurance missions without surface visibility, and capture high-resolution seabed data makes them indispensable for both defense and offshore energy operations.

The fuel cell-powered segment is expected to grow at a CAGR of 14.6% through 2035. Fuel cells provide extended operational endurance for unmanned surface vehicles, reducing the need for frequent refueling during persistent surveillance or offshore servicing operations. Increasing investments in maritime decarbonization and alternative propulsion technologies are accelerating the development and early deployment of fuel cell-powered marine platforms.

North America Unmanned Marine Vehicles Market held a 33.1% share in 2025. Market growth in the region is driven by heightened focus on maritime security, protection of offshore assets, and naval modernization initiatives. Persistent ISR, mine countermeasure, and environmental surveillance missions are driving adoption among defense agencies, coast guards, and offshore energy operators. Advanced autonomous navigation, AI-based mission systems, and modular unmanned platforms are increasing operational efficiency, while collaborations with technology companies are further enhancing capabilities. North America is expected to maintain leadership in innovation and deployment of unmanned marine vehicles through 2035.

Prominent players operating in the Global Unmanned Marine Vehicles Market include BlueZone Group, AutoNaut Ltd, Deep Ocean Engineering, Inc., Elbit Systems Ltd., Exail Technologies, International Submarine Engineering Ltd., Kongsberg Maritime, L3Harris Technologies, Inc., Lockheed Martin Corporation, Maritime Robotics AS, Ocean Aero, Ocius Technology Ltd, Saab Seaeye, Saildrone, Inc., and Teledyne Technologies Incorporated. Companies in the Global Unmanned Marine Vehicles Market are pursuing multiple strategies to consolidate their market position and enhance competitiveness. They are investing heavily in R&D to develop AI-enabled autonomous systems, fuel cell propulsion platforms, and next-generation underwater and surface vehicles. Strategic partnerships with defense organizations, offshore energy operators, and technology firms enable integration of cutting-edge unmanned solutions into operational fleets. Companies are also expanding production capacity, establishing regional service hubs, and offering training programs to improve customer support. Modular design, open-architecture mission systems, and digital twin integration allow rapid upgrades and fleet interoperability, strengthening adoption in defense, research, and commercial sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vehicle type trends

- 2.2.2 Primary energy source trends

- 2.2.3 Autonomy level trends

- 2.2.4 Vehicle size trends

- 2.2.5 End user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising naval ISR and mine countermeasure modernization programs

- 3.2.1.2 Maritime border surveillance and anti-submarine warfare needs

- 3.2.1.3 Deepwater oil & gas asset integrity inspections

- 3.2.1.4 Offshore wind farm inspection and subsea cable monitoring demand

- 3.2.1.5 Integration of AI-enabled autonomous navigation systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory uncertainty for autonomous maritime operations

- 3.2.2.2 Limited battery endurance for long-duration missions

- 3.2.3 Market opportunities

- 3.2.3.1 Swarm-enabled multi-vehicle coordinated missions

- 3.2.3.2 Hybrid propulsion and hydrogen-powered USVs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Unmanned surface vehicles (USVs)

- 5.3 Unmanned underwater vehicles (UUVs)

- 5.4 Hybrid surface-underwater vehicles

Chapter 6 Market Estimates and Forecast, By Primary Energy Source, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Battery electric

- 6.3 Combustion-based

- 6.4 Fuel cell-based

- 6.5 Renewable-driven

Chapter 7 Market Estimates and Forecast, By Autonomy Level, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Remotely operated

- 7.3 Autonomous

Chapter 8 Market Estimates and Forecast, By Vehicle Size, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Small (< 5 meters)

- 8.3 Medium (5-15 meters)

- 8.4 Large (> 15 meters)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Defense & military organizations

- 9.3 Offshore energy operators

- 9.4 Commercial marine service providers

- 9.5 Civil government maritime authorities

- 9.6 Research & academic institutions

- 9.7 Port & harbor authorities

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Kongsberg Maritime

- 11.1.2 Lockheed Martin Corporation

- 11.1.3 Saab Seaeye

- 11.1.4 L3Harris Technologies, Inc.

- 11.1.5 Teledyne Technologies Incorporated

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Saildrone, Inc.

- 11.2.1.2 Elbit Systems Ltd.

- 11.2.1.3 Deep Ocean Engineering, Inc.

- 11.2.2 Asia Pacific

- 11.2.2.1 Exail Technologies

- 11.2.2.2 International Submarine Engineering Ltd.

- 11.2.2.3 Ocean Aero

- 11.2.3 Europe

- 11.2.3.1 Maritime Robotics AS

- 11.2.3.2 Ocius Technology Ltd

- 11.2.3.3 AutoNaut Ltd

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 BlueZone Group