|

市场调查报告书

商品编码

1998792

鹰嘴豆市场商机、成长要素、产业趋势分析及2026-2035年预测。Chickpeas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

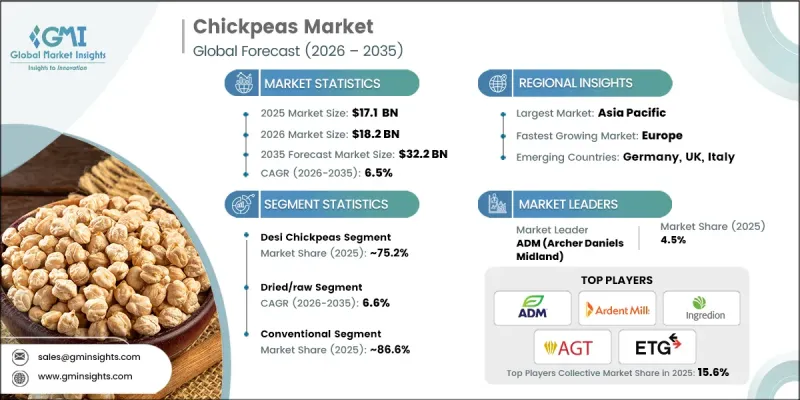

预计到 2025 年,全球鹰嘴豆市场价值将达到 171 亿美元,并预计以 6.5% 的复合年增长率成长,到 2035 年达到 322 亿美元。

鹰嘴豆(也称为鹰嘴豆)因其高营养价值而广为人知,富含蛋白质、纤维、维生素和必需矿物质。全球对植物性饮食日益增长的兴趣,以及人们对鹰嘴豆健康益处的认识不断提高,正在推动市场成长。消费者追求高蛋白、无麸质和非基因改造食品,这提升了鹰嘴豆作为一种天然且用途广泛的食材的需求。素食、纯素食和弹性素食饮食方式的日益普及,进一步增加了各种形式的鹰嘴豆消费量。加工食品、零食和其他植物来源产品对鹰嘴豆的需求也在推动市场成长,使鹰嘴豆成为现代饮食的重要组成部分。永续的农业实践以及对仓储和加工基础设施的投资,有助于确保鹰嘴豆的品质和供应稳定性,并促进该行业的长期发展。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 171亿美元 |

| 预计金额 | 322亿美元 |

| 复合年增长率 | 6.5% |

预计到2025年,干鹰嘴豆和鲜鹰嘴豆市占率将达到70.5%,并在2026年至2035年间以6.6%的复合年增长率成长。这一细分市场的成长得益于消费者对加工最少、天然食材的偏好。干鹰嘴豆用途广泛,让消费者在家烹调时也能轻鬆摄取富含蛋白质和膳食纤维的食物。为了确保产品品质和供应的稳定性,农民和供应商正越来越多地采用永续的耕作方式,并建造现代化的加工和仓储设施。

预计到2025年,传统鹰嘴豆市占率将达到86.6%,并在2035年之前以6.6%的复合年增长率成长。其成本绩效且易于获取,使其成为寻求价格亲民产品的消费者的首选。传统鹰嘴豆广泛用于加工食品,例如麵粉、零食和即食食品。同时,随着消费者对健康、永续性和有机认证产品的关注度不断提高,有机鹰嘴豆也日益受到重视。传统鹰嘴豆和有机鹰嘴豆对于满足市场多样化的需求至关重要。

预计到2025年,北美鹰嘴豆市占率将达到7.1%。该地区鹰嘴豆市场正蓬勃发展,这主要得益于人们对植物来源营养的日益关注,以及对鹰嘴豆零食、无麸质产品和健康替代食品需求的增长。成熟的食品加工和零售业为市场扩张提供了支持,而产品创新和不断拓展的分销网络也进一步巩固了市场地位。素食主义和纯素食主义的饮食趋势,以及便利营养产品的普及,正在进一步推动美国和加拿大市场的渗透。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 卡布里鹰嘴豆

- 印度鹰嘴豆

第六章 市场估计与预测:依类型划分,2022-2035年

- 干/生

- 小麦粉

- 即食产品

第七章 市场估计与预测:依类型划分,2022-2035年

- 传统的

- 有机的

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 饮食

- 家常菜和传统菜餚

- 调理食品/已调理食品

- 麵包糖果甜点

- 零食和糖果甜点

- 植物性蛋白质产品

- 其他的

- 动物饲料

- 营养补充品

- 工业的

第九章 市场估价与预测:依通路划分,2022-2035年

- 批发和直销

- 超级市场和大卖场

- 专卖店

- 线上零售

- 便利商店

第十章 市场估价与预测:依最终用户划分,2022-2035年

- 食品加工/製造商

- 一般家庭和零售消费者

- 餐厅经营者

- 机构买家

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十二章:公司简介

- ADM(Archer Daniels Midland)

- Agrocorp Processing Australia

- AGT Food &Ingredients Inc.

- Ardent Mills

- Avena Foods

- Bean Growers Australia

- Diefenbaker Spice &Pulse(DSP)

- ETG Group

- Grain Processing Corporation(GPC)

- Ingredion Incorporated

- MT Royal

- Nutriati Inc.

- Superior Pulses

- Vad Industries

The Global Chickpeas Market was valued at USD 17.1 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 32.2 billion by 2035.

Chickpeas, also known as garbanzo beans, are widely recognized for their nutritional profile, offering protein, fiber, vitamins, and essential minerals. The increasing global focus on plant-based diets, along with rising awareness of the health benefits of chickpeas, is driving market growth. Consumers are seeking protein-rich, gluten-free, and non-GMO foods, boosting demand for chickpeas as a natural, versatile ingredient. Vegetarian, vegan, and flexitarian diets have gained significant traction, further increasing the consumption of chickpeas in various forms. The market growth is also fueled by the demand for chickpeas in processed foods, snacks, and other plant-based products, making them an integral part of modern dietary patterns. Sustainable farming practices and investment in storage and processing infrastructure are helping maintain quality, availability, and long-term growth of the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.1 Billion |

| Forecast Value | $32.2 Billion |

| CAGR | 6.5% |

The dried and raw chickpeas segment held a 70.5% share in 2025 and is expected to grow at a CAGR of 6.6% between 2026 and 2035. This segment benefits from consumer preference for minimally processed, natural ingredients. Dried chickpeas are versatile and allow consumers to cook meals at home while maintaining a protein-rich and fiber-filled diet. Farmers and suppliers are increasingly adopting sustainable cultivation methods and building modern processing and storage facilities to ensure consistent quality and supply.

The conventional chickpeas segment accounted for 86.6% share in 2025 and is projected to grow at a CAGR of 6.6% through 2035. Their cost-effectiveness and widespread availability make them the preferred choice for consumers seeking budget-friendly options. Conventional chickpeas are commonly used in processed foods such as flours, snacks, and ready-to-eat meals. Meanwhile, organic chickpeas are gaining traction as consumer interest in health-conscious, sustainable, and certified organic products grows. Both conventional and organic segments are essential to meet the diverse needs of the market.

North America Chickpeas Market accounted for 7.1% share in 2025. The region is experiencing growth driven by rising awareness of plant-based nutrition, increasing demand for chickpea-based snacks, gluten-free products, and healthy food alternatives. The established food processing and retail sectors support market expansion, while product innovation and distribution network growth continue to strengthen market presence. Vegan and vegetarian dietary trends, along with convenient, nutritious offerings, are further bolstering market adoption across the U.S. and Canada.

Key players operating in the Global Chickpeas Market include Agrocorp Processing Australia, Bean Growers Australia, Diefenbaker Spice & Pulse (DSP), MT Royal, ETG Group, ADM (Archer Daniels Midland), Ingredion Incorporated, Vad Industries, Superior Pulses, Ardent Mills, Avena Foods, Nutriati Inc., and AGT Food & Ingredients Inc. Companies in the Global Chickpeas Market are adopting strategies to strengthen their position by investing in modern processing and storage facilities, expanding distribution networks, and improving supply chain efficiency. Product innovation, including ready-to-cook, ready-to-eat, and fortified chickpea offerings, helps cater to evolving consumer preferences. Firms are emphasizing sustainable and certified farming practices to appeal to environmentally conscious buyers. Strategic partnerships with retailers, food service providers, and international distributors allow for broader market reach and recurring demand. Companies are also focusing on marketing campaigns highlighting health benefits, protein content, and dietary versatility to reinforce brand presence and encourage adoption among plant-based consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Form

- 2.2.3 Nature

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.2.6 End user

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Kabuli chickpeas

- 5.3 Desi chickpeas

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dried/raw

- 6.3 Flour & powder

- 6.4 Ready-to-eat products

Chapter 7 Market Estimates and Forecast, By Nature, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Organic

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Home cooking/traditional meals

- 8.2.2 Ready meals & prepared foods

- 8.2.3 Bakery & confectionery

- 8.2.4 Snacks & savories

- 8.2.5 Plant-based protein products

- 8.2.6 Others

- 8.3 Animal feed

- 8.4 Nutraceuticals

- 8.5 Industrial

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Wholesale & direct sales

- 9.3 Supermarkets & hypermarkets

- 9.4 Specialty stores

- 9.5 Online retail

- 9.6 Convenience stores

Chapter 10 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Food processors & manufacturers

- 10.3 Household/retail consumers

- 10.4 Food service operators

- 10.5 Institutional buyers

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 ADM (Archer Daniels Midland)

- 12.2 Agrocorp Processing Australia

- 12.3 AGT Food & Ingredients Inc.

- 12.4 Ardent Mills

- 12.5 Avena Foods

- 12.6 Bean Growers Australia

- 12.7 Diefenbaker Spice & Pulse (DSP)

- 12.8 ETG Group

- 12.9 Grain Processing Corporation (GPC)

- 12.10 Ingredion Incorporated

- 12.11 MT Royal

- 12.12 Nutriati Inc.

- 12.13 Superior Pulses

- 12.14 Vad Industries