|

市场调查报告书

商品编码

1998796

2026 年至 2035 年超豪华家庭自动化市场的商业机会、成长要素、产业趋势与预测。Ultra-Luxury Home Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

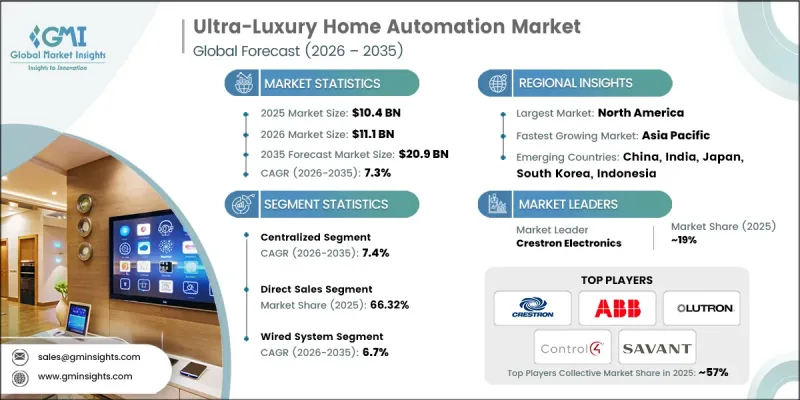

全球超豪华家庭自动化市场预计到 2025 年将价值 104 亿美元,预计到 2035 年将以 7.3% 的复合年增长率增长至 209 亿美元。

该行业的成长源于富裕住宅对高度个人化、智慧化居住环境日益增长的需求。住宅业主越来越倾向于透过客製化的自动化平台,对照明、温控、安防系统和多媒体基础设施等关键住宅功能进行整合控制。客製化的自动化解决方案使住宅能够根据自身的生活节奏、喜好和生活方式需求来配置生活空间。此外,最新的自动化技术能够将多个智慧型装置整合到一个集中式的管理介面中,使复杂的住宅管理更加便捷有效率。超豪华住宅正在演变为精心打造的数位生态系统,科技提升了舒适度、专属感和易用性。业主期望自动化平台能够与建筑风格、空间布局和日常使用习惯相协调。基于场景的自动化透过智慧编程协调多种功能,进一步提升了居住体验。豪华住宅开发案正越来越多地融入先进的自动化功能,以提供彰显个人身分和地位的精緻生活体验。为了满足这些不断变化的期望,超豪华住宅自动化市场的供应商正致力于提供复杂的硬体基础设施和智慧软体平台组合,旨在满足客户最具体的需求。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 104亿美元 |

| 预计金额 | 209亿美元 |

| 复合年增长率 | 7.3% |

预计到2025年,集中式自动化市场规模将达到50亿美元,并在2026年至2035年间以7.4%的复合年增长率成长。该细分市场在超豪华智慧住宅市场中占据主导地位,因为它透过统一的控制框架实现了全面的系统整合。集中式平台使住宅能够透过单一介面高效管理多个住宅系统,从而提高大型住宅的营运效率。富裕的住宅偏好这种架构,因为它确保了互联技术之间的可靠通信,并降低了系统不相容的可能性。此外,先进的控制系统支援开发高度客製化的自动化程序和日程安排功能,从而打造个人化的住宅体验。

预计到2025年,有线技术市占率将达到63.22%,并在2035年之前以6.7%的复合年增长率成长。该系统凭藉其可靠的性能和稳定的数据传输能力,持续引领市场。实体基础设施确保了在庞大的住宅环境中实现持续稳定的连接,而设备间不间断的通讯至关重要。高频宽容量支援先进的自动化流程,避免干扰或连线波动。高端住宅住宅往往更倾向于选择有线安装,因为其可靠性高、网路安全潜力强,且系统长期稳定。多种住宅技术的深度整合进一步提升了集中式自动化框架的效率和反应速度。

美国超豪华智慧住宅市场预计到2025年将达到33亿美元,并在2026年至2035年间以7.4%的复合年增长率成长。推动美国市场需求成长的主要因素是越来越多的富裕住宅投资于技术先进的住宅环境。新建的豪华住宅项目越来越多地采用完全客製化的自动化基础设施,以提升生活水准和营运效率。消费者对先进数位科技的认知不断提高,也加速了智慧住宅系统在豪华住宅开发案的应用。对豪华房地产的持续投资也促进了超豪华住宅领域对先进自动化平台的稳定需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 个人化智慧生活体验的需求日益增长

- 人工智慧和物联网等先进技术的融合

- 豪华房地产开发成长

- 陷阱与挑战

- 高阶系统和较高的初始安装成本

- 资料安全和隐私问题

- 机会

- 与高端房地产开发商和建筑师建立合作关係

- 生物识别技术与下一代安全技术的融合

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 照明设备

- 壁挂式模组/智慧灯泡

- 智慧开关

- 智慧插头

- 其他(智慧型调光器等)

- 智慧安防设备

- 人体存在/接近感测器

- 门窗感应器

- 警报

- 智慧无线门铃

- 智慧门锁

- 其他(监视器等)

- 娱乐装置

- 扬声器/音讯分配

- 影像布线

- 其他(例如虚拟个人助理)

- 保护感测器

- 漏水和火灾感测器

- 紫外线感测器

- 其他(湿度感测器等)

- 其他的

第六章 市场估算与预测:依自动化类型划分,2022-2035年

- 去中心化

- 集中

- 杂交种

第七章 市场估计与预测:依技术划分,2022-2035年

- 有线系统

- 无线系统

第八章 市场估算与预测:依通路划分,2022-2035年

- 直销

- 间接销售

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十章:公司简介

- ABB

- Aurum HomeTech

- Bang & Olufsen

- Control4

- Crestron Electronics

- Ecobee

- Heyo Smart

- Honeywell International

- Johnson Controls

- Legrand

- Lutron Electronics

- Savant Systems

- Schneider Electric

- Siemens

- Vivint

The Global Ultra-Luxury Home Automation Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 20.9 billion by 2035.

Growth in the industry is driven by the rising preference among affluent homeowners for highly personalized smart living environments. Property owners in the premium residential segment increasingly seek integrated control over essential home functions, including lighting, climate management, safety systems, and multimedia infrastructure through customized automation platforms. Tailored automation solutions allow homeowners to configure their living spaces according to personal routines, preferences, and lifestyle requirements. In addition, modern automation technologies enable the integration of multiple smart devices into a single centralized management interface, making complex residential operations more convenient and efficient. Ultra-luxury residences are evolving toward highly curated digital ecosystems where technology enhances comfort, exclusivity, and ease of use. Property owners expect automation platforms that align with architectural design, spatial layout, and daily usage behavior. Scenario-based automation further enhances living experiences by coordinating multiple functions through intelligent programming. Premium residential developments increasingly incorporate advanced automation capabilities to deliver a refined lifestyle experience that reflects personal identity and status. To address these evolving expectations, providers in the ultra-luxury home automation market are focusing on delivering sophisticated combinations of hardware infrastructure and intelligent software platforms designed to meet the highly specific requirements of their clientele.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 7.3% |

The centralized automation segment generated USD 5 billion in 2025 and is forecast to grow at a CAGR of 7.4% between 2026 and 2035. This segment holds a dominant position in the ultra-luxury home automation market because it enables comprehensive system coordination through a unified control framework. Centralized platforms allow homeowners to efficiently oversee multiple residential systems from a single interface, improving operational efficiency across large properties. Affluent homeowners prefer this architecture because it ensures reliable communication between connected technologies and reduces the likelihood of system incompatibility. Advanced control systems also enable the development of highly customized automation routines and scheduling capabilities that support personalized residential experiences.

The wired technology segment accounted for 63.22% share in 2025 and is anticipated to grow at a CAGR of 6.7% through 2035. This system type continues to lead the market because of its dependable performance and stable data transmission capabilities. Physical infrastructure ensures consistent connectivity across extensive residential environments where uninterrupted communication between devices is essential. High bandwidth capacity supports sophisticated automation processes without interference or connectivity fluctuations. Homeowners in the luxury residential segment often favor wired installations due to their reliability, enhanced cybersecurity potential, and long-term system stability. Strong integration across multiple residential technologies further improves the efficiency and responsiveness of centralized automation frameworks.

United States Ultra-Luxury Home Automation Market was valued at USD 3.3 billion in 2025 and is expected to grow at a CAGR of 7.4% from 2026 to 2035. Demand in the country is supported by a growing population of affluent homeowners investing in technologically advanced residential environments. Newly developed luxury properties increasingly incorporate fully customized automation infrastructure to enhance living standards and operational efficiency. Rising consumer awareness of advanced digital technologies is accelerating the adoption of intelligent residential systems across premium housing developments. Continued investment in high-end real estate is also contributing to consistent demand for advanced automation platforms within the ultra-luxury residential segment.

Prominent participants operating in the Global Ultra-Luxury Home Automation Market include Crestron Electronics, Savant Systems, Control4, Lutron Electronics, Legrand, Schneider Electric, ABB, Siemens, Johnson Controls, Honeywell International, Vivint, Ecobee, Bang & Olufsen, Aurum HomeTech, and Heyo Smart. Companies operating in the Ultra-Luxury Home Automation Market are strengthening their market presence through a combination of technology innovation, strategic collaborations, and premium service offerings. Leading players are investing in advanced software platforms that enable seamless integration between multiple home automation technologies while maintaining high system reliability. Firms are also developing customized automation ecosystems designed specifically for luxury residential environments, allowing them to address highly specialized homeowner requirements. Partnerships with luxury real estate developers, architects, and interior designers are becoming an important strategy to secure early involvement in high-end construction projects.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Automation Type

- 2.2.4 Technology Type

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for personalized smart living experiences

- 3.2.1.2 Integration of advanced technologies such as AI and IoT

- 3.2.1.3 Growth in luxury real estate development

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High upfront costs of premium systems and installation

- 3.2.2.2 Data security and privacy concerns

- 3.2.3 Opportunities

- 3.2.3.1 Partnerships with luxury real estate developers and architects

- 3.2.3.2 Integration of biometric and next-gen security technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Lighting devices

- 5.2.1 In-wall modules/ smart bulbs

- 5.2.2 Smart switches

- 5.2.3 Smart plugs

- 5.2.4 Others (smart dimmer etc.)

- 5.3 Smart security devices

- 5.3.1 Motion/arrival sensor

- 5.3.2 Door/window sensor

- 5.3.3 Alarms

- 5.3.4 Smart wireless bells

- 5.3.5 Smart door locks

- 5.3.6 Others (security cameras etc.)

- 5.4 Entertainment devices

- 5.4.1 Speakers/ audio distribution

- 5.4.2 Video distribution

- 5.4.3 Others (virtual personal assistant etc.)

- 5.5 Protection sensors

- 5.5.1 Flood/fire sensors

- 5.5.2 UV sensors

- 5.5.3 Others (humidity sensors etc.)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Automation Type, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Distributed

- 6.3 Centralized

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Wired system

- 7.3 Wireless system

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Aurum HomeTech

- 10.3 Bang & Olufsen

- 10.4 Control4

- 10.5 Crestron Electronics

- 10.6 Ecobee

- 10.7 Heyo Smart

- 10.8 Honeywell International

- 10.9 Johnson Controls

- 10.10 Legrand

- 10.11 Lutron Electronics

- 10.12 Savant Systems

- 10.13 Schneider Electric

- 10.14 Siemens

- 10.15 Vivint

智慧家居系统市场:依安装类型、组件、连接方式、最终用户、销售管道和应用划分-2026-2032年全球市场预测

智慧家居系统市场:依安装类型、组件、连接方式、最终用户、销售管道和应用划分-2026-2032年全球市场预测 汽车个人化和使用者体验平台市场预测:至 2034 年—按组件、车辆类型、应用和区域分類的全球分析

汽车个人化和使用者体验平台市场预测:至 2034 年—按组件、车辆类型、应用和区域分類的全球分析 2026年全球智慧家庭市场报告

2026年全球智慧家庭市场报告 家庭自动化市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

家庭自动化市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 家庭自动化市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型及最终用户划分全球智慧家居系统市场规模、份额、趋势及成长分析报告(2026-2034年)

家庭自动化市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型及最终用户划分全球智慧家居系统市场规模、份额、趋势及成长分析报告(2026-2034年) 日本智慧家居系统市场规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年日本智慧家庭市场规模、份额、趋势和预测:按类型、技术、最终用户和地区划分,2026-2034年

日本智慧家居系统市场规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年日本智慧家庭市场规模、份额、趋势和预测:按类型、技术、最终用户和地区划分,2026-2034年 全球智慧家庭市场(至 2035 年):按产品类型、技术类型、应用类型、最终用户类型、地区、产业趋势和预测2026年全球家庭自动化与控制系统市场报告

全球智慧家庭市场(至 2035 年):按产品类型、技术类型、应用类型、最终用户类型、地区、产业趋势和预测2026年全球家庭自动化与控制系统市场报告