|

市场调查报告书

商品编码

1998802

动物保健市场:商业机会、成长要素、产业趋势分析及2026-2035年预测Animal Healthcare Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025年全球动物保健市场价值为2,208亿美元,预计2035年将以5.9%的复合年增长率成长至3,994亿美元。

市场成长的驱动力在于动物疾病发生率的上升,包括需要高级兽医护理的慢性病和感染疾病。农业环境、住宅环境和城市生态系统中人与动物接触的增加也凸显了有效动物健康管理的重要性。动物保健市场涵盖了广泛的全球产业,专注于预防、诊断和治疗影响伴侣动物和牲畜健康的疾病。这包括动物用药品、疫苗、诊断解决方案、药用饲料添加剂、医疗设备和一次性用品,旨在保护动物健康并支持畜牧业生产力。此外,加强疾病控制有助于降低通用感染疾病的风险,进而保护公众健康。该行业正逐步从一般治疗方法转向更先进的预防性和针对性的医疗保健解决方案。虽然伴侣动物生技药品和特化单株抗体的应用日益增多,但畜牧业医疗保健也越来越依赖尖端疫苗技术和基于畜群的疾病预防策略。此外,随着诊断技术和基于生物标记的检测手段日益普及,个人化兽医学正受到越来越多的关注,使兽医能够根据动物的物种特征和具体健康状况量身定制治疗方案。同时,以患者为中心的治疗方案的开发也拓展了传统药物治疗以外的治疗可能性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 2208亿美元 |

| 预测金额 | 3994亿美元 |

| 复合年增长率 | 5.9% |

预计到2025年,兽医服务市占率将达到74.5%,并在2035年之前以6%的复合年增长率成长。这一强劲的市场趋势主要受可支配收入成长和对专业兽医护理需求增加的驱动。人们对动物健康和福利的日益关注,促使更多人为宠物寻求全面的兽医服务。此外,兽医技术的进步也扩大了该领域的服务范围。更多宠物专属服务变得更加便捷,从而提高了兽医机构的使用率。现代医疗保健技术的整合以及服务交付的改进,正在增强整个兽医服务行业的整体实力,并支持市场的持续扩张。

预计到2025年,伴侣动物市场规模将达到1,331亿美元。该市场包含伴侣动物群体中的多个子群体。全球饲养宠物作为伴侣的趋势日益增长,是推动该市场成长的主要动力。如今,世界各地许多家庭都饲养宠物作为伴侣,这导致对兽医护理、医疗产品和专业医疗保健服务的需求不断增加。宠物健康和保健支出的增加也推动了创新动物保健解决方案的开发和应用。此外,新兴经济体可支配收入的成长使更多宠物饲主能够投资于先进的医疗保健产品和兽医服务,从而进一步促进了伴侣动物市场的扩张。

预计到2025年,北美动物保健市占率将达到38.5%。该地区凭藉其完善的兽医基础设施和先进的动物医疗解决方案的广泛应用,保持着主导地位。创新疗法、疫苗和寄生虫控制产品在伴侣动物和家畜中的积极应用,推动了该地区市场的成长。北美也受益于先进诊断技术和精准兽医方法的早期应用。拥有强大研发能力的关键产业参与者的存在,进一步加速了该地区的创新。人们对预防性动物保健意识的不断提高,以及对影响动物的慢性疾病和通用感染疾病日益增长的关注,持续推动对先进兽医服务和优质动物保健产品的需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 宠物数量增加

- 政府和民众加大对动物照护的支持度

- 对线上动物用药品局的需求日益增长

- 动物医疗保健支出增加

- 产业潜在风险与挑战

- 动物用药品高成本

- 遍远地区的通行限制

- 市场机会

- 远端医疗和远距兽医咨询的扩展

- 扩大以预防和保健为重点的动物保健解决方案的普及应用。

- 促进因素

- 成长潜力分析

- 技术趋势(基于初步调查)

- 当前技术趋势

- 新兴技术

- 监理情势(基于初步调查)

- 还款方案(基于初步调查)

- 动物用药品产业创业投资趋势

- 动物用药品产业的经济影响

- 消费行为趋势(基于初步调查)

- 未来市场趋势(基于初步研究)

- 人工智慧和生成式人工智慧对市场的影响

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 製药

- 种类

- 製药

- 杀虫剂

- 消炎(药)

- 抗感染药物

- 皮质类固醇

- 镇静剂

- 循环系统药物

- 消化器官系统药物

- 其他药物

- 疫苗

- 减毒活病毒疫苗(MLV)

- 灭活疫苗

- 其他疫苗

- 药用饲料添加剂

- 抗生素

- 维他命

- 胺基酸

- 酵素

- 抗氧化剂

- 益生元和益生菌

- 矿物

- 其他药用饲料添加剂

- 製药

- 适应症

- 皮肤科

- 循环系统疾病

- 消化系统疾病

- 呼吸系统疾病

- 其他迹象

- 销售管道

- 兽药

- 电子商务

- 零售药房

- 种类

- 医疗设备

- 兽医诊断设备

- 麻醉设备

- 病患监测设备

- 兽用外科器械

- 动物用品

- 其他医疗设备

- 兽医医疗服务

第六章 市场估计与预测:依动物种类划分,2022-2035年

- 伴侣动物

- 狗

- 猫

- 马

- 其他伴侣动物

- 家畜

- 家禽

- 猪

- 牛

- 鱼

- 其他牲畜

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 海湾合作委员会国家

- 以色列

第八章:公司简介

- B. Braun Vet Care(B Braun Melsungen)

- Boehringer Ingelheim

- Ceva Sante Animale

- Dechra Pharmaceuticals

- Elanco Animal Health

- Endovac Animal Health

- HIPRA

- IDEXX Laboratories

- Merck

- Medtronic

- Neogen

- Sklar Surgical Instruments

- Symrise

- Vetoquinol

- Virbac

- Zoetis

- Phibro Animal Health

- Indian Immunologicals

- Kyoritsu Seiyaku

- Ourofino Saude Animal

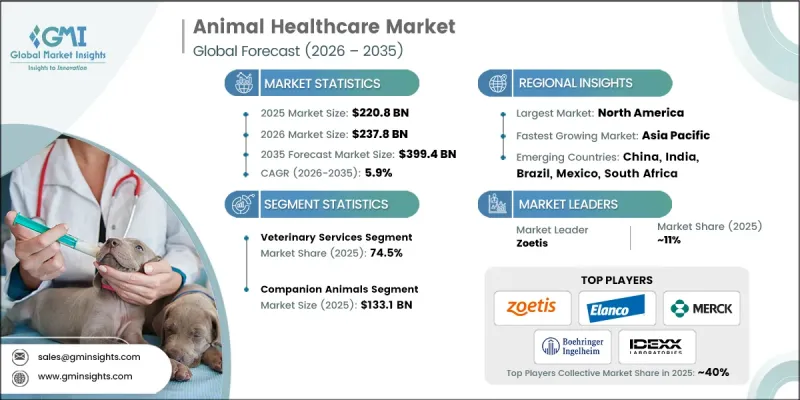

The Global Animal Healthcare Market was valued at USD 220.8 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 399.4 billion by 2035.

Market growth is influenced by the increasing occurrence of animal diseases, including both long-term health conditions and infectious illnesses that require advanced veterinary care. The rising interaction between humans and animals across agricultural settings, residential environments, and urban ecosystems has also elevated the importance of effective animal health management. The animal healthcare market encompasses a broad global industry dedicated to preventing, diagnosing, and treating medical conditions affecting both companion animals and livestock populations. It includes veterinary pharmaceuticals, vaccines, diagnostic solutions, medicated feed additives, medical equipment, and disposable supplies designed to protect animal health and support livestock productivity. In addition, improved disease control helps safeguard public health by reducing the risk of zoonotic disease transmission. The industry is gradually shifting away from generalized treatment methods toward more advanced preventive and targeted healthcare solutions. Increased adoption of biologics and specialized monoclonal antibodies for companion animals is becoming more common, while livestock healthcare is increasingly supported by modern vaccine technologies and herd-level disease prevention strategies. Personalized veterinary medicine is also gaining traction as diagnostic capabilities and biomarker-based testing become more widely available, allowing veterinarians to customize treatments based on species characteristics and specific health conditions. Furthermore, the development of patient-friendly therapeutic options is expanding treatment possibilities beyond conventional medication methods.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $220.8 Billion |

| Forecast Value | $399.4 Billion |

| CAGR | 5.9% |

The veterinary services segment held a 74.5% share in 2025 and is projected to grow at a CAGR of 6% throughout 2035. This strong market performance is largely driven by increasing disposable income levels and rising demand for professional veterinary care. Growing awareness about animal health and well-being has encouraged more individuals to seek comprehensive veterinary services for their animals. In addition, advancements in veterinary medical technologies have expanded the scope of services available within the sector. A wide range of pet-focused services has become more accessible, supporting higher utilization of veterinary facilities. The integration of modern healthcare technologies and improved service offerings is strengthening the overall veterinary services segment and supporting continued market expansion.

The companion animals segment generated USD 133.1 billion in 2025. This segment is categorized into several groups within the broader companion animal population. Rising global adoption of animals as household companions is a major factor supporting the growth of this segment. A significant portion of households worldwide currently care for animals as companions, contributing to increased demand for veterinary care, medical products, and specialized healthcare services. Higher spending on pet health and wellness is also encouraging the development and introduction of innovative animal healthcare solutions. In addition, growing disposable income levels in emerging economies are enabling more pet owners to invest in advanced healthcare products and veterinary services, further supporting the expansion of the companion animals segment.

North America Animal Healthcare Market held a 38.5% share in 2025. The region maintains a leading position due to its well-established veterinary healthcare infrastructure and widespread adoption of advanced medical solutions for animal care. Strong utilization of innovative therapeutics, vaccines, and parasite control products across both companion animal and livestock populations contributes to regional market growth. North America also benefits from the early implementation of advanced diagnostic technologies and precision veterinary healthcare approaches. The presence of major industry participants with strong research and development capabilities further accelerates innovation within the region. Growing awareness of preventive animal healthcare, along with increasing concern regarding chronic and zoonotic diseases affecting animals, continues to drive demand for advanced veterinary services and premium animal health products.

Key companies operating in the Global Animal Healthcare Market include Zoetis, Merck, Boehringer Ingelheim, Elanco Animal Health, Virbac, Vetoquinol, Ceva Sante Animale, Dechra Pharmaceuticals, IDEXX Laboratories, Phibro Animal Health, Neogen, HIPRA, B. Braun Vet Care (B Braun Melsungen), Symrise, Sklar Surgical Instruments, Medtronic, Endovac Animal Health, Indian Immunologicals, Kyoritsu Seiyaku, and Ourofino Saude Animal. Companies active in the Animal Healthcare Market are implementing several strategic approaches to strengthen their competitive position and expand their global footprint. A key focus area is investment in research and development aimed at introducing innovative veterinary pharmaceuticals, vaccines, and diagnostic technologies. Many organizations are also expanding their product portfolios through strategic partnerships, acquisitions, and collaborations with biotechnology firms and veterinary research institutions. Geographic expansion into emerging markets is another important strategy, as companies seek to capture rising demand for animal health products in developing regions. In addition, firms are enhancing digital capabilities by integrating data-driven diagnostics, tele-veterinary services, and advanced monitoring technologies into their offerings. Companies are also prioritizing sustainable production practices and regulatory compliance to maintain product credibility while supporting long-term growth in the animal healthcare market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing population of pet animals

- 3.2.1.2 Increasing support offered by government and public organizations for animal care

- 3.2.1.3 Growing demand for online veterinary pharmacies

- 3.2.1.4 Increase in animal healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with animal health drugs

- 3.2.2.2 Limited access in rural areas

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of telemedicine and remote veterinary consultation

- 3.2.3.2 Rising adoption of preventive and wellness-focused animal health solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape (Driven by Primary Research)

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape (Driven by Primary Research)

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East and Africa

- 3.6 Reimbursement scenario (Driven by Primary Research)

- 3.7 Venture capitalist scenario in animal health industry

- 3.8 Economic impacts of the animal health industry

- 3.9 Consumer behaviour trends (Driven by Primary Research)

- 3.10 Future market trends (Driven by Primary Research)

- 3.11 Impact of AI and generative AI on the market

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmaceuticals

- 5.2.1 Type

- 5.2.1.1 Drugs

- 5.2.1.1.1 Antiparasitic

- 5.2.1.1.2 Anti-inflammatory

- 5.2.1.1.3 Anti-infectives

- 5.2.1.1.4 Corticosteroids

- 5.2.1.1.5 Tranquilizers

- 5.2.1.1.6 Cardiovascular drugs

- 5.2.1.1.7 Gastrointestinal drugs

- 5.2.1.1.8 Other drugs

- 5.2.1.2 Vaccines

- 5.2.1.2.1 Modified live vaccines (MLV)

- 5.2.1.2.2 Killed inactivated vaccines

- 5.2.1.2.3 Other vaccines

- 5.2.1.3 Medicated feed additives

- 5.2.1.3.1 Antibiotics

- 5.2.1.3.2 Vitamins

- 5.2.1.3.3 Amino acids

- 5.2.1.3.4 Enzymes

- 5.2.1.3.5 Antioxidants

- 5.2.1.3.6 Prebiotics and probiotics

- 5.2.1.3.7 Minerals

- 5.2.1.3.8 Other medicated feed additives

- 5.2.1.1 Drugs

- 5.2.2 Indication

- 5.2.2.1 Dermatology

- 5.2.2.2 Cardiovascular diseases

- 5.2.2.3 Gastrointestinal diseases

- 5.2.2.4 Respiratory diseases

- 5.2.2.5 Other indications

- 5.2.3 Distribution channel

- 5.2.3.1 Veterinary hospital pharmacies

- 5.2.3.2 E-commerce

- 5.2.3.3 Retail pharmacies

- 5.2.1 Type

- 5.3 Medical devices

- 5.3.1 Veterinary diagnostic equipment

- 5.3.2 Anesthesia equipment

- 5.3.3 Patient monitoring equipment

- 5.3.4 Veterinary surgical equipment

- 5.3.5 Veterinary consumables

- 5.3.6 Other medical devices

- 5.4 Veterinary services

Chapter 6 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Horses

- 6.2.4 Other companion animals

- 6.3 Livestock animals

- 6.3.1 Poultry

- 6.3.2 Swine

- 6.3.3 Cattle

- 6.3.4 Fish

- 6.3.5 Other livestock animals

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 GCC Countries

- 7.6.3 Israel

Chapter 8 Company Profiles

- 8.1 B. Braun Vet Care (B Braun Melsungen)

- 8.2 Boehringer Ingelheim

- 8.3 Ceva Sante Animale

- 8.4 Dechra Pharmaceuticals

- 8.5 Elanco Animal Health

- 8.6 Endovac Animal Health

- 8.7 HIPRA

- 8.8 IDEXX Laboratories

- 8.9 Merck

- 8.10 Medtronic

- 8.11 Neogen

- 8.12 Sklar Surgical Instruments

- 8.13 Symrise

- 8.14 Vetoquinol

- 8.15 Virbac

- 8.16 Zoetis

- 8.17 Phibro Animal Health

- 8.18 Indian Immunologicals

- 8.19 Kyoritsu Seiyaku

- 8.20 Ourofino Saude Animal

动物用药品活性成分市场:依动物种类、产品类型、化合物类型、原料、应用及最终用户划分-2026-2032年全球市场预测

动物用药品活性成分市场:依动物种类、产品类型、化合物类型、原料、应用及最终用户划分-2026-2032年全球市场预测 兽医保健市场规模、份额、趋势和预测:按产品类型、动物种类、最终用户和地区划分(2026-2034 年)兽医护理市场:按动物类型、服务类型、执业模式、最终用户和通路类型划分-2026-2032年全球市场预测动物血浆製品及衍生市场:按类型、按衍生类型、按最终用户、按应用划分,全球预测(2026-2032年)兽医外科市场:按动物类型、手术类型、技术和最终用户划分,全球预测,2026-2032年猫科动物药品市场:依治疗领域、产品类型、给药途径及最终用户划分-2026-2032年全球预测

兽医保健市场规模、份额、趋势和预测:按产品类型、动物种类、最终用户和地区划分(2026-2034 年)兽医护理市场:按动物类型、服务类型、执业模式、最终用户和通路类型划分-2026-2032年全球市场预测动物血浆製品及衍生市场:按类型、按衍生类型、按最终用户、按应用划分,全球预测(2026-2032年)兽医外科市场:按动物类型、手术类型、技术和最终用户划分,全球预测,2026-2032年猫科动物药品市场:依治疗领域、产品类型、给药途径及最终用户划分-2026-2032年全球预测 兽用护肤产品市场规模、份额和成长分析:按产品类型、动物种类、成分类型、应用领域、分销渠道和地区划分-2026-2033年产业预测

兽用护肤产品市场规模、份额和成长分析:按产品类型、动物种类、成分类型、应用领域、分销渠道和地区划分-2026-2033年产业预测 全球动物保健市场规模、份额、趋势和成长分析报告(2026-2034年)兽医保健市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

全球动物保健市场规模、份额、趋势和成长分析报告(2026-2034年)兽医保健市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 施马伦贝格病毒治疗市场 - 全球产业规模、份额、趋势、机会及预测(按治疗类型、动物类型、地区和竞争格局划分,2021-2031年)

施马伦贝格病毒治疗市场 - 全球产业规模、份额、趋势、机会及预测(按治疗类型、动物类型、地区和竞争格局划分,2021-2031年)