|

市场调查报告书

商品编码

1998819

智慧车队管理市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Smart Fleet Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

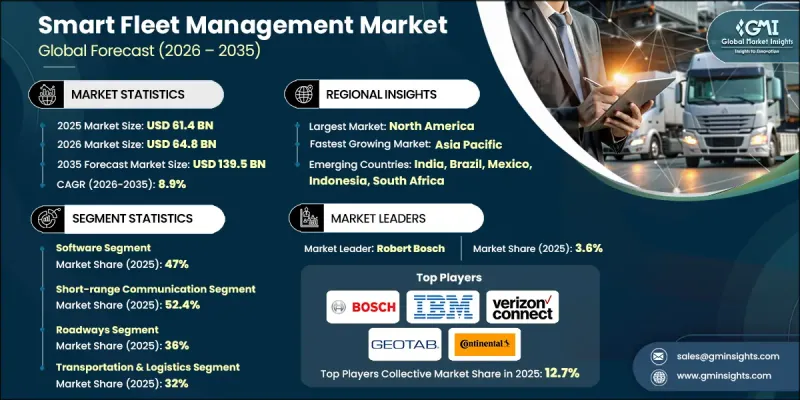

2025年全球智慧车队管理市场价值为614亿美元,预计2035年将以8.9%的复合年增长率成长至1,395亿美元。

随着企业日益重视营运视觉性和效率,市场蓄势待发,即将迎来显着成长。管理车队的企业正在投资智慧车队管理系统,以全面了解车辆位置、驾驶员表现和营运指标。这使管理人员能够做出数据驱动的决策,减少延迟,优化车队运转率,并提高整体效率。不断上涨的燃油成本和营运压力正在推动企业采用能够最大限度减少怠速、优化路线和追踪驾驶员行为的解决方案。透过利用分析和远端资讯处理技术,车队营运商可以降低油耗、提高生产力并实施预测性维护策略。联网汽车和物联网系统的日益整合也促进了即时监控和可操作洞察的实现,使各行各业的企业能够在提高成本效益和车队绩效的同时,应对营运挑战。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 起始金额 | 614亿美元 |

| 预测金额 | 1395亿美元 |

| 复合年增长率 | 8.9% |

截至2025年,短程通讯领域将占据52.4%的市场份额,预计到2035年将以8%的复合年增长率成长。蓝牙、RFID和Wi-Fi等技术可实现车辆之间或车辆与本地基础设施之间短距离的资料交换。这些解决方案支援局部监控、透过感测器快速更新数据,以及协调车辆在仓库、装卸点和园区运作中的运作。

到2025年,运输和物流行业将占据32%的市场份额。智慧车队管理工具可协助营运商优化车辆运转率、路线规划、驾驶员行为和燃油效率。即时追踪、预测性维护和分析功能可降低成本、确保准时交付,并提高区域和国际网路的营运效率。

预计到2025年,美国智慧车队管理市场规模将达210亿美元。美国商业车队营运商正在扩大远端资讯处理技术的应用,用于监控燃油消耗、优化配送路线和追踪驾驶员绩效。基于云端平台和人工智慧驱动的预测性维护解决方案正被广泛应用于各种类型的车辆。电子记录设备(ELD)相关法规的合规性进一步推动了即时报告和绩效基准测试,从而有助于提高大规模货运网路的安全性、课责和营运效率。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 成长驱动因素

- 即时车辆状态可视化

- 优化燃料成本

- 安全和合法令遵循

- 电子商务和最后一公里配送的成长

- 产业潜在风险与挑战

- 前期实施成本高

- 资料隐私与网路安全风险

- 市场机会

- 电动车充电基础设施的整合

- 拓展新兴市场

- 里程保险(UBI)

- 公共部门车辆管理数位化

- 成长驱动因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国国家公路交通安全管理局(NHTSA)

- 加拿大运输部车辆安全标准(CMVSS)

- 欧洲

- 欧洲车辆类型认证(WVTA)

- 欧洲经济共同体法规 124 (R124)

- 亚太地区

- 日本汽车标准协会(JASO)

- AIS(汽车产业标准)- 印度

- 拉丁美洲

- 巴西国家交通运输委员会(CONTRAN)-第242号决议

- 墨西哥官方标准 (Normas Oficiales Mexicanas)

- 中东和非洲

- ESMA(阿联酋标准化和计量局)

- 南非标准局(SABS)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析(基于初步调查)

- 对过去价格趋势的分析

- 按球员类型分類的定价策略(高端/超值/成本加成)

- 成本細項分析

- 专利分析(基于初步研究)

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- GenAI 各细分市场的应用案例与部署蓝图

- 风险、限制和监管考量

- 基础设施和实施情况(基于初步调查)

- 按地区和购买者群体分類的采用率

- 基础设施投资的可扩展性限制和趋势

- 预测假设和情境分析(基于初步研究)

- 基本案例-驱动复合年增长率的关键宏观经济与产业变量

- 乐观情境-宏观经济与产业的顺风

- 悲观情景-宏观经济放缓或产业逆风

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

- 企业级分层基准测试

- 层级分类标准与选择标准

- 按收入、地区和创新能力分類的层级定位矩阵。

第五章 市场估计与预测:依组件划分,2022-2035年

- 硬体

- 追踪设备

- 车载资讯设备

- 感应器

- 远距离诊断

- 通讯设备

- 其他的

- 软体

- 车辆追踪

- 路线优化

- 合规与报告

- 其他的

- 服务

- 专业服务

- 咨询与整合

- 客製化

- 系统实现

- 託管服务

- 远端监控

- 支援与维护

- 专业服务

第六章 市场估算与预测:依连结技术划分,2022-2035年

- 近距离场通讯

- 远端通讯

- 杂交种

第七章 市场估计与预测:依运输方式划分,2022-2035年

- 路

- 海

- 航空

- 铁路

第八章 市场估算与预测:依最终用途产业划分,2022-2035年

- 运输/物流

- 零售与电子商务

- 医疗和紧急服务

- 石油和天然气

- 建筑和采矿

- 现场服务

- 政府/公共部门

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 越南

- 印尼

- 菲律宾

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Cisco Systems

- Continental

- Denso

- General Motors

- IBM

- Infineon Technologies

- Magellan and Trimble Navigation

- Robert Bosch

- Siemens

- Zonar Systems

- 当地公司

- MiX Telematics

- Samsara

- Teletrac Navman

- Omnitracs

- Fleet Complete

- Hitachi

- Powerfleet

- Gurtam(Wialon)

- 新兴企业

- Azuga

- CalAmp

- Noregon

- Zubie

The Global Smart Fleet Management Market was valued at USD 61.4 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 139.5 billion by 2035.

Market growth is poised for significant growth as businesses increasingly prioritize operational visibility and efficiency. Companies managing vehicle fleets are investing in smart fleet management systems to gain comprehensive oversight of vehicle locations, driver performance, and operational metrics. This enables managers to make data-driven decisions, reduce delays, optimize fleet utilization, and improve overall efficiency. Rising fuel costs and operational pressures are driving the adoption of solutions that minimize idling, optimize routes, and track driver behavior. By leveraging analytics and telematics, fleet operators can reduce fuel consumption, enhance productivity, and implement predictive maintenance strategies. The growing integration of connected vehicles and IoT-enabled systems also facilitates real-time monitoring and actionable insights, enabling companies to address operational challenges while improving cost efficiency and fleet performance across industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.4 Billion |

| Forecast Value | $139.5 Billion |

| CAGR | 8.9% |

The short-range communication segment held a 52.4% share in 2025 and is expected to grow at a CAGR of 8% through 2035. Technologies such as Bluetooth, RFID, and Wi-Fi allow limited-distance data exchange between vehicles or between vehicles and local infrastructure. These solutions support localized monitoring, rapid updates via sensors, and fleet coordination across depots, loading points, and campus operations.

The transportation and logistics sector accounted for 32% share in 2025. Smart fleet management tools help operators optimize vehicle utilization, route planning, driver behavior, and fuel efficiency. Real-time tracking, predictive maintenance, and analytics reduce costs, ensure timely deliveries, and enhance operational efficiency across regional and international networks.

U.S. Smart Fleet Management Market reached USD 21 billion in 2025. Commercial fleet operators in the U.S. increasingly use telematics to monitor fuel usage, optimize delivery routes, and track driver performance. Cloud-based platforms and AI-driven predictive maintenance solutions are widely adopted across different vehicle types. Regulatory compliance for electronic logging devices (ELDs) further supports real-time reporting and performance benchmarking, improving safety, accountability, and operational efficiency across large trucking networks.

Key players in the Global Smart Fleet Management Market include IBM, Cisco Systems, Siemens, Continental, Denso, Infineon Technologies, Robert Bosch, Magellan and Trimble Navigation, Zonar Systems, and General Motors. Companies in the Smart Fleet Management Market are leveraging multiple strategies to solidify their market presence. Key approaches include investing in advanced telematics and IoT platforms that enable real-time fleet tracking and predictive analytics. Strategic partnerships with logistics operators and automotive manufacturers allow firms to expand their customer base and integrate solutions across vehicle types. Several players are enhancing their offerings through AI-driven route optimization, fuel management tools, and driver behavior monitoring systems. Expansion into new geographic regions and development of modular, scalable solutions provide flexibility for small and large fleet operators alike. Additionally, firms are focusing on regulatory compliance, cybersecurity, and cloud-based platforms to maintain trust, improve operational efficiency, and strengthen competitive positioning in the global smart fleet management market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Connectivity technology

- 2.2.4 Transport mode

- 2.2.5 End use industry

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Real-time fleet visibility

- 3.2.1.2 Fuel cost optimization

- 3.2.1.3 Safety & compliance regulations

- 3.2.1.4 E-commerce & last-mile delivery growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial deployment costs

- 3.2.2.2 Data privacy & cybersecurity risks

- 3.2.3 Market opportunities

- 3.2.3.1 EV charging infrastructure integration

- 3.2.3.2 Emerging market expansion

- 3.2.3.3 Usage-based insurance (UBI)

- 3.2.3.4 Public sector fleet digitization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Whole Vehicle Type Approval (WVTA)

- 3.4.2.2 ECE Regulation 124 (R124)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automotive Standards Organization (JASO)

- 3.4.3.2 AIS (Automotive Industry Standards) - India

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) - Resolution 242

- 3.4.4.2 Mexican NOM Standards (Normas Oficiales Mexicanas)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Infrastructure & deployment landscape (driven by primary research)

- 3.13.1 Deployment penetration by region & buyer segment

- 3.13.2 Scalability constraints & infrastructure investment trends

- 3.14 Forecast assumptions & scenario analysis (driven by primary research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Tracking devices

- 5.2.2 Telematics devices

- 5.2.3 Sensors

- 5.2.4 Remote diagnostics

- 5.2.5 Communication devices

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Vehicle tracking

- 5.3.2 Route optimization

- 5.3.3 Compliance & reporting

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional services

- 5.4.1.1 Consulting & integration

- 5.4.1.2 Customization

- 5.4.1.3 System deployment

- 5.4.2 Managed services

- 5.4.2.1 Remote monitoring

- 5.4.2.2 Support & maintenance

- 5.4.1 Professional services

Chapter 6 Market Estimates & Forecast, By Connectivity Technology, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Short-range communication

- 6.3 Long-range communication

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Transport Mode, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Roadways

- 7.3 Marine

- 7.4 Airways

- 7.5 Railways

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Transportation & logistics

- 8.3 Retail & e-commerce

- 8.4 Healthcare & emergency services

- 8.5 Oil & gas

- 8.6 Construction & mining

- 8.7 Field services

- 8.8 Government & public sector

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Cisco Systems

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 General Motors

- 10.1.5 IBM

- 10.1.6 Infineon Technologies

- 10.1.7 Magellan and Trimble Navigation

- 10.1.8 Robert Bosch

- 10.1.9 Siemens

- 10.1.10 Zonar Systems

- 10.2 Regional players

- 10.2.1 MiX Telematics

- 10.2.2 Samsara

- 10.2.3 Teletrac Navman

- 10.2.4 Omnitracs

- 10.2.5 Fleet Complete

- 10.2.6 Hitachi

- 10.2.7 Powerfleet

- 10.2.8 Gurtam (Wialon)

- 10.3 Emerging players

- 10.3.1 Azuga

- 10.3.2 CalAmp

- 10.3.3 Noregon

- 10.3.4 Zubie

智慧车队管理市场:按组件、应用、部署模式、连接方式和车辆类型划分-2026-2032年全球市场预测

智慧车队管理市场:按组件、应用、部署模式、连接方式和车辆类型划分-2026-2032年全球市场预测 共用电动车队管理和订阅式旅游市场预测至2034年:按车辆类型、服务模式、车队管理功能、最终用户和地区分類的全球分析智慧车队事件管理市场预测至2034年-按组件、部署模式、车队类型、事件类型、最终用户和地区分類的全球分析

共用电动车队管理和订阅式旅游市场预测至2034年:按车辆类型、服务模式、车队管理功能、最终用户和地区分類的全球分析智慧车队事件管理市场预测至2034年-按组件、部署模式、车队类型、事件类型、最终用户和地区分類的全球分析 2026年全球智慧车队管理市场报告智慧车队远端资讯处理市场预测:至 2034 年:全球解决方案、硬体、运输方式、连接方式、车队规模、最终用户和区域分析

2026年全球智慧车队管理市场报告智慧车队远端资讯处理市场预测:至 2034 年:全球解决方案、硬体、运输方式、连接方式、车队规模、最终用户和区域分析 智慧车队管理市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球智慧车队管理市场规模、份额、趋势和成长分析报告:2026-2034年

智慧车队管理市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球智慧车队管理市场规模、份额、趋势和成长分析报告:2026-2034年 智慧车队管理市场-全球产业规模、份额、趋势、机会及预测(按模式、应用、连接方式、营运模式、地区和竞争格局划分,2021-2031年)智慧公车交通管理系统市场:按组件、公车类型、服务、应用和部署模式划分-全球预测,2026-2032年

智慧车队管理市场-全球产业规模、份额、趋势、机会及预测(按模式、应用、连接方式、营运模式、地区和竞争格局划分,2021-2031年)智慧公车交通管理系统市场:按组件、公车类型、服务、应用和部署模式划分-全球预测,2026-2032年 智慧车队管理市场规模、份额和成长分析(按模式、连接方式、营运方式、应用领域和地区划分)-2026-2033年产业预测

智慧车队管理市场规模、份额和成长分析(按模式、连接方式、营运方式、应用领域和地区划分)-2026-2033年产业预测