|

市场调查报告书

商品编码

1998821

工业阀门市场机会、成长要素、产业趋势分析及2026-2035年预测Industrial Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

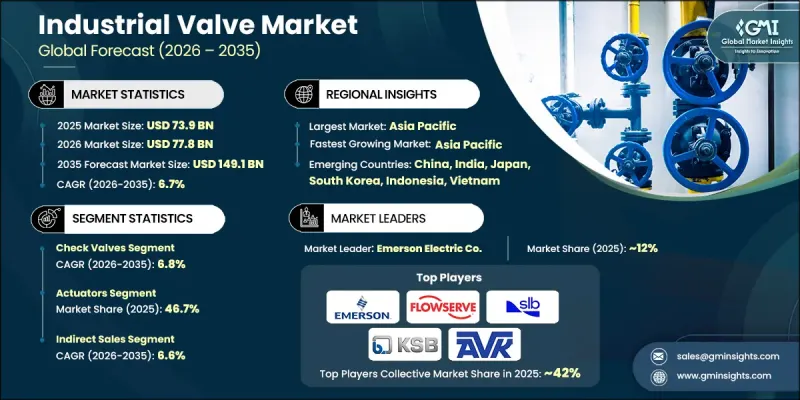

预计到 2025 年,全球工业阀门市场规模将达到 739 亿美元,并以 6.7% 的复合年增长率成长,到 2035 年将达到 1,491 亿美元。

随着全球电力生产和大型基础设施建设投资的加速,工业阀门市场持续成长。公共和私营部门都在增加对发电厂、公共产业系统和工业加工设施的资本投入,显着提升了对先进阀门技术的需求。阀门在工业系统中,尤其是在能源生产和资源开采活动中,对流量控制和压力稳定性起着至关重要的作用。随着全球可再生能源设施的扩张,现代能源系统中使用的复杂管道网路需要可靠的阀门来高效调节流体流动。都市区的基础设施现代化也促进了市场成长,特别是为满足不断增长的人口需求而进行的供水和污水处理系统的扩张。工业阀门仍然是众多工业环境中维持管路安全、运作可靠性和高效製程控制的关键组件。石化产能的扩张进一步推动了需求,因为加工设施需要大规模的阀门安装来支援连续运作。此外,在大规模工程建设计划中,阀门系统越来越多地从设计和规划阶段就被纳入考量,以确保长期运作效率并符合安全标准。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 739亿美元 |

| 预测金额 | 1491亿美元 |

| 复合年增长率 | 6.7% |

预计到2025年,止回阀市场规模将达到144亿美元,并预计在2026年至2035年间以6.8%的复合年增长率成长。止回阀是应用最广泛的阀门之一,在防止管道系统回流方面发挥着至关重要的作用。透过维持流体单向流动,这些阀门有助于保护泵浦、管道和製程设备免受运作中损坏。其相对简单的机械设计确保了系统的可靠性能,同时减少了维护需求。在严苛的压力条件下仍能维持高耐久性,进一步增强了其在工业环境中的适用性。管道基础设施和工业设施的持续扩张正在推动全球对这类阀门系统的持续需求。

预计到2025年,执行器市占率将达到46.7%,并在2026年至2035年间以7.2%的复合年增长率成长。随着工业营运中自动化程度的不断提高,执行器正成为关键组件类别。自动化阀门系统显着提高了製程精度、运作可靠性和整体系统效率。在复杂的加工环境中运行的行业越来越依赖执行器驱动的阀门来实现远端操作和集中式流程管理。先进的执行器技术提高了系统反应速度,同时最大限度地减少了手动调节的需求。与数位控制系统的整合还可以实现即时效能监控和运行优化。随着各行业不断推进设施现代化以提高生产效率和安全标准,预计执行器的全球应用将保持强劲势头。

预计到2025年,中国工业阀门市场规模将达92亿美元。这一市场成长主要得益于强大的工业製造能力和大规模的能源基础设施建设。电力设施的大量投资推动了各行业对工业阀门的需求成长。此外,石化生产基础设施的扩展也带动了对能够应对严苛运作况的高性能阀门的需求。旨在改善水资源管理系统的大规模城市基础设施项目,也为阀门技术的稳定供应提供了保障。国内製造商持续扩大产能,以支持重大工业和基础设施计划。出口导向设备製造进一步支撑了全球市场的稳定替换需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 扩大能源和基础设施投资

- 智慧阀门和物联网阀门技术的应用

- 工业自动化和工业4.0的引入

- 陷阱与挑战

- 原物料价格波动和供应链不稳定

- 严格的监管合规和认证要求

- 机会

- 进入可再生能源和清洁能源基础设施市场

- 开发耐腐蚀和性能增强材料

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监理情势

- 标准和合规要求

- 区域法律规范

- 认证标准

- 贸易统计(HS编码 - 8481)

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 球阀

- 单向阀

- 蝶阀

- 闸阀

- 球阀

- 塞阀

- 隔膜阀

- 安全阀

第六章 市场估计与预测:依材料划分,2022-2035年

- 钢

- 塑胶

- 铸铁

- 合金基体

- 其他的

第七章 市场估计与预测:依组件划分,2022-2035年

- 执行器

- 阀体

- 其他的

第八章 市场规模估算与预测(2022-2035年)

- <1"

- 1英寸至6英寸

- 7英寸至25英寸

- 26英寸至50英寸

- 50吋或更大

第九章 市场估计与预测:依最终用途划分,2022-2035年

- 化学

- 能源与公共产业

- 建造

- 金属和采矿

- 农业

- 製药

- 食品/饮料

- 纸浆和造纸

- 其他的

第十章 市场估价与预测:依通路划分,2022-2035年

- 直销

- 间接销售

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十二章:公司简介

- ALFA LAVAL

- AVK Holding A/S

- Baker Hughes Company

- Crane Company

- Danfoss

- Emerson Electric Co.

- Georg Fischer Ltd.

- Hitachi, Ltd.

- ITT INC.

- KITZ Corporation

- KSB SE &Co. KGaA

- Mueller Co. LLC.

- SLB(Schlumberger Limited.)

- TechnipFMC plc

- The Weir Group PLC

The Global Industrial Valve Market was valued at USD 73.9 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 149.1 billion by 2035.

The industrial valve market continues to gain momentum as global investment in energy generation and large-scale infrastructure development accelerates. Both public and private sector organizations are increasing capital spending on power plants, utility systems, and industrial processing facilities, which significantly boosts the demand for advanced valve technologies. Valves play a fundamental role in managing flow control and pressure stability across industrial systems, particularly in energy production and resource extraction activities. As renewable energy installations expand globally, complex piping networks used in modern energy systems require highly reliable valves to regulate fluid movement efficiently. Infrastructure upgrades across urban regions are also contributing to market growth, particularly as water distribution and wastewater treatment systems expand to meet rising population demands. Industrial valves remain essential components in maintaining pipeline safety, operational reliability, and efficient process control across numerous industrial environments. Growing petrochemical production capacity further contributes to demand, as processing facilities require extensive valve installations to support continuous operations. Additionally, large engineering and construction projects increasingly incorporate valve systems during the design and planning stages to ensure long-term operational efficiency and safety compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $73.9 Billion |

| Forecast Value | $149.1 Billion |

| CAGR | 6.7% |

The check valves segment generated USD 14.4 billion in 2025 and is expected to grow at a CAGR of 6.8% from 2026 through 2035. Check valves represent one of the most widely used valve types because they play a critical role in preventing reverse flow within pipeline systems. By maintaining one-directional fluid movement, these valves help protect pumps, pipelines, and process equipment from operational damage. Their relatively simple mechanical design reduces maintenance requirements while ensuring dependable system performance. High durability under demanding pressure conditions further strengthens their suitability for industrial environments. Ongoing expansion of pipeline infrastructure and industrial facilities continues to reinforce global demand for these valve systems.

The actuators segment held 46.7% share in 2025 and is forecast to grow at a CAGR of 7.2% between 2026 and 2035. Actuators have emerged as the leading component category due to the increasing adoption of automation across industrial operations. Automated valve systems significantly enhance process precision, operational reliability, and overall system efficiency. Industries operating complex processing environments increasingly rely on actuator-driven valves to enable remote operation and centralized process management. Advanced actuator technologies improve system responsiveness while minimizing the need for manual adjustments. Integration with digital control systems also allows real-time performance monitoring and operational optimization. As industries continue modernizing facilities to improve productivity and safety standards, actuator adoption is expected to remain strong worldwide.

China Industrial Valve Market accounted for USD 9.20 billion in 2025. The country's market growth is supported by extensive industrial manufacturing capacity and large-scale energy infrastructure development. Significant investments in power generation facilities are contributing to higher demand for industrial valve installations across multiple industrial segments. Expansion of petrochemical production infrastructure is also increasing the need for high-performance valves capable of handling demanding operational conditions. In addition, large urban infrastructure programs aimed at improving water management systems are generating consistent procurement demand for valve technologies. Domestic manufacturers continue expanding production capacity to support major industrial and infrastructure projects. Export-oriented equipment manufacturing further sustains steady replacement demand in global markets.

Major companies participating in the Global Industrial Valve Market include Emerson Electric Co., Crane Company, Danfoss, Baker Hughes Company, SLB, TechnipFMC plc, The Weir Group PLC, ITT Inc., KITZ Corporation, KSB SE & Co. KGaA, Hitachi Ltd., Georg Fischer Ltd., Mueller Co. LLC., AVK Holding A/S, and Alfa Laval. Companies operating in the Industrial Valve Market are strengthening their competitive position by focusing on innovation, strategic partnerships, and global expansion initiatives. Many manufacturers are investing in advanced valve technologies that support automation, digital monitoring, and predictive maintenance capabilities. Continuous research and development efforts are helping companies improve valve durability, operational efficiency, and compatibility with complex industrial systems. Strategic acquisitions and collaborations allow firms to expand their product portfolios and gain access to specialized technologies and regional markets. Manufacturers are also increasing investments in production facilities and supply chain networks to support growing infrastructure and energy projects worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Material

- 2.2.3 Component

- 2.2.4 Size

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding energy and infrastructure investments

- 3.2.1.2 Adoption of smart and IoT-enabled valve technologies

- 3.2.1.3 Industrial automation and Industry 4.0 implementation

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Raw material price volatility and supply chain instability

- 3.2.2.2 Stringent regulatory compliance and certification demands

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into renewable and clean energy infrastructure

- 3.2.3.2 Development of corrosion-resistant and performance-enhancing materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code - 8481)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Ball Valves

- 5.3 Check Valves

- 5.4 Butterfly Valves

- 5.5 Gate Valves

- 5.6 Globe Valves

- 5.7 Plug Valves

- 5.8 Diaphragm Valves

- 5.9 Safety Valves

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Plastic

- 6.4 Cast Iron

- 6.5 Alloy Based

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Component, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Actuators

- 7.3 Valve Body

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Size, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 <1"

- 8.3 1" to 6"

- 8.4 7" to 25"

- 8.5 26" to 50"

- 8.6 >50"

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Chemical

- 9.3 Energy & Utilities

- 9.4 Construction

- 9.5 Metal & Mining

- 9.6 Agriculture

- 9.7 Pharmaceutical

- 9.8 Food & Beverage

- 9.9 Pulp & Paper

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 ALFA LAVAL

- 12.2 AVK Holding A/S

- 12.3 Baker Hughes Company

- 12.4 Crane Company

- 12.5 Danfoss

- 12.6 Emerson Electric Co.

- 12.7 Georg Fischer Ltd.

- 12.8 Hitachi, Ltd.

- 12.9 ITT INC.

- 12.10 KITZ Corporation

- 12.11 KSB SE & Co. KGaA

- 12.12 Mueller Co. LLC.

- 12.13 SLB (Schlumberger Limited.)

- 12.14 TechnipFMC plc

- 12.15 The Weir Group PLC

工业阀门市场分析及预测(至2035年):类型、产品类型、技术、应用、材质、製程、最终用户、功能、安装配置、解决方案

工业阀门市场分析及预测(至2035年):类型、产品类型、技术、应用、材质、製程、最终用户、功能、安装配置、解决方案 工业阀门市场规模、份额、趋势和预测:按产品类型、功能、材质、尺寸、最终用途行业和地区划分(2026-2034 年)

工业阀门市场规模、份额、趋势和预测:按产品类型、功能、材质、尺寸、最终用途行业和地区划分(2026-2034 年) 拍击阀市场:材质、尺寸、压力等级、驱动方式、应用及通路划分-2026-2032年全球市场预测工业喷雾阀市场:2026-2032年全球市场预测(依产品类型、操作机构、材质、喷雾模式、应用及最终用户产业划分)

拍击阀市场:材质、尺寸、压力等级、驱动方式、应用及通路划分-2026-2032年全球市场预测工业喷雾阀市场:2026-2032年全球市场预测(依产品类型、操作机构、材质、喷雾模式、应用及最终用户产业划分) 2026-2030年全球石油天然气工业阀门市场反硝化喷嘴市场:依喷嘴类型、材料、压力类型、安装类型、应用、最终用户产业划分,全球预测(2026-2032年)双流体喷嘴市场:按喷嘴类型、材料、应用、最终用户和销售管道,全球预测,2026-2032年多喷嘴喷雾过热器市场(按喷嘴类型、安装类型、最终用途行业、应用和分销渠道划分),全球预测,2026-2032年按类型、材料、分销通路、终端用户产业和应用程式分類的狭缝喷嘴市场-全球预测,2026-2032年

2026-2030年全球石油天然气工业阀门市场反硝化喷嘴市场:依喷嘴类型、材料、压力类型、安装类型、应用、最终用户产业划分,全球预测(2026-2032年)双流体喷嘴市场:按喷嘴类型、材料、应用、最终用户和销售管道,全球预测,2026-2032年多喷嘴喷雾过热器市场(按喷嘴类型、安装类型、最终用途行业、应用和分销渠道划分),全球预测,2026-2032年按类型、材料、分销通路、终端用户产业和应用程式分類的狭缝喷嘴市场-全球预测,2026-2032年 全球喷嘴市场规模、份额、趋势和成长分析报告(2026-2034)

全球喷嘴市场规模、份额、趋势和成长分析报告(2026-2034)