|

市场调查报告书

商品编码

1998827

犬类特异性皮肤炎市场:市场机会、成长要素、产业趋势分析及2026-2035年预测Canine Atopic Dermatitis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

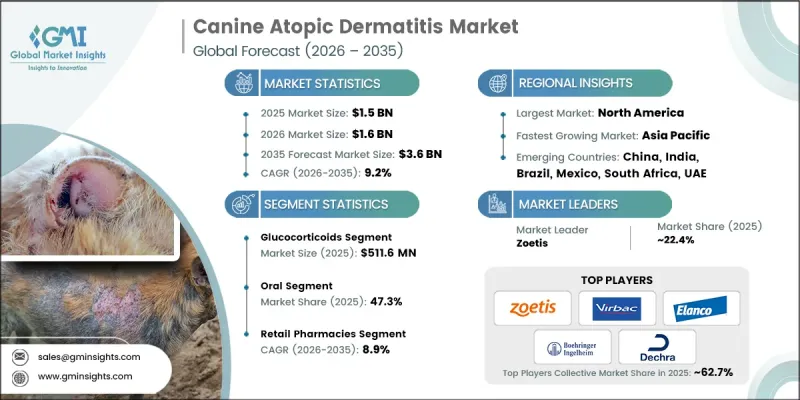

2025 年全球犬类异位性皮肤炎市场价值为 15 亿美元,预计到 2035 年将以 9.2% 的复合年增长率增长至 36 亿美元。

犬异位性皮肤炎盛行率的上升以及人们对伴侣动物保健日益增长的关注,是推动该市场成长的主要因素。宠物饲主对宠物健康的日益重视,也带动了对先进兽医皮肤病治疗的需求。此外,兽药的创新也对市场产生了积极影响,因为宠物饲主和兽医都在寻求安全、有效且针对性强的慢性皮肤病治疗方法。已开发市场和新兴市场兽医基础设施的不断改进以及专科诊所的增多,使得更多犬隻能够得到正确的诊断和治疗。新兴市场居民可支配收入的增加,进一步促进了对宠物保健的投资。随着人们对预防性和持续性皮肤护理重要性的认识不断提高,犬特发性皮肤炎市场在各个地区都呈现出稳定且持续的成长态势。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 15亿美元 |

| 预计金额 | 36亿美元 |

| 复合年增长率 | 9.2% |

犬特异性皮肤炎是一种慢性发炎性皮肤病,与遗传因素有关,由对螨虫、花粉、真菌或某些食物等环境过敏原的超敏反应引发。此病会引发过度免疫反应,导致持续性搔痒、发红以及反覆发生的皮肤和耳部感染疾病。单株抗体和口服疗法等创新兽药治疗方法的研发显着改变了此疾病的治疗管理。单株抗体可针对并缓解搔痒和炎症,而口服疗法则具有长期治疗的便利性和有效性。人们对伴侣动物健康(尤其是在新兴经济体)的认识不断提高,这正在推动兽药疗法的应用和投资不断增长。

预计到2025年,糖皮质激素类药物市场规模将达5.116亿美元。这些药物,包括泼尼松和地塞米松,能迅速有效地缓解发炎和搔痒,因此是治疗重症和急性发作的第一线药物。与新型标靶治疗相比,它们价格实惠,这促进了其持续普及,尤其是在兽医资源匮乏、宠物保险覆盖率低的地区。

预计到2025年,口服给药途径将占47.3%的市占率。奥克拉替尼和糖皮质激素等口服药物因其使用方便性而受到宠物饲主的青睐,有助于提高用药依从性并确保治疗的持续性。这些治疗方法能够迅速缓解搔痒和炎症,对急性和慢性症状均有效。标靶口服疗法透过特异性调节发炎路径来增强疗效,因此在兽医皮肤病学领域越来越受欢迎。

北美犬类异位性皮肤炎市场占据41%的市场份额,预计到2035年将以9%的复合年增长率成长。该地区市场成长的主要驱动因素包括:完善的兽医基础设施、创新皮肤病治疗方案的普及以及单株抗体等先进治疗方法的广泛应用。宠物饲主日益增长的专业照护意愿以及犬类慢性皮肤病的高发生率进一步巩固了北美市场的领先地位。

目录

第一章:调查方法

- 市场范围和定义

- 研究途径

- 对品质的承诺

- GMI的AI政策与对资料完整性的承诺

- 资讯来源一致性通讯协定

- GMI的AI政策与对资料完整性的承诺

- 调查过程和可靠性评分

- 研究路径的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 收入份额分析

- 基准年的计算

- 预测模型

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 宠物数量的增加和宠物的人性化

- 对皮肤疾病和先进治疗方法方案的认识不断提高

- 产业潜在风险与挑战

- 某些药物的副作用

- 人用药品的仿单标示外使用

- 市场机会

- 联合治疗的需求和使用增加

- 开发一种用于治疗儿童溃疡性大肠炎的药物

- 促进因素

- 成长潜力分析

- 监理情势(基于初步调查)

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 北美洲

- 价格分析(基于初步调查)

- 研发管线和临床试验趋势

- 未来市场趋势

- 人工智慧和生成式人工智慧对市场的影响

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 糖皮质激素

- 抗组织胺药

- 免疫抑制剂

- 单株抗体

- 其他产品

第六章 市场估计与预测:依给药途径划分,2022-2035年

- 口服

- 外用

- 注射药物

第七章 市场估价与预测:依通路划分,2022-2035年

- 零售药房

- 兽药

- 网路药房

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- AB Science

- Boehringer Ingelheim

- Ceva

- Dechra Veterinary Products

- Elanco

- Kindred Biosciences

- Nextmune(Vimian)

- Phibro Animal Health Corporation

- Toray Industries

- Vetoquinol

- Virbac

- Zoetis

The Global Canine Atopic Dermatitis Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 3.6 billion by 2035.

The market growth is driven by the rising prevalence of atopic dermatitis in dogs and a growing focus on companion animal healthcare. Increasing awareness among pet owners about their pets' well-being is fueling demand for advanced veterinary dermatology therapies. The market is also benefiting from innovations in veterinary medications, as pet owners and veterinarians seek safe, effective, and targeted treatment options for chronic skin conditions. With the expansion of veterinary infrastructure and specialized clinics in both developed and emerging regions, more dogs are receiving proper diagnosis and treatment. Rising disposable incomes in emerging markets further encourage investments in pet healthcare. As awareness of the importance of preventative and ongoing dermatological care spreads, the canine atopic dermatitis market is witnessing steady and sustained growth across geographies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 9.2% |

Canine atopic dermatitis is a chronic, genetically influenced inflammatory skin disorder caused by hypersensitivity to environmental allergens like dust mites, pollen, mold, or specific foods. The condition triggers an exaggerated immune response, resulting in persistent itching, redness, and recurrent skin and ear infections. The development of innovative veterinary treatments such as monoclonal antibodies and oral therapies has transformed disease management. Monoclonal antibodies offer targeted relief from pruritus and inflammation, while oral therapies provide convenience and efficacy for long-term treatment. Rising knowledge of companion animal health, especially in emerging economies, is driving higher adoption rates and increased investment in veterinary therapeutics.

The glucocorticoids segment generated USD 511.6 million in 2025. These medications, including prednisone and dexamethasone, are highly effective in rapidly alleviating inflammation and itching, making them the preferred choice for severe or acute flare-ups. Their affordability compared to newer targeted therapies supports their continued adoption, particularly in regions with limited access to advanced veterinary care or low pet insurance penetration.

The oral administration segment held a 47.3% share in 2025. Oral medications like oclacitinib and glucocorticoids are favored by pet owners due to ease of use, which improves compliance and ensures consistent treatment. These therapies deliver fast relief for pruritus and inflammation and are effective for both acute and chronic conditions. Targeted oral treatments enhance efficacy by specifically modulating inflammatory pathways, reinforcing their popularity in veterinary dermatology practices.

North America Canine Atopic Dermatitis Market held 41% share and is expected to grow at a 9% CAGR through 2035. Strong veterinary infrastructure, access to innovative dermatology treatments, and widespread adoption of advanced therapies such as monoclonal antibodies are supporting regional market growth. Pet owners' increasing willingness to invest in specialized care and the prevalence of chronic dermatological conditions among dogs further strengthen North America's market leadership.

Key players operating in the Global Canine Atopic Dermatitis Market include AB Science, Boehringer Ingelheim, Ceva, Dechra Veterinary Products, Elanco Animal Health, Kindred Biosciences, Nextmune, Phibro Animal Health Corporation, Toray Industries, Vetoquinol, Virbac, and Zoetis. Companies in the Global Canine Atopic Dermatitis Market are focusing on R&D to develop innovative therapies, including monoclonal antibodies, targeted oral medications, and combination treatments. They are investing in clinical trials to demonstrate safety and efficacy while expanding product portfolios to address different severity levels and breeds. Strategic collaborations with veterinary clinics and distribution partners, along with educational initiatives to increase awareness among pet owners and veterinarians, are central to expanding market reach. Firms are also entering emerging markets and leveraging digital marketing to increase product adoption and improve brand visibility, enhancing their competitive position.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Route of administration trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and humanization of pets

- 3.2.1.2 Increased awareness of skin disorders and advanced treatment options

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Side effect of few medications

- 3.2.2.2 Off-label use of human drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand and utilization of combination therapies

- 3.2.3.2 Development of pediatric ulcerative colitis treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Pricing analysis (Driven by primary research)

- 3.6 Pipeline and clinical trials landscape

- 3.7 Future market trends

- 3.8 Impact of AI and generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Glucocorticoids

- 5.3 Antihistamines

- 5.4 Immunosuppressants

- 5.5 MAbs

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Topical

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Retail pharmacies

- 7.3 Veterinary hospital pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AB Science

- 9.2 Boehringer Ingelheim

- 9.3 Ceva

- 9.4 Dechra Veterinary Products

- 9.5 Elanco

- 9.6 Kindred Biosciences

- 9.7 Nextmune (Vimian)

- 9.8 Phibro Animal Health Corporation

- 9.9 Toray Industries

- 9.10 Vetoquinol

- 9.11 Virbac

- 9.12 Zoetis

异位性皮肤炎市场:2026-2032年全球市场预测(依产品、给药途径、严重程度、病患细分及分销管道划分)

异位性皮肤炎市场:2026-2032年全球市场预测(依产品、给药途径、严重程度、病患细分及分销管道划分) 异位性皮肤炎治疗市场分析及预测(至2035年):按类型、产品类型、应用、最终用户、技术、剂型、组件、实施类型、流程和解决方案划分

异位性皮肤炎治疗市场分析及预测(至2035年):按类型、产品类型、应用、最终用户、技术、剂型、组件、实施类型、流程和解决方案划分 全球异位性皮肤炎治疗市场规模、份额、趋势和成长分析报告(2026-2034年)全球异位性皮肤炎治疗市场规模、份额、趋势和成长分析报告(2026-2034年)

全球异位性皮肤炎治疗市场规模、份额、趋势和成长分析报告(2026-2034年)全球异位性皮肤炎治疗市场规模、份额、趋势和成长分析报告(2026-2034年) 特应性疾病治疗市场:按疾病类型、药物类别、给药途径、最终用户、分销管道、患者类型和地区划分足底压力分析垫市场:按产品类型、感测器技术、应用、最终用户和分销管道划分 - 全球预测(2026-2032年)

特应性疾病治疗市场:按疾病类型、药物类别、给药途径、最终用户、分销管道、患者类型和地区划分足底压力分析垫市场:按产品类型、感测器技术、应用、最终用户和分销管道划分 - 全球预测(2026-2032年) 异位性皮肤炎治疗市场规模、份额及成长分析(依治疗类型、年龄层、严重程度及地区划分)-2026-2033年产业预测

异位性皮肤炎治疗市场规模、份额及成长分析(依治疗类型、年龄层、严重程度及地区划分)-2026-2033年产业预测 异位性皮肤炎治疗市场规模、份额和成长分析(按给药途径、药物类别、分销管道和地区划分)—产业预测,2026-2033年

异位性皮肤炎治疗市场规模、份额和成长分析(按给药途径、药物类别、分销管道和地区划分)—产业预测,2026-2033年 异位性皮肤炎药物市场-全球产业规模、份额、趋势、机会和预测,按药物类别、给药途径、地区和竞争格局划分,2020-2030年预测

异位性皮肤炎药物市场-全球产业规模、份额、趋势、机会和预测,按药物类别、给药途径、地区和竞争格局划分,2020-2030年预测 犬异位性皮肤炎市场报告(按药物类别、给药途径、配销通路和地区划分)2025-2033

犬异位性皮肤炎市场报告(按药物类别、给药途径、配销通路和地区划分)2025-2033