|

市场调查报告书

商品编码

1998828

2026 年至 2035 年汽车碰撞测试碰撞测试人偶的市场机会、成长要素、产业趋势分析与预测。Automotive Crash Test Dummies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

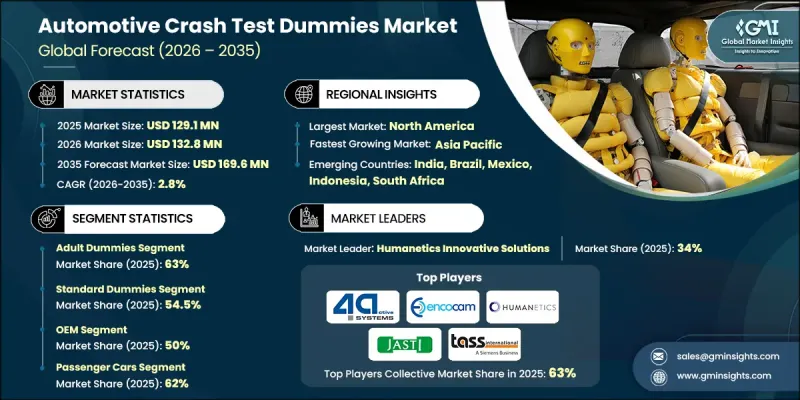

全球汽车碰撞测试碰撞测试人偶市场预计到 2025 年将价值 1.291 亿美元,预计到 2035 年将以 2.8% 的复合年增长率增长至 1.696 亿美元。

汽车碰撞测试碰撞测试人偶市场的成长与全球汽车产量的持续扩张密切相关,这导致所有新车型对安全检验和一致性测试的需求不断增长。随着汽车製造商推出改进的车辆设计并整合新的安全技术,对详细碰撞模拟和安全性能评估的需求持续上升。此外,随着多个地区的监管机构收紧车辆安全标准,製造商被敦促进行广泛的碰撞测试,以确保符合不断变化的指导方针。随着对乘员保护和汽车安全技术创新的日益重视,碰撞测试碰撞测试人偶在汽车研发专案中的重要性进一步提升。此外,动态力学建模和测量能力的进步使工程师能够获得更准确的碰撞场景中人员受伤风险数据。这些进步持续支撑着对先进碰撞测试工具的长期需求,汽车碰撞测试碰撞测试人偶市场正在成为更广泛的汽车安全生态系统中不可或缺的重要组成部分。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 1.291亿美元 |

| 预测金额 | 1.696亿美元 |

| 复合年增长率 | 2.8% |

在汽车产业,人们越来越重视提升对不同体型乘员的保护,这导致对能够模拟各种人体结构的专用碰撞测试碰撞测试人偶的需求日益增长。现代碰撞测试人偶系统变得更加精密和复杂,更高的生物逼真度使工程师能够在模拟碰撞过程中收集到关于潜在损伤的极其精确的数据。先进感测器技术的整合使碰撞测试碰撞测试人偶能够在测试过程中记录更广泛的力、运动和衝击响应测量数据。随着碰撞模拟变得越来越复杂,这些先进的碰撞测试人偶正在帮助工程师更深入地了解车辆的安全性能,并据此改进安全设计。

成人碰撞测试碰撞测试人偶市场占据63%的市场份额,预计2026年至2035年将以1.6%的复合年增长率成长。成人碰撞测试人偶广泛应用于车辆碰撞模拟,以评估乘员在多种碰撞场景(包括正面碰撞、侧面碰撞和追撞)中的安全性。这些碰撞测试人偶旨在复製典型成年人的体型结构,并配备测量系统,用于追踪身体多个关键部位的潜在损伤。从这些模拟中收集的数据对于制定全球车辆安全标准和指南改进型安全系统的开发至关重要。由于成年人的体型结构代表了实际车辆乘员的绝大多数,因此这些碰撞测试人偶仍然是全球汽车安全测试计画中不可或缺的一部分。

预计到2025年,标准碰撞测试人偶市占率将达到54.5%,并在2026年至2035年间以1.7%的复合年增长率成长。标准碰撞测试碰撞测试人偶是通用模型,主要用于法规遵循测试和车辆安全性的基准评估。这些模型通常采用简化的机械结构,模拟碰撞过程中人体的移动。虽然与更先进的模型相比,它们的电子元件较少,但由于其易于获取且经济高效,因此在许多测试项目中仍然发挥着重要作用。汽车製造商经常在常规安全检验程序和实验室测试活动中使用标准碰撞测试人偶,尤其是在不需要收集高度详细资料的情况下。

受严格的车辆安全法规和汽车测试标准的不断进步的推动,美国汽车碰撞测试碰撞测试人偶市场预计在2025年将达到3870万美元。联邦安全指南要求製造商在车辆认证过程中进行全面的碰撞评估,这持续推动对标准化碰撞测试设备的需求。美国汽车製造商和独立测试实验室定期进行详细的碰撞模拟,以确保车辆符合既定的安全标准。随着安全评估项目的不断发展和测试通讯协定的日益完善,研究机构正在逐步升级其设施,以适应新的碰撞测试碰撞测试人偶技术。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 严格的汽车安全法规

- 全球汽车产量增加

- 人们越来越关注儿童和行人的安全问题

- 扩大高级碰撞测试人偶的使用范围

- 产业潜在风险与挑战

- 先进碰撞测试碰撞测试人偶高成本

- 漫长的更新和调整週期

- 市场机会

- 新兴市场安全法规的扩展

- 建立代表女性和老年人的碰撞测试人偶变量

- 电动车和自动驾驶汽车测试的成长

- 智慧数据采集系统的进展

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国国家公路交通安全管理局(NHTSA)

- 美国公路安全保险协会(IIHS)

- 欧洲

- 欧洲新车安全评鑑协会(Euro NCAP)

- 联合国欧洲经济委员会规章(R94、R95、R129)

- 亚太地区

- 日本汽车研究所(JARI)/JIS标准

- 中国汽车技术研究中心(CATARC)/中国新车安全评估协会(C-NCAP)

- 拉丁美洲

- 拉丁美洲 NCAP

- ABNT NBR/国家汽车安全指南

- 中东和非洲

- ESMA车辆安全标准(阿联酋)

- 南非汽车安全标准 (SABS)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析(基于初步调查)

- 对过去价格趋势的分析

- 按业务类型分類的定价策略(溢价/价值/成本加成)

- 成本細項分析

- 专利分析(基于初步研究)

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- 按细分市场分類的生成式人工智慧用例和部署蓝图

- 风险、局限性和监管考量

- 生产能力和生产趋势(基于初步调查)

- 按地区和主要生产商分類的设备产能

- 运转率和扩张计划

- 贸易数据分析(基于付费资料库)

- 进出口量及进口额趋势

- 主要贸易走廊及关税的影响

- 预测假设和情境分析(基于初步研究)

- 基本案例-驱动复合年增长率的关键宏观经济与产业变量

- 乐观情境-宏观经济与产业的顺风

- 悲观情景-宏观经济放缓或产业逆风

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

- 企业级分层基准测试

- 层级分类标准与选择标准

- 按收入、地区和创新能力分類的层级定位矩阵。

第五章 市场估算与预测:Dummy Inc.,2022-2035年

- 成人碰撞测试人偶

- 成年男性碰撞测试人偶

- 成年女性用碰撞测试人偶

- 婴儿和幼儿安抚奶嘴

- 适用于一岁以下婴儿的安抚奶嘴

- 6岁儿童碰撞测试人偶

- 3岁儿童碰撞测试人偶

- 婴儿安抚奶嘴

- 适用于8个月大婴儿的安抚奶嘴

- 适用于2个月大婴儿的安抚奶嘴

- 新生儿安抚奶嘴

第六章 市场估计与预测:依技术划分,2022-2035年

- 标准假人

- 配备高级功能/感测器的碰撞测试人偶

- 混合型碰撞测试人偶

第七章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- LCV

- MCV

- 重型车辆(HCV)

第八章 市场估算与预测:依最终用途划分,2022-2035年

- OEM(目的地设备製造商)

- 汽车零件供应商和测试实验室

- 政府和监管机构

- 独立安全组织/研究机构

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 波兰

- 罗马尼亚

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 越南

- 印尼

- 菲律宾

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- 4activeSystems

- Autoliv

- Cellbond

- CTS

- HORIBA MIRA

- Humanetics Innovative Solutions

- JASTI

- Kistler

- MGA Research

- TASS International

- 当地公司

- Calspan

- Crashtest-Service.com

- DEKRA

- Denton

- Diversified Technical Systems(DTS)

- Dynamic Research

- Transportation Research Center(TRC)

- 新兴企业

- AB Dynamics

- FUTEK Advanced Sensor Technology

- Hunan Safe Automobile Technology

The Global Automotive Crash Test Dummies Market was valued at USD 129.1 million in 2025 and is estimated to grow at a CAGR of 2.8% to reach USD 169.6 million by 2035.

Growth in the automotive crash test dummies market is closely linked to the continued expansion of global vehicle manufacturing, which increases the need for safety validation and compliance testing across new vehicle models. As automakers introduce updated vehicle designs and integrate new safety technologies, the requirement for detailed crash simulations and safety performance assessments continues to rise. Regulatory bodies across several regions have also strengthened vehicle safety standards, encouraging manufacturers to perform extensive crash testing to ensure compliance with evolving guidelines. The increasing emphasis on occupant protection and vehicle safety innovation is reinforcing the importance of crash test dummies in automotive research and development programs. In addition, improvements in biomechanical modeling and measurement capabilities are enabling engineers to capture more accurate data related to human injury risk during crash scenarios. These developments continue to support the long-term demand for advanced crash testing tools, positioning the automotive crash test dummies market as a critical component within the broader automotive safety ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $129.1 Million |

| Forecast Value | $169.6 Million |

| CAGR | 2.8% |

The automotive industry has placed greater attention on improving protection for occupants with varying physical characteristics, which has increased demand for specialized crash test dummies designed to represent different body structures. Modern dummy systems are becoming significantly more advanced, offering improved bio-fidelity that enables engineers to collect highly precise data regarding potential injuries during simulated collisions. The integration of enhanced sensor technologies has allowed crash test dummies to record a wider range of measurements related to force, motion, and impact response during testing procedures. As crash simulations become more complex, these advanced dummies help engineers better understand vehicle safety performance and refine safety designs accordingly.

The adult crash test dummies segment held 63% share and is expected to grow at a CAGR of 1.6% between 2026 and 2035. Adult dummies are widely used in vehicle crash simulations to evaluate occupant safety across multiple collision scenarios involving the front, side, and rear of a vehicle. These dummies are designed to replicate the physical characteristics of typical adult body structures and are equipped with measurement systems that track potential injuries across several critical areas of the body. Data collected from these simulations plays an essential role in establishing global vehicle safety benchmarks and guiding the development of improved safety systems. Because adult body structures represent a significant portion of real-world vehicle occupants, these dummies remain fundamental to automotive safety testing programs worldwide.

The standard dummies segment accounted for 54.5% share in 2025 and is anticipated to grow at a CAGR of 1.7% from 2026 to 2035. Standard crash test dummies are designed as general-purpose models used primarily in regulatory compliance testing and baseline vehicle safety evaluations. These models typically feature simplified mechanical structures that replicate human body movement during collision events. Although they incorporate limited electronic instrumentation compared to advanced models, they continue to play a crucial role in many testing programs due to their accessibility and cost efficiency. Automotive manufacturers frequently utilize standard dummies for routine safety validation procedures and laboratory testing activities where extremely detailed data collection is not required.

United States Automotive Crash Test Dummies Market reached USD 38.7 million in 2025, supported by strict vehicle safety regulations and ongoing advancements in automotive testing standards. Federal safety guidelines require manufacturers to conduct comprehensive crash evaluations as part of vehicle certification processes, which continues to drive demand for standardized crash test equipment. Automotive manufacturers and independent testing organizations in the United States regularly perform detailed crash simulations to ensure that vehicles meet established safety benchmarks. As safety evaluation programs evolve and testing protocols become more sophisticated, research laboratories are gradually upgrading their facilities to accommodate newer crash test dummy technologies.

Key companies operating in the Global Automotive Crash Test Dummies Market include Humanetics Innovative Solutions, Kistler, Cellbond (Encocam), MGA Research, Dynamic Research, CTS, 4activeSystems, JASTI, and TASS (Siemens). Companies active in the Global Automotive Crash Test Dummies Market are focusing on multiple strategic initiatives to strengthen their competitive position and expand their technological capabilities. Significant investments are being directed toward research and development to improve dummy biofidelity and enhance the accuracy of injury measurement systems. Manufacturers are also incorporating advanced sensor technologies and data acquisition systems to provide more detailed insights into crash dynamics. Strategic collaborations with automotive manufacturers, safety laboratories, and regulatory institutions are helping companies develop testing solutions aligned with evolving safety standards. Expanding product portfolios to include next-generation dummy platforms designed for complex crash simulations is another key strategy.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Dummy

- 2.2.3 Technology

- 2.2.4 Vehicle

- 2.2.5 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent vehicle safety regulations

- 3.2.1.2 Rising vehicle production globally

- 3.2.1.3 Increasing focus on child & pedestrian safety

- 3.2.1.4 Growing adoption of advanced dummies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced crash test dummies

- 3.2.2.2 Long replacement & calibration cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market safety regulation expansion

- 3.2.3.2 Development of female and elderly representative dummies

- 3.2.3.3 Growth in electric & autonomous vehicle testing

- 3.2.3.4 Advancements in smart data acquisition systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Insurance Institute for Highway Safety (IIHS)

- 3.4.2 Europe

- 3.4.2.1 Euro NCAP (European New Car Assessment Programme)

- 3.4.2.2 UNECE Regulations (R94, R95, R129)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automobile Research Institute (JARI) / JIS Standards

- 3.4.3.2 China Automotive Technology & Research Center (CATARC) / Chinese NCAP (C-NCAP)

- 3.4.4 Latin America

- 3.4.4.1 Latin NCAP

- 3.4.4.2 ABNT NBR / National Automotive Safety Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA Vehicle Safety Standards (UAE)

- 3.4.5.2 SABS Automotive Safety Standards (South Africa)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by primary research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by primary research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Trade data analysis (Driven by paid database)

- 3.14.1 Import/export volume & value trends

- 3.14.2 Key trade corridors & tariff impact

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Dummy, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Adult dummies

- 5.2.1 Male adult dummies

- 5.2.2 Female adult dummies

- 5.3 Child dummies

- 5.3.1 0-year-old child dummies

- 5.3.2 6-year-old child dummies

- 5.3.3 3-year-old child dummies

- 5.4 Infant dummies

- 5.4.1 8-month infant dummies

- 5.4.2 2-month infant dummies

- 5.4.3 newborn dummies

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Standard dummies

- 6.3 Advanced / sensor-equipped dummies

- 6.4 Hybrid dummies

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Original Equipment Manufacturers (OEMs)

- 8.3 Automotive suppliers & testing labs

- 8.4 Government / regulatory bodies

- 8.5 Independent safety organizations / research institutions

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 4activeSystems

- 10.1.2 Autoliv

- 10.1.3 Cellbond

- 10.1.4 CTS

- 10.1.5 HORIBA MIRA

- 10.1.6 Humanetics Innovative Solutions

- 10.1.7 JASTI

- 10.1.8 Kistler

- 10.1.9 MGA Research

- 10.1.10 TASS International

- 10.2 Regional players

- 10.2.1 Calspan

- 10.2.2 Crashtest-Service.com

- 10.2.3 DEKRA

- 10.2.4 Denton

- 10.2.5 Diversified Technical Systems (DTS)

- 10.2.6 Dynamic Research

- 10.2.7 Transportation Research Center (TRC)

- 10.3 Emerging players

- 10.3.1 AB Dynamics

- 10.3.2 FUTEK Advanced Sensor Technology

- 10.3.3 Hunan Safe Automobile Technology