|

市场调查报告书

商品编码

1998834

运动医学市场机会、成长要素、产业趋势分析及2026-2035年预测Sports Medicine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

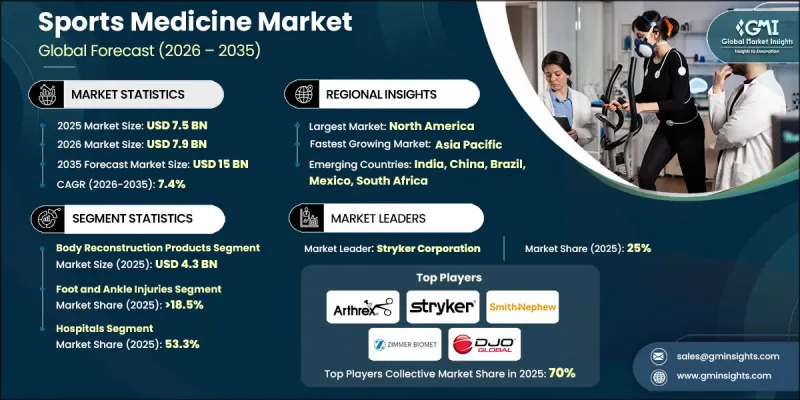

全球运动医学市场预计到 2025 年将价值 75 亿美元,预计到 2035 年将以 7.4% 的复合年增长率增长至 150 亿美元。

受全球运动伤害率上升以及植入、穿戴式装置和微创手术等技术进步的推动,运动医学市场正在蓬勃发展。由于关节镜手术和其他微创技术相比传统手术具有许多优势,例如恢復更快、疼痛更轻、併发症率更低,因此医疗专业人员正越来越多地采用这些技术。运动医学涵盖旨在预防、诊断和治疗运动相关伤害的产品和服务,包括医疗设备、植入、復健设备和运动表现监测工具。此外,运动参与度的提高、健身意识的增强以及损伤管理技术的创新也进一步推动了该市场的发展。采用生物相容性材料、3D列印和智慧涂层的先进植入能够加速癒合,同时最大限度地降低感染风险。感测器和智慧手环等穿戴式装置能够即时监测肌肉活动、动态和压力水平,从而支持个人化治疗并改善康復效果。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 75亿美元 |

| 预计金额 | 150亿美元 |

| 复合年增长率 | 7.4% |

预计2025年,人体重组产品市场规模将达43亿美元。这些产品包括用于修復、替换或重组运动伤害后受损的骨骼、关节和组织的医疗设备和生物製药。它们在恢復活动能力、稳定性和功能方面发挥着至关重要的作用,使运动员能够更快地重返赛场。运动相关损伤数量的增加以及对先进治疗方法日益增长的需求正在推动人体重组产品的普及。诸如3D列印植入、生物可吸收材料和再生医学生物製剂等创新技术正在改善手术效果、缩短恢復时间并提高患者满意度。

到2025年,足踝损伤市场将占市场份额的18.5%。这些部位的损伤包括骨折、扭伤、断裂和应力性骨折,这些损伤会对活动能力和运动表现产生显着影响。高强度运动、过度使用和穿着不合适的鞋子是导致这些伤害的主要因素。随着患者和医疗专业人员越来越重视早期疗育和有效的復健策略,损伤预防、诊断和復健技术的不断进步正在推动该细分市场的成长。

到2025年,北美运动医学市占率将达到36.4%。该地区市场成长的驱动力包括先进的医疗基础设施、技术创新以及日益增长的体育参与。青少年和成人中骨折、韧带断裂、脑震盪和过度使用综合症等损伤发生率的上升,使得先进治疗方法、復健服务和预防医学的需求强劲。该地区受益于完善的医疗设施、技术精湛的医护人员以及旨在推广安全运动的宣传活动。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 全球运动伤害病例呈上升趋势。

- 植入和穿戴式装置的技术进步

- 对微创手术的需求日益增长,以及运动医学中心的增加。

- 人们对身体健康和体育活动的认识不断提高

- 产业潜在风险与挑战

- 开发中国家训练有素的医护人员短缺

- 运动医学费用高昂

- 市场机会

- 远端医疗和远距復健服务的发展将使混合护理模式成为可能。

- 促进因素

- 成长潜力分析

- 监理情势

- 技术进步

- 当前技术趋势

- 新兴技术

- 2025年价格分析

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

- 人工智慧和生成式人工智慧对市场的影响

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 身体重组产品

- 整形外科植入

- 骨折和韧带修復产品

- 关节镜设备

- 软组织修復产品

- 义肢

- 正交生物製品

- 身体支持和恢復

- 矫正器具和支架

- 压力衣

- 物理治疗设备

- 热疗

- 电刺激

- 其他实体支撑和恢復产品

- 配件

- 绷带

- 磁带

- 消毒剂

- 裹

- 其他配件

- 其他产品

第六章 市场估计与预测:依伤害类型划分,2022-2035年

- 膝伤

- 肩部受伤

- 足部和踝部损伤

- 背部和脊椎损伤

- 髋部和鼠蹊部损伤

- 其他损害

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 物理治疗中心

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- Stryker

- Arthrex, Inc.

- Wright Medical Technology

- Otto Bock Healthcare

- Zimmer Biomet

- Smith &Nephew Plc

- Breg, Inc.

- Muller Sports, Inc.

- RTI Surgical

- Performance Health International Limited

- KARL STORZ

- Bauerfeind AG

- CONMED Corporation

- Johnson &Johnson

- Ossur Corporate

- Creamer Product, Inc.

- DJO Global

- Anika Therapeutics, Inc.

The Global Sports Medicine Market was valued at USD 7.5 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 15 billion by 2035.

The market's growth is fueled by the rising prevalence of sports injuries worldwide, coupled with technological advancements in implants, wearable devices, and minimally invasive surgical procedures. Healthcare providers are increasingly adopting arthroscopic and other minimally invasive techniques due to their advantages, including faster recovery, reduced pain, and lower complication rates compared to traditional surgeries. Sports medicine encompasses products and services designed to prevent, diagnose, and treat sports-related injuries, including medical devices, implants, rehabilitation equipment, and performance monitoring tools. The market is further driven by growing sports participation, heightened fitness awareness, and innovations in injury management technologies. Advanced implants using biocompatible materials, 3D printing, and smart coatings accelerate healing while minimizing infection risks. Wearable devices such as sensors and smart bands provide real-time monitoring of muscle activity, biomechanics, and stress levels, supporting personalized treatment and enhanced recovery outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.5 Billion |

| Forecast Value | $15 Billion |

| CAGR | 7.4% |

The body reconstruction products segment generated USD 4.3 billion in 2025. These products include medical devices and biologics designed to repair, replace, or reconstruct damaged bones, joints, and tissues following sports injuries. They play a vital role in restoring mobility, stability, and functionality, enabling athletes to return to their activities faster. Growing sports-related injuries and demand for advanced treatment options drive the adoption of body reconstruction products. Innovations like 3D-printed implants, bioresorbable materials, and regenerative biologics enhance surgical outcomes, reduce recovery time, and improve patient satisfaction.

The foot and ankle injuries segment generated 18.5% share in 2025. Injuries in these areas include fractures, sprains, tendon tears, and stress fractures, which significantly impact mobility and athletic performance. High-impact activities, overuse, and improper footwear contribute to their prevalence. Continuous advancements in injury prevention, diagnostics, and rehabilitation technologies support market growth in this segment, as patients and healthcare providers prioritize early intervention and effective recovery strategies.

North America Sports Medicine Market held a 36.4% share in 2025. Market growth in the region is driven by advanced healthcare infrastructure, technological innovation, and rising sports participation. Increasing incidences of injuries such as fractures, ligament tears, concussions, and overuse conditions among youth and adults have created a strong demand for advanced treatment options, rehabilitation services, and preventive care. The region benefits from a combination of highly equipped medical facilities, skilled healthcare professionals, and awareness campaigns promoting safe athletic practices.

Key companies operating in the Global Sports Medicine Market include Wright Medical Technology, DJO Global, Arthrex, Inc., Johnson & Johnson, Performance Health International Limited, Zimmer Biomet, Stryker, CONMED Corporation, Anika Therapeutics, Inc., Otto Bock Healthcare, Smith & Nephew Plc, Muller Sports, Inc., Creamer Product, Inc., KARL STORZ, Breg, Inc., and Bauerfeind AG. Companies in the Sports Medicine Market are expanding their presence by investing in research and development of innovative implants, wearable devices, and regenerative biologics. Manufacturers are forming strategic partnerships with hospitals, clinics, and sports organizations to integrate products into treatment and rehabilitation programs. Geographic expansion into emerging markets allows access to a growing base of athletes and recreational participants. Firms are also focusing on minimally invasive solutions to improve recovery outcomes and patient satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Injury type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of sports injuries globally

- 3.2.1.2 Technological advancements in implants and wearable devices

- 3.2.1.3 Growing demand for minimal invasive surgeries and rising number of sports medical centres

- 3.2.1.4 Increasing awareness regarding physical fitness and sports activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of trained healthcare professional in developing countries

- 3.2.2.2 Inflated cost of sports medicine

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in telehealth and remote rehabilitation services, enabling hybrid care models.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2025

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Body reconstruction products

- 5.2.1 Orthopedic implants

- 5.2.2 Fracture and ligament repair products

- 5.2.3 Arthroscopy devices

- 5.2.4 Soft tissue repair products

- 5.2.5 Prosthetics

- 5.2.6 Orthobiologics

- 5.3 Body support & recovery

- 5.3.1 Braces and supports

- 5.3.2 Compression clothing

- 5.3.3 Physiotherapy equipment

- 5.3.4 Thermal therapy

- 5.3.5 Electrostimulation

- 5.3.6 Other body support & recovery products

- 5.4 Accessories

- 5.4.1 Bandages

- 5.4.2 Tapes

- 5.4.3 Disinfectants

- 5.4.4 Wraps

- 5.4.5 Other accessories

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Injury Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Knee injuries

- 6.3 Shoulder injuries

- 6.4 Foot and ankle injuries

- 6.5 Back and spine injuries

- 6.6 Hip and groin injuries

- 6.7 Other injuries

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Physiotherapy centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Stryker

- 9.2 Arthrex, Inc.

- 9.3 Wright Medical Technology

- 9.4 Otto Bock Healthcare

- 9.5 Zimmer Biomet

- 9.6 Smith & Nephew Plc

- 9.7 Breg, Inc.

- 9.8 Muller Sports, Inc.

- 9.9 RTI Surgical

- 9.10 Performance Health International Limited

- 9.11 KARL STORZ

- 9.12 Bauerfeind AG

- 9.13 CONMED Corporation

- 9.14 Johnson & Johnson

- 9.15 Ossur Corporate

- 9.16 Creamer Product, Inc.

- 9.17 DJO Global

- 9.18 Anika Therapeutics, Inc.

2026年全球运动医学市场报告

2026年全球运动医学市场报告 日本运动医学市场规模、份额、趋势和预测:按产品、应用、最终用户和地区划分,2026-2034年运动医学市场规模、份额、趋势及预测(按产品、应用、最终用户及地区划分),2026-2034年

日本运动医学市场规模、份额、趋势和预测:按产品、应用、最终用户和地区划分,2026-2034年运动医学市场规模、份额、趋势及预测(按产品、应用、最终用户及地区划分),2026-2034年 运动医学市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年

运动医学市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年 运动医学市场:2025-2030 年预测

运动医学市场:2025-2030 年预测 运动医学市场规模、份额、趋势分析报告:按产品类型、应用、地区、细分市场预测,2025-2033 年

运动医学市场规模、份额、趋势分析报告:按产品类型、应用、地区、细分市场预测,2025-2033 年 运动医学市场评估:设备类型·用途·终端用户·各地区的机会及预测 (2018-2032年)

运动医学市场评估:设备类型·用途·终端用户·各地区的机会及预测 (2018-2032年) 运动医学市场规模、份额、成长分析、按产品、按应用、按最终用户、按地区 - 按行业预测,2024-2031 年

运动医学市场规模、份额、成长分析、按产品、按应用、按最终用户、按地区 - 按行业预测,2024-2031 年 运动医学市场,规模,占有率,趋势,产业分析报告:各产品类型,各用途,各最终用途,各地区,市场预测

运动医学市场,规模,占有率,趋势,产业分析报告:各产品类型,各用途,各最终用途,各地区,市场预测 全球运动医学市场:按产品、应用和最终用户 - 预测(~2029 年)

全球运动医学市场:按产品、应用和最终用户 - 预测(~2029 年)