|

市场调查报告书

商品编码

1998835

2026 年至 2035 年病患监测设备的市场机会、成长要素、产业趋势与预测。Patient Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

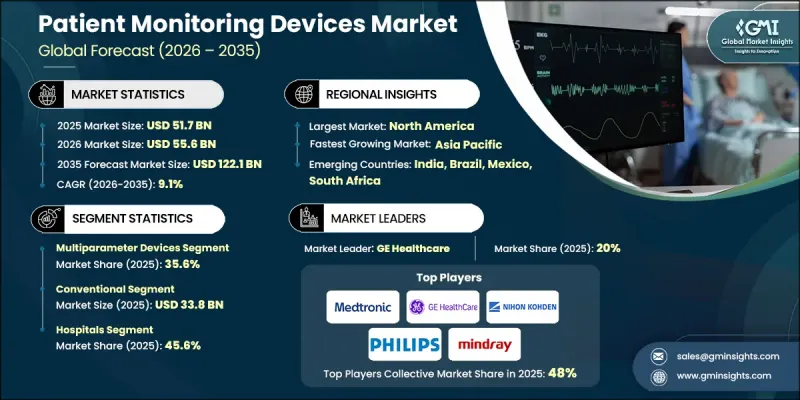

2025年全球病患监测设备市场价值为517亿美元,预计到2035年将以9.1%的复合年增长率增长至1221亿美元。

受慢性病患病率上升、人口老化、技术进步以及新兴经济体医疗保健支出增加等因素的推动,该市场正经历强劲增长。随着人口老化,需要持续监测的心血管、呼吸系统和代谢性疾病发生率不断上升,推动了市场需求。病患监测设备的创新,特别是物联网和人工智慧技术的融合,实现了即时健康数据收集、预测分析和自动化决策。这些进步使临床医生能够及早发现风险并提供个人化护理。现代设备具备无线连接、云端资料管理、模组化设计和更佳的便携性,提高了重症监护、手术和居家照护等场景的工作流程效率。先进的监视器即使在恶劣环境下也能提供可靠的测量数据,帮助医疗专业人员更快、更准确地做出临床决策,进而改善全球患者的治疗效果。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 517亿美元 |

| 预测金额 | 1221亿美元 |

| 复合年增长率 | 9.1% |

预计到2025年,多参数监视器市场规模将达到184亿美元,占整个市场的35.6%。多参数监视器可同时监测多项生命征象,并将资料整合到单一平台上。它们广泛应用于重症监护室、手术室和急诊医疗环境,提供可自订的配置、高解析度显示器和模组化设计,以实现以患者为中心的监护。

预计2025年,传统床边监护设备市场规模将达338亿美元。传统床边监护设备是固定式设备,用于追踪心率、血压、血氧饱和度和体温等关键生理参数。这些设备已成为医院的标准配置,用于在重症监护室、普通病房和手术室进行持续监测,从而可靠地评估基本生命征象。

预计到2025年,美国病患监测设备市场规模将达到202亿美元,主要驱动因素是需要持续监测的慢性疾病(例如心血管疾病和呼吸系统疾病)盛行率的不断上升。美国先进的医疗基础设施、庞大的手术量以及对数位医疗解决方案的投资,进一步加速了市场成长,推动了从传统监视器向具有集中式监护功能和电子健康记录(EHR)兼容性的整合无线系统的转变。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 慢性病盛行率增加

- 新兴经济体可支配收入和医疗保健支出不断增长

- 病患监测设备的技术进步

- 老年人口增加

- 产业潜在风险与挑战

- 设备高成本

- 严格的法规环境

- 市场机会

- 扩大人工智慧驱动的预测性监测工具的应用

- 促进因素

- 成长潜力分析

- 监理情势(基于初步调查)

- 北美洲

- 欧洲

- 亚太地区

- 技术进步

- 当前技术趋势

- 新兴技术

- 未来市场趋势

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 心臟监测设备

- 心电图仪

- 植物型循环记录器

- 携带式心电遥测监视器

- 智慧型穿戴式心电图贴片

- 神经监测设备

- 脑电图(EEG)测量设备

- 脑氧饱和度监测仪

- 颅内压监测器

- 肌电图(EMG)设备

- 呼吸监测设备

- 脉搏血氧饱和度分析仪

- 肺计量计

- 二氧化碳测量仪

- 峰值流量计

- 麻醉监控器

- 血流动力学监测装置

- 胎儿和新生儿监护

- 多参数监视器

- 其他产品

第六章 市场估计与预测:依类型划分,2022-2035年

- 传统的

- 无线的

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 居家医疗设施

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- Becton Dickinson and Company

- Biotronik

- EPSIMED

- Fukuda Denshi

- GE Healthcare

- HILLROM & WELCH ALLYN

- Koninklijke Philips

- Medion

- Medtronic

- Natus Medical

- Nihon Kohden Corporation

- OMRON Corporation

- OSI Systems

- Shenzhen Mindray Bio-Medical Electronics

- Skanray Technologies

The Global Patient Monitoring Devices Market was valued at USD 51.7 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 122.1 billion by 2035.

The market is witnessing strong expansion owing to the rising prevalence of chronic diseases, increasing geriatric populations, technological advancements, and higher healthcare spending in emerging economies. Aging demographics are driving demand, as older populations face a growing incidence of cardiovascular, respiratory, and metabolic conditions that require continuous monitoring. Innovations in patient monitoring devices, particularly the integration of IoT and AI technologies, allow real-time health data collection, predictive analytics, and automated decision-making. These advancements enable clinicians to detect risks early and deliver personalized care. Modern devices now offer wireless connectivity, cloud-based data management, modular designs, and improved portability, enhancing workflow efficiency in critical care, surgical, and home care settings. Advanced monitors provide reliable measurements even under challenging conditions, helping healthcare professionals make faster, accurate clinical decisions while improving patient outcomes globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $51.7 Billion |

| Forecast Value | $122.1 Billion |

| CAGR | 9.1% |

The multiparameter devices segment reached USD 18.4 billion in 2025, representing 35.6%. Multiparameter monitors track multiple vital signs simultaneously, consolidating data on a single platform. They are widely used in ICUs, operating rooms, and emergency care settings, offering customizable settings, high-resolution displays, and modular configurations for tailored patient monitoring.

The conventional segment accounted for USD 33.8 billion in 2025. Conventional bedside monitoring devices are stationary units that track core physiological parameters such as heart rate, blood pressure, oxygen saturation, and temperature. These devices are standard in hospitals for continuous monitoring in ICUs, general wards, and operating rooms, offering reliable and basic vital sign assessment.

U.S. Patient Monitoring Devices Market reached USD 20.2 billion in 2025, driven by the rising prevalence of chronic illnesses, including cardiovascular and respiratory diseases, which necessitate ongoing monitoring. The country's advanced healthcare infrastructure, high surgical volumes, and investment in digital health solutions support the transition from conventional monitors to integrated, wireless systems with centralized monitoring and EHR compatibility, further accelerating market growth.

Key players in the Global Patient Monitoring Devices Market include Medtronic, Koninklijke Philips, GE Healthcare, Fukuda Denshi, Becton Dickinson and Company, Nihon Kohden Corporation, HILLROM & WELCH ALLYN, OSI Systems, Shenzhen Mindray Bio-Medical Electronics, Skanray Technologies, Medion, EPSIMED, Natus Medical, and Cerba Healthcare. Companies in the Global Patient Monitoring Devices Market are focusing on several strategies to strengthen their market presence. They are investing in AI, IoT, and wireless technologies to develop advanced, real-time monitoring solutions. Partnerships with hospitals, healthcare providers, and research institutions help in co-developing devices that meet clinical needs. Expanding distribution networks, enhancing after-sales services, and offering cloud-based data management platforms ensure customer retention. Firms are also focusing on modular, portable, and cost-effective solutions for homecare and remote monitoring. Continuous innovation in multiparameter and wearable devices, along with compliance with regulatory standards, helps maintain competitive advantage and expand global market share.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.2 Research transparency addendum

- 1.7.3 Source attribution framework

- 1.7.4 Quality assurance metrics

- 1.7.1 Quantified market impact analysis

- 1.8 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing disposable income and healthcare expenditure in emerging countries

- 3.2.1.3 Technological advancement in patient monitoring devices

- 3.2.1.4 Growing geriatric population base

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption for AI-powered predictive monitoring tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiac monitoring devices

- 5.2.1 ECG devices

- 5.2.2 Implantable loop recorders

- 5.2.3 Mobile cardiac telemetry monitors

- 5.2.4 Smart wearable ECG patches

- 5.3 Neuromonitoring devices

- 5.3.1 EEG devices

- 5.3.2 Cerebral oximeters

- 5.3.3 Intracranial pressure monitors

- 5.3.4 EMG devices

- 5.4 Respiratory monitoring devices

- 5.4.1 Pulse oximeters

- 5.4.2 Spirometers

- 5.4.3 Capnographs

- 5.4.4 Peak flow meters

- 5.5 Anesthesia monitor

- 5.6 Hemodynamic monitoring devices

- 5.7 Fetal and neonatal monitoring

- 5.8 Multiparameter devices

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Wireless

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Becton Dickinson and Company

- 9.2 Biotronik

- 9.3 EPSIMED

- 9.4 Fukuda Denshi

- 9.5 GE Healthcare

- 9.6 HILLROM & WELCH ALLYN

- 9.7 Koninklijke Philips

- 9.8 Medion

- 9.9 Medtronic

- 9.10 Natus Medical

- 9.11 Nihon Kohden Corporation

- 9.12 OMRON Corporation

- 9.13 OSI Systems

- 9.14 Shenzhen Mindray Bio-Medical Electronics

- 9.15 Skanray Technologies

病患监测设备市场:2026-2032年全球市场预测(按产品类型、技术、连接方式、应用、最终用户和部署模式划分)

病患监测设备市场:2026-2032年全球市场预测(按产品类型、技术、连接方式、应用、最终用户和部署模式划分) 2026年全球植入式远端患者监护设备市场报告2026年全球病患监测设备市场报告2026年全球远端患者监护贴片市场报告

2026年全球植入式远端患者监护设备市场报告2026年全球病患监测设备市场报告2026年全球远端患者监护贴片市场报告 日本患者照护监护设备市场:依产品类型、监护参数、最终用户、模式和病患小组

日本患者照护监护设备市场:依产品类型、监护参数、最终用户、模式和病患小组 全球病患监测设备市场规模、份额、趋势和成长分析报告(2026-2034年)24小时动态血压监测仪市场按产品类型、分销管道、应用和最终用户划分,全球预测(2026-2032年)床边监视器和集中式监护系统市场按产品类型、参数类型、技术、连接方式、性别、最终用户和应用划分-2026-2032年全球预测经皮皮氧分压 (PO2) 和二氧化碳分压 (PCO2) 监测仪市场按产品类型、便携性、安装方式和最终用户划分 - 全球预测 2026-2032 年

全球病患监测设备市场规模、份额、趋势和成长分析报告(2026-2034年)24小时动态血压监测仪市场按产品类型、分销管道、应用和最终用户划分,全球预测(2026-2032年)床边监视器和集中式监护系统市场按产品类型、参数类型、技术、连接方式、性别、最终用户和应用划分-2026-2032年全球预测经皮皮氧分压 (PO2) 和二氧化碳分压 (PCO2) 监测仪市场按产品类型、便携性、安装方式和最终用户划分 - 全球预测 2026-2032 年 日本病患照护监护设备市场报告(按设备类型、应用、最终用户和地区划分,2026-2034年)

日本病患照护监护设备市场报告(按设备类型、应用、最终用户和地区划分,2026-2034年)