|

市场调查报告书

商品编码

1998841

工业雷射系统市场机会、成长要素、产业趋势分析及2026-2035年预测Industrial Laser Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

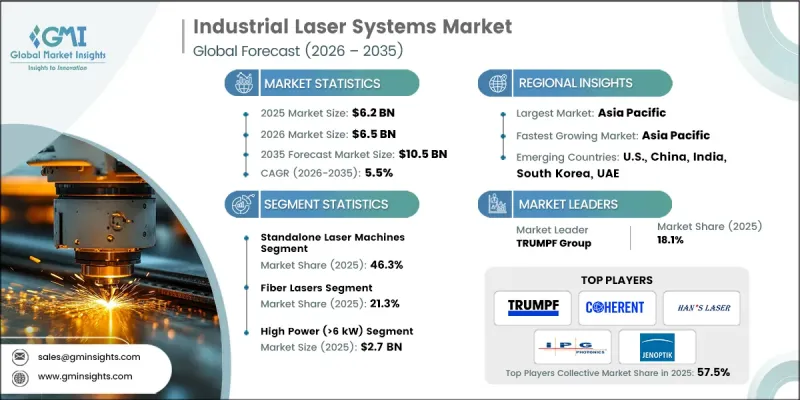

全球工业雷射系统市场预计到 2025 年将达到 62 亿美元,年复合成长率为 5.5%,到 2035 年将达到 105 亿美元。

雷射技术在精密製造领域的日益普及,尤其是在对精度和效率要求极高的高附加价值应用领域,是推动该市场成长的主要动力。电动汽车电池生产中对雷射焊接的需求不断增长,电子製造中对雷射打标的需求不断增长,半导体微型化所需的超快雷射微加工技术以及航太和工业零件所需的雷射辅助增材製造技术的需求不断增长,这些都促进了行业的扩张。光纤雷射、超快雷射和机器人整合等技术的进步,使製造商能够在提高品质、可靠性和能源效率的同时,缩短生产时间。这些因素,加上对自动化和工业4.0流程的持续投资,正在为多个工业领域创造强劲的成长机会。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 62亿美元 |

| 预测金额 | 105亿美元 |

| 复合年增长率 | 5.5% |

工业雷射系统市场的发展主要受精密雷射焊接需求成长的驱动,尤其是在电池和电子设备製造领域。雷射焊接能够高速连接导电材料,同时最大限度地减少热变形,确保结构完整性并提升电气性能。同时,超快雷射微加工技术在半导体製造领域也备受关注,它能够实现高精度晶圆切割、微孔加工和薄膜结构形成,且不会造成热损伤。雷射增材製造技术也越来越多地应用于结构要求高的复杂航太和工业零件的製造,进一步拓展了高性能雷射的应用范围。雷射系统在精度、速度和自动化方面的融合,促使製造商将先进的雷射解决方案整合到整个生产线中,从而提高产量比率、重复性和营运效率。

预计2026年至2035年间,机器人雷射加工系统市场将以6.6%的复合年增长率成长。这些系统在汽车、航太和重工业等产业需求旺盛,这些产业越来越依赖自动化来提高生产效率和精确度。机器人雷射系统能够减少人工劳动,提高生产一致性,并无缝整合到工业4.0环境中。由于机器人雷射加工系统能够提供连续运行,同时确保结果的准确性和可重复性,因此对于希望在保持品质标准的同时扩大生产规模的製造商而言,这是一项极具吸引力的投资。

受重型材料加工应用的推动,高功率(6kW以上)雷射市场预计到2025年将达到27亿美元。高功率雷射广泛应用于切割厚金属板、製造汽车底盘、造船和钢铁加工等领域。它们能够快速且有效率地切割大面积、高反射率的金属表面,因此在需要可靠金属加工解决方案的产业中不可或缺。高功率雷射的日益普及避免了大规模製造过程中的生产中断,并显着提升了市场份额。

到2025年,北美工业雷射系统市占率将达到27.7%。该地区的成长主要得益于汽车、航太和电子产品製造商对高精度雷射焊接、切割和微加工解决方案的强劲需求。电动车产业的蓬勃发展、半导体生产以及先进金属加工设施的普及,进一步加速了光纤雷射和超快雷射系统的应用。对智慧製造基础设施、机器人技术和工业4.0生产线的投资,正在推动各行各业采用先进雷射技术。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 电动车电池製造领域对高精度雷射焊接的需求

- 需要高精度雷射打标的家用电子电器产品生产。

- 半导体小型化需要超高速雷射微加工技术

- 需要微尺度雷射加工的医疗设备製造。

- 整合雷射加工设备的自动化智慧工厂

- 产业潜在风险与挑战

- 复杂雷射加工工艺熟练操作人员短缺

- 维护高功率工业雷射光源的复杂性。

- 市场机会

- 超快雷射在半导体晶圆加工的应用

- 雷射增材製造在航太零件领域的应用拓展

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与开发

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴竞争对手和Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依雷射类型划分,2022-2035年

- 光纤雷射

- 二氧化碳雷射

- 固体雷射

- 二极体雷射

- 超高速雷射

- 准分子雷射

- 其他的

第六章 市场估算与预测:依材料类型划分,2022-2035年

- 低功率(小于1千瓦)

- 中功率(1-6千瓦)

- 高功率(>6千瓦)

第七章 市场估计与预测:依系统配置划分,2022-2035年

- 独立式雷射加工机

- 机器人雷射加工系统

- 整合生产线系统

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 切割

- 焊接

- 标记和雕刻

- 钻孔

- 其他的

第九章 市场估价与预测:依最终用户划分,2022-2035年

- 车

- 电子设备製造

- 半导体製造

- 航太/国防

- 金属加工及工业製造

- 医疗设备

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- TRUMPF Group

- IPG Photonics Corporation

- Coherent Corp.

- 按地区分類的主要企业

- 北美洲

- Lumentum Holdings Inc.

- nLIGHT, Inc.

- Amada Miyachi America, Inc.

- MKS Instruments, Inc.

- 亚太地区

- Han's Laser Technology Industry Group Co., Ltd.

- Raycus Fiber Laser Technologies Co., Ltd.

- Maxphotonics Co., Ltd.

- Sahajanand Laser Technology Limited

- 欧洲

- Bystronic Laser AG

- Jenoptik AG

- LPKF Laser &Electronics AG

- Toptica Photonics AG

- 北美洲

The Global Industrial Laser Systems Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 10.5 billion in 2035.

The market is propelled by the growing adoption of laser-based technologies in precision manufacturing, particularly for high-value applications that require accuracy and efficiency. Increasing demand for laser welding in electric vehicle battery production, laser marking in electronics manufacturing, ultrafast laser micromachining for semiconductor miniaturization, and laser-assisted additive manufacturing for aerospace and industrial components is driving industry expansion. Technological advances in fiber lasers, ultrafast lasers, and robotic integration allow manufacturers to reduce production times while improving quality, reliability, and energy efficiency. These factors, combined with ongoing investments in automation and Industry 4.0 processes, are creating strong growth opportunities across multiple industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 5.5% |

The industrial laser systems market is particularly fueled by the rising need for precision laser welding in battery and electronics manufacturing. Laser welding enables high-speed joining of conductive materials with minimal thermal distortion, ensuring strong structural integrity and improved electrical performance. Simultaneously, ultrafast laser micromachining is gaining traction in semiconductor manufacturing, enabling highly precise wafer cutting, micro-via drilling, and thin-film structuring without causing heat damage. Laser-based additive manufacturing is also increasingly adopted for producing complex aerospace components and industrial parts with high structural requirements, creating broader applications for high-performance lasers. The convergence of precision, speed, and automation in laser systems is pushing manufacturers to integrate advanced laser solutions across production lines, supporting improved yield, repeatability, and operational efficiency.

The robotic laser processing systems segment is expected to grow at a CAGR of 6.6% during 2026-2035. These systems are highly sought after in sectors like automotive, aerospace, and heavy manufacturing that increasingly rely on automation to enhance productivity and precision. Robotic laser systems reduce manual labor, improve production consistency, and integrate seamlessly into Industry 4.0 environments. The ability to operate continuously while delivering accurate and repeatable results has made robotic laser processing an attractive investment for manufacturers aiming to scale production while maintaining quality standards.

The high-power (>6 kW) segment reached USD 2.7 billion in 2025, driven by heavy-duty material processing applications. High-power lasers are widely deployed in thick metal cutting, automotive chassis manufacturing, shipbuilding, and steel fabrication. Their ability to cut large and reflective metal surfaces with high speed and efficiency makes them indispensable in industries requiring robust metal processing solutions. The growing adoption of these high-output lasers ensures uninterrupted production in large-scale fabrication operations, contributing significantly to the market's revenue share.

North America Industrial Laser Systems Market accounted for 27.7% share in 2025. The region's growth is largely driven by strong demand from automotive, aerospace, and electronics manufacturers, which require high-precision laser welding, cutting, and micromachining solutions. The expanding electric vehicle industry, semiconductor production, and advanced metal fabrication facilities are further accelerating the adoption of fiber and ultrafast laser systems. Investments in smart manufacturing infrastructure, robotics, and Industry 4.0-enabled production lines are enhancing the deployment of advanced laser-based technologies across multiple sectors.

Key companies operating in the Global Industrial Laser Systems Market include Coherent Corp., Han's Laser Technology Industry Group Co., Ltd., IPG Photonics Corporation, Jenoptik AG, Lumentum Holdings Inc., Raycus Fiber Laser Technologies Co., Ltd., Amada Miyachi America, Inc., TRUMPF Group, Toptica Photonics AG, nLIGHT, Inc., LPKF Laser & Electronics AG, Bystronic Laser AG, Sahajanand Laser Technology Limited, Maxphotonics Co., Ltd., and MKS Instruments, Inc. Companies in the Global Industrial Laser Systems Market are implementing strategies to strengthen their market presence and competitive position. Key initiatives include investing heavily in R&D to improve laser power, precision, and efficiency while developing new fiber, ultrafast, and robotic laser solutions tailored to high-demand sectors. Expanding product portfolios to cater to emerging applications in electric vehicles, semiconductors, aerospace, and industrial manufacturing is a critical growth strategy. Firms are also pursuing strategic collaborations with system integrators, OEMs, and automation technology providers to create integrated manufacturing solutions. Increasing global manufacturing footprints and after-sales service networks allow companies to enhance accessibility and reliability for end users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Laser type trends

- 2.2.2 Power range trends

- 2.2.3 System configuration trends

- 2.2.4 Application trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 EV battery manufacturing demanding precision laser welding

- 3.2.1.2 Consumer electronics production demanding high-precision laser marking

- 3.2.1.3 Semiconductor miniaturization requiring ultrafast laser micromachining

- 3.2.1.4 Medical device manufacturing requiring micro-scale laser processing

- 3.2.1.5 Automated smart factories integrating laser processing equipment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Skilled operator shortage for complex laser machining processes

- 3.2.2.2 Maintenance complexity in high-power industrial laser sources

- 3.2.3 Market opportunities

- 3.2.3.1 Ultrafast lasers adoption in semiconductor wafer processing

- 3.2.3.2 Laser additive manufacturing expansion in aerospace components

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Laser Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fiber lasers

- 5.3 Co2 lasers

- 5.4 Solid-state lasers

- 5.5 Diode lasers

- 5.6 Ultrafast lasers

- 5.7 Excimer lasers

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Low power (<1 kW)

- 6.3 Medium power (1-6 kW)

- 6.4 High power (>6 kW)

Chapter 7 Market Estimates and Forecast, By System Configuration, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Standalone laser machines

- 7.3 Robotic laser processing systems

- 7.4 Integrated production line systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Cutting

- 8.3 Welding

- 8.4 Marking & engraving

- 8.5 Drilling

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Electronics manufacturing

- 9.4 Semiconductor fabrication

- 9.5 Aerospace & defense

- 9.6 Metal fabrication & industrial manufacturing

- 9.7 Medical devices

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 TRUMPF Group

- 11.1.2 IPG Photonics Corporation

- 11.1.3 Coherent Corp.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Lumentum Holdings Inc.

- 11.2.1.2 nLIGHT, Inc.

- 11.2.1.3 Amada Miyachi America, Inc.

- 11.2.1.4 MKS Instruments, Inc.

- 11.2.2 Asia Pacific

- 11.2.2.1 Han's Laser Technology Industry Group Co., Ltd.

- 11.2.2.2 Raycus Fiber Laser Technologies Co., Ltd.

- 11.2.2.3 Maxphotonics Co., Ltd.

- 11.2.2.4 Sahajanand Laser Technology Limited

- 11.2.3 Europe

- 11.2.3.1 Bystronic Laser AG

- 11.2.3.2 Jenoptik AG

- 11.2.3.3 LPKF Laser & Electronics AG

- 11.2.3.4 Toptica Photonics AG

- 11.2.1 North America

超快工业雷射市场:按应用、最终用户、雷射源类型、脉衝持续时间、波长和功率输出分類的全球预测,2026-2032年

超快工业雷射市场:按应用、最终用户、雷射源类型、脉衝持续时间、波长和功率输出分類的全球预测,2026-2032年 2026年全球工业雷射系统市场报告

2026年全球工业雷射系统市场报告 全球工业雷射市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034年)

全球工业雷射市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034年) 工业雷射系统市场规模、份额和成长分析(按雷射类型、功率范围、应用和地区划分)-2026-2033年产业预测工业雷射器市场(按雷射类型、功率、应用和最终用户产业)—2025-2032 年全球预测建筑雷射市场:按雷射类型、射程、应用、终端用户行业和销售管道- 全球预测(2025-2032年)

工业雷射系统市场规模、份额和成长分析(按雷射类型、功率范围、应用和地区划分)-2026-2033年产业预测工业雷射器市场(按雷射类型、功率、应用和最终用户产业)—2025-2032 年全球预测建筑雷射市场:按雷射类型、射程、应用、终端用户行业和销售管道- 全球预测(2025-2032年) 全球工业雷射系统市场

全球工业雷射系统市场 工业雷射系统市场报告(按类型、应用、最终用途行业和地区)2025 年至 2033 年

工业雷射系统市场报告(按类型、应用、最终用途行业和地区)2025 年至 2033 年 工业雷射器市场:全球2025-2029

工业雷射器市场:全球2025-2029 工业雷射系统市场 - 全球产业规模、份额、趋势、机会和预测,按类型、按功率输出、按最终用户产业、按地区和按竞争进行细分,2020-2030 年预测

工业雷射系统市场 - 全球产业规模、份额、趋势、机会和预测,按类型、按功率输出、按最终用户产业、按地区和按竞争进行细分,2020-2030 年预测