|

市场调查报告书

商品编码

1998848

纤维素纤维市场机会、成长要素、产业趋势分析及2026-2035年预测Cellulose Fiber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

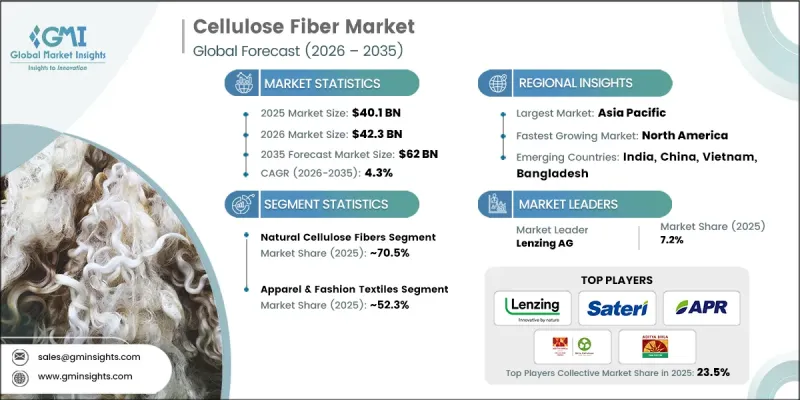

2025年全球纤维素纤维市场规模预估为401亿美元,预估至2035年将达620亿美元,年复合成长率为4.3%。

由于各行各业对永续和环保纺织解决方案的需求不断增长,市场正经历稳步增长。纤维素纤维,包括棉、麻、亚麻等天然纤维以及黏胶纤维、Lyocell纤维、莫代尔纤维等再生纤维,因其可生物降解性、舒适性和多功能性而备受关注。在时尚服饰业,消费者和製造商都越来越重视环保选项,从而推动了向永续材料和循环经济实践的转变。在服饰领域,纤维素纤维因其透气性、吸湿性和柔软质地而备受青睐,使其适用于从日常穿着到功能性服装的各种应用。再生纤维具有悬垂性、光泽度和染色性等更优异的性能,为合成纤维提供了永续的替代方案。除了服装业外,纤维素纤维还广泛用于家用纺织品、不织布和功能性纺织品,为床上用品、毛巾、家具面料、卫生用品和擦拭巾提供舒适性、耐用性、吸水性和可生物降解性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 401亿美元 |

| 预测金额 | 620亿美元 |

| 复合年增长率 | 4.3% |

预计到2025年,天然纤维素纤维市占率将达到70.5%,到2035年将以4.5%的复合年增长率成长。棉、麻、亚麻等植物来源纤维因其天然可生物降解性、舒适性和消费者熟悉度,继续主导市场。棉花仍然是领先的天然纤维,因其柔软性、透气性和在服装、家用纺织品和工业应用领域的多功能性而备受青睐。亚麻和亚麻纤维因其环境影响小、用水量和农药用量少以及耐用性高,再次受到关注,尤其适用于技术纺织品和永续时尚领域。

预计到2025年,服装和时尚纺织品市场份额将达到52.3%,并在2035年之前以4.2%的复合年增长率增长。该领域的主导地位归功于纤维素纤维的舒适性、透气性和美观性。虽然日常穿着主要依赖棉,但Lyocell纤维和莫代尔纤维等再生纤维因其优异的垂坠感、吸湿排汗性能和柔软触感,在高端时装、运动服和休閒正得到越来越广泛的应用。消费者对可生物降解和可再生纤维日益增长的偏好正在推动永续时尚的趋势。

预计到2025年,北美纤维素纤维市占率将达到16.7%。该地区的成长主要得益于消费者永续性意识的提高以及对天然可生物降解纤维的需求成长。在循环经济倡议、纺织品回收计划和供应链透明度的支持下,成熟的纺织、服装和室内装饰行业正积极采用永续纤维。此外,市场需求正进一步扩展至技术纺织品、不织布、医疗、汽车及特殊包装等领域,使市场范围超越传统纺织品。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依纺织品类型划分,2022-2035年

- 天然纤维素纤维

- 棉布

- 亚麻(亚麻布)

- 大麻(工业大麻)

- 黄麻

- 其他韧皮纤维和叶纤维(洋麻、苎麻、剑麻、蕉麻)

- 再生/人工纤维素纤维(MMCFs)

- 黏胶/人造丝

- Lyocell纤维

- 模态

- 醋酸纤维素

- 其他的

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 服装和时尚用纺织品

- 室内和家用纺织品

- 不织布

- 工业和技术用纺织品

- 汽车纺织品

- 包装材料

- 医疗保健

- 农业

- 其他的

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第八章:公司简介

- Sateri Holdings Limited

- Aditya Birla Group/Birla Cellulose

- Lenzing AG

- Thai Rayon Public Company

- 亚太人造丝(APR)

- Kelheim Fibres GmbH

- Eastman Chemical Company

- Asahi Kasei Corporation

- Cargill Cotton

- Olam Agri

- Bracell

- Tangshan Sanyou Group

- HempFlax Group BV

- The Flax Company

- Libeco NV

The Global Cellulose Fiber Market was valued at USD 40.1 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 62 billion by 2035.

The market is experiencing steady growth due to rising demand for sustainable and eco-friendly textile solutions across various industries. Cellulose fibers, including natural fibers such as cotton, hemp, and flax, as well as regenerated fibers like viscose, lyocell, and modal, are gaining traction for their biodegradability, comfort, and versatility. The fashion and apparel industry is increasingly shifting toward sustainable materials and circular economy practices, with both consumers and manufacturers prioritizing environmentally responsible options. In clothing, cellulose fibers are favored for their breathability, moisture absorption, and soft texture, suitable for everyday wear as well as performance garments. Regenerated fibers enhance properties like drape, luster, and dyeability, providing sustainable alternatives to synthetic textiles. Beyond apparel, cellulose fibers are widely used in home textiles, nonwovens, and technical textiles, offering comfort, durability, absorbency, and biodegradability across bedding, towels, upholstery, hygiene products, and wipes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.1 Billion |

| Forecast Value | $62 Billion |

| CAGR | 4.3% |

The natural cellulose fibers segment held 70.5% share in 2025 and is expected to grow at a CAGR of 4.5% by 2035. Plant-based fibers like cotton, hemp, and flax continue to dominate the market due to their natural biodegradability, comfort, and consumer familiarity. Cotton remains the primary natural fiber, appreciated for softness, breathability, and versatility across apparel, home textiles, and industrial applications. Hemp and flax are witnessing renewed interest due to their low environmental impact, minimal water and pesticide requirements, and high durability, making them suitable for technical textiles and sustainable fashion.

The apparel and fashion textiles segment accounted for 52.3% share in 2025 and is projected to grow at a CAGR of 4.2% through 2035. This segment dominates due to cellulose fibers' comfort, breathability, and aesthetic versatility. Everyday garments largely rely on cotton, while regenerated fibers such as lyocell and modal are increasingly adopted in premium fashion, activewear, and athleisure for superior drape, moisture management, and soft hand feel. Rising consumer preference for biodegradable, renewable fibers is boosting the sustainable fashion trend.

North America Cellulose Fiber Market held a 16.7% share in 2025. Growth in the region is driven by increased consumer awareness of sustainability and a shift toward natural, biodegradable fibers. Established textile, apparel, and home furnishing industries are actively incorporating sustainable fibers, supported by circular economy initiatives, textile recycling programs, and supply chain transparency. Demand is further expanding across technical textiles, nonwovens, medical, automotive, and specialty packaging applications, broadening the market beyond conventional textiles.

Leading companies in the Global Cellulose Fiber Market include Lenzing AG, Sateri Holdings Limited, Aditya Birla Group / Birla Cellulose, Thai Rayon Public Company, Asia Pacific Rayon (APR), Kelheim Fibres GmbH, Eastman Chemical Company, Asahi Kasei Corporation, Cargill Cotton, Olam Agri, Bracell, Tangshan Sanyou Group, HempFlax Group B.V., The Flax Company, and Libeco NV. Key strategies adopted by cellulose fiber companies to strengthen market presence include investing in sustainable fiber production, including organic cotton and low-impact hemp or flax. Firms are developing regenerated fibers with enhanced properties such as improved drape, luster, and dyeability to capture premium apparel and technical textile segments. Strategic partnerships with fashion brands, home textile manufacturers, and industrial users help expand distribution and adoption. Companies are also focusing on circular economy initiatives, recycling programs, and supply chain traceability to meet rising sustainability standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Fiber type

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fiber Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Natural cellulose fibers

- 5.2.1 Cotton

- 5.2.2 Flax (linen)

- 5.2.3 Hemp (industrial hemp)

- 5.2.4 Jute

- 5.2.5 Other bast & leaf fibers (kenaf, ramie, sisal, abaca)

- 5.3 Regenerated / man-made cellulose fibers (MMCFs)

- 5.3.1 Viscose / rayon

- 5.3.2 Lyocell

- 5.3.3 Modal

- 5.3.4 Cellulose acetate

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Apparel & fashion textiles

- 6.3 Home furnishings & household textiles

- 6.4 Nonwovens

- 6.5 Industrial & technical textiles

- 6.6 Automotive textiles

- 6.7 Packaging materials

- 6.8 Medical & healthcare

- 6.9 Agriculture

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Sateri Holdings Limited

- 8.2 Aditya Birla Group / Birla Cellulose

- 8.3 Lenzing AG

- 8.4 Thai Rayon Public Company

- 8.5 Asia Pacific Rayon (APR)

- 8.6 Kelheim Fibres GmbH

- 8.7 Eastman Chemical Company

- 8.8 Asahi Kasei Corporation

- 8.9 Cargill Cotton

- 8.10 Olam Agri

- 8.11 Bracell

- 8.12 Tangshan Sanyou Group

- 8.13 HempFlax Group B.V.

- 8.14 The Flax Company

- 8.15 Libeco NV

纤维素纤维市场:依纤维类型、形态、原料及应用划分-2026-2032年全球市场预测

纤维素纤维市场:依纤维类型、形态、原料及应用划分-2026-2032年全球市场预测 纤维素纤维市场规模、份额、趋势和预测:按纤维类型、应用和地区划分,2026-2034年

纤维素纤维市场规模、份额、趋势和预测:按纤维类型、应用和地区划分,2026-2034年 纤维素纤维市场分析及预测(至2035年):依类型、产品类型、应用、技术、成分、材料类型、製程、最终用户及功能划分醋酸纤维素纱线市场按产品类型、丹尼尔数、纤维长度和应用划分,全球预测,2026-2032年黏胶毛毡市场按产品类型、製造流程、厚度、应用、终端用户产业和通路划分-2026-2032年全球预测

纤维素纤维市场分析及预测(至2035年):依类型、产品类型、应用、技术、成分、材料类型、製程、最终用户及功能划分醋酸纤维素纱线市场按产品类型、丹尼尔数、纤维长度和应用划分,全球预测,2026-2032年黏胶毛毡市场按产品类型、製造流程、厚度、应用、终端用户产业和通路划分-2026-2032年全球预测 全球纤维素纤维市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的考量因素及预测(2026-2034)

全球纤维素纤维市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的考量因素及预测(2026-2034) 纤维素纤维市场规模、份额和成长分析(按类型、纤维类型、应用和地区划分)-2026-2033年产业预测

纤维素纤维市场规模、份额和成长分析(按类型、纤维类型、应用和地区划分)-2026-2033年产业预测 2034年全球人造纤维素纤维市场机会与策略

2034年全球人造纤维素纤维市场机会与策略 木棉纤维市场规模、份额和趋势分析报告:按应用、产品、地区和细分市场预测(2025-2033 年)

木棉纤维市场规模、份额和趋势分析报告:按应用、产品、地区和细分市场预测(2025-2033 年) 纤维素纤维市场(按产品、应用、国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

纤维素纤维市场(按产品、应用、国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测