|

市场调查报告书

商品编码

1998851

连接器市场商机、成长要素、产业趋势分析及 2026-2035 年预测。Connector Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

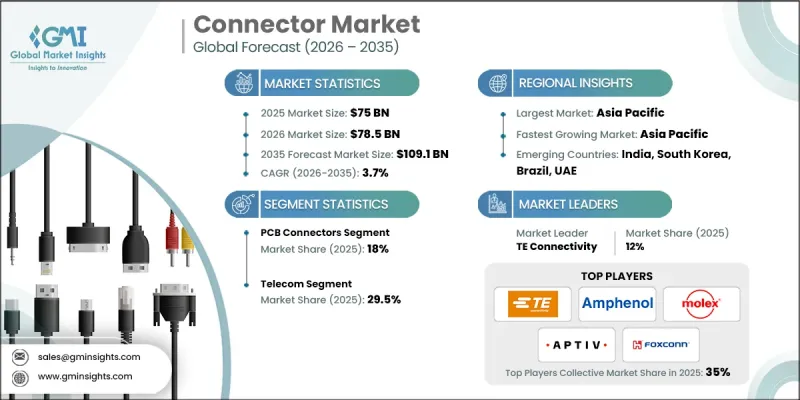

全球连接器市场预计到 2025 年将价值 750 亿美元,预计到 2035 年将以 3.7% 的复合年增长率增长至 1,091 亿美元。

该市场的发展动力源于监管机构为规范家用电子电器充电介面和统一快速扩张的电动车基础设施中的车辆-充电器连接所做的努力。监管机构优先考虑连接器的统一性,以减少废弃物、简化设备生态系统并简化原始设备製造商 (OEM) 的合规流程。标准化的插座定义了引脚配置、安全通讯协定和快速充电要求,重新定义了材料选择,并降低了多 SKU 生产的复杂性。在汽车领域,电气化正在推动对具有卓越抗振性和热稳定性的高功率连接器的需求。同时,介面标准的整合正在加速认证流程,实现充电网路的互通性,并促进售后市场的成长。此外,人工智慧在资料中心和高效能运算领域的日益普及,也推动了对高速基板对板连接器、夹层连接器、光纤连接器和电缆连接器的需求,这些连接器需要具有低插入损耗、严格的时延控制和减少串扰等特性,以应对高密度运算工作负载。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 750亿美元 |

| 预测金额 | 1091亿美元 |

| 复合年增长率 | 3.7% |

受多重通讯协定支援、增强网路安全和高频宽数位效能需求的推动,I/O连接器市场预计到2035年将以3.4%的复合年增长率成长。这些连接器对于需要高速、可靠资料传输和增强屏蔽能力的工业控制器、网路设备和运算系统至关重要。

预计到2025年,通讯领域将占据29.5%的市场份额,到2035年将以4.3%的复合年增长率成长。这一成长主要受频宽需求不断增长、高密度5G/5G Advanced部署、云端优先网路架构以及国际光纤基础设施扩张的推动。该产业的连接器必须支援超高速资料传输、低损耗光纤传输以及能够处理更高频宽的射频介面。人工智慧主导的网路现代化进一步推动了高密度光连接器、模组化互连和可扩展光纤平台的应用。

到2025年,美国连接器市场将占据78%的份额,市场规模将达到118亿美元。这个市场扩张主要受三大因素驱动:全国电动车充电基础设施的建设、测试和测量I/O系统的现代化以及支持人工智慧工作负载的超大规模云的增长。随着高密度资料中心的增加,市场对专为高密度机架和液冷架构设计的耐热基板级互连、光纤组件和电源连接器的需求日益增长。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监理情势

- 影响产业的因素

- 促进因素

- 汽车产业前景光明

- 不断扩张的通讯业

- 快速的都市化和对家用电子电器日益增长的需求

- 产业潜在风险与挑战

- 劣质产品的流通正成为一个严重的问题。

- 促进因素

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新机会和趋势

- 数位化和物联网集成

- 进入新兴市场

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 竞争性标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 市场规模及预测:依产品划分,2022-2035年

- PCB连接器

- I/O连接器

- 圆形连接器

- 光纤连接器

- 射频同轴连接器

- 其他的

第六章 市场规模与预测:依最终用途划分,2022-2035年

- 沟通

- 运输

- 车

- 电脑及周边设备

- 其他行业

第七章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 西班牙

- 英国

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- 3M

- Ametek

- Amphenol

- Aptiv

- AVX

- Fischer Connectors

- Foxconn

- GTK

- Hirose Electric

- Japan Aviation Electronics

- Lapp Group

- LOTES

- Luxshare Precision

- Mencom

- Molex

- Phoenix Contact

- Rosenberger

- Samtec Inc.

- TE Connectivity

- Yazaki

The Global Connector Market was valued at USD 75 billion in 2025 and is estimated to grow at a CAGR of 3.7% to reach USD 109.1 billion by 2035.

The market is driven by regulatory initiatives aimed at standardizing charging interfaces in consumer electronics and harmonizing vehicle-to-charger connections in rapidly expanding EV infrastructure. Regulators are emphasizing connector uniformity to reduce electronic waste, streamline device ecosystems, and simplify compliance for OEMs. Standardized receptacles define pin configurations, safety protocols, and fast-charging requirements, reshaping material choices and reducing the complexity of multi-SKU production. In the automotive sector, electrification is driving demand for high-power, vibration-resistant, and thermally stable connectors, while fewer interface standards accelerate certification, enable interoperable charging networks, and support aftermarket growth. Meanwhile, rising AI adoption in data centers and high-performance computing is increasing the need for high-speed board-to-board, mezzanine, optical, and cable connectors that offer lower insertion loss, tighter skew control, and reduced crosstalk for dense computational workloads.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $75 Billion |

| Forecast Value | $109.1 Billion |

| CAGR | 3.7% |

The I/O connector segment is expected to grow at a CAGR of 3.4% through 2035, fueled by the need for multi-protocol support, enhanced cybersecurity, and high-bandwidth digital performance. These connectors are essential for industrial controllers, networking equipment, and computing systems that demand fast, reliable data transfer with improved shielding.

The telecom segment accounted for 29.5% share in 2025 and is projected to grow at a CAGR of 4.3% by 2035. Growth is driven by rising bandwidth requirements, dense 5G/5G Advanced deployments, cloud-first network architectures, and expanding international fiber infrastructure. Connectors for this industry must support ultra-high-speed data, low-loss optical transmission, and RF interfaces capable of handling higher frequency bands. AI-driven network modernization further increases the adoption of high-density optical connectors, modular interconnects, and scalable fiber platforms.

U.S. Connector Market held a 78% share in 2025, generating USD 11.8 billion. Market expansion is fueled by three key factors: the nationwide build-out of EV charging infrastructure, modernization of test and measurement I/O systems, and hyperscale cloud growth to support AI workloads. High-density data centers are increasing demand for thermally tolerant board-level interconnects, fiber assemblies, and power connectors designed for dense racks and liquid cooling architectures.

Prominent players in the Global Connector Market include 3M, Ametek, Amphenol, Aptiv, AVX, Fischer Connectors, Foxconn, GTK, Hirose Electric, Japan Aviation Electronics, Lapp Group, LOTES, Luxshare Precision, Mencom, Molex, Phoenix Contact, Rosenberger, Samtec Inc., TE Connectivity, and Yazaki. Key strategies deployed by connector manufacturers include investing in R&D for high-speed, high-power, and thermally robust connectors; standardizing products for interoperability across multiple industries; forming strategic partnerships with EV, telecom, and data center OEMs; expanding global manufacturing and distribution networks; and offering integrated technical support and aftersales services. Companies also focus on sustainable material adoption, modular design solutions, and certification readiness to enhance market penetration, reduce customer switching barriers, and improve competitive positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 End use trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Positive outlook toward automobile industry

- 3.3.1.2 Expanding telecommunication industry

- 3.3.1.3 Rapid urbanization along with growing demand for consumer electronic devices

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High breach of low-quality products

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive benchmarking

- 4.4 Strategic dashboard

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million, Million Units)

- 5.1 Key trends

- 5.2 PCB connectors

- 5.3 IO connectors

- 5.4 Circular connectors

- 5.5 Fiber optic connectors

- 5.6 RF coaxial connectors

- 5.7 Others

Chapter 6 Market Size and Forecast, By End use, 2022 - 2035 (USD Million, Million Units)

- 6.1 Key trends

- 6.2 Telecom

- 6.3 Transportation

- 6.4 Automotive

- 6.5 Computer & peripherals

- 6.6 Other industries

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Million Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 UAE

- 7.5.2 Saudi Arabia

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 3M

- 8.2 Ametek

- 8.3 Amphenol

- 8.4 Aptiv

- 8.5 AVX

- 8.6 Fischer Connectors

- 8.7 Foxconn

- 8.8 GTK

- 8.9 Hirose Electric

- 8.10 Japan Aviation Electronics

- 8.11 Lapp Group

- 8.12 LOTES

- 8.13 Luxshare Precision

- 8.14 Mencom

- 8.15 Molex

- 8.16 Phoenix Contact

- 8.17 Rosenberger

- 8.18 Samtec Inc.

- 8.19 TE Connectivity

- 8.20 Yazaki

D-Sub微型连接器市场报告:趋势、预测和竞争分析(至2035年)铁路电源连接器市场报告:趋势、预测和竞争分析(至2035年)

D-Sub微型连接器市场报告:趋势、预测和竞争分析(至2035年)铁路电源连接器市场报告:趋势、预测和竞争分析(至2035年) 2026年全球空间连结器市场报告

2026年全球空间连结器市场报告 全球军用连接器市场规模、份额、趋势和成长分析报告(2026-2034年)

全球军用连接器市场规模、份额、趋势和成长分析报告(2026-2034年) 全球连接器市场(2026)

全球连接器市场(2026) 连接器市场:依产品、传输方式、材质、安装类型、最终用户和销售管道-2026-2032年全球预测FFC 和 FPC 连接器市场:按产品类型、触点数量、间距、安装方式、方向、应用和最终用户行业分類的全球预测 - 2026 年至 2032 年机架和麵板电源连接器市场:按触点数量、额定电流、端接方式、接点材料、安装方式、销售管道、最终用户行业划分,全球预测,2026-2032年商用载流布线装置市场:按装置类型、额定电压、额定电流、安装类型、相序配置、绝缘材料、导体材料、应用、最终用户行业划分-全球预测,2026-2032年

连接器市场:依产品、传输方式、材质、安装类型、最终用户和销售管道-2026-2032年全球预测FFC 和 FPC 连接器市场:按产品类型、触点数量、间距、安装方式、方向、应用和最终用户行业分類的全球预测 - 2026 年至 2032 年机架和麵板电源连接器市场:按触点数量、额定电流、端接方式、接点材料、安装方式、销售管道、最终用户行业划分,全球预测,2026-2032年商用载流布线装置市场:按装置类型、额定电压、额定电流、安装类型、相序配置、绝缘材料、导体材料、应用、最终用户行业划分-全球预测,2026-2032年 全球压入式销市场报告、绩效及预测(2021-2032年)

全球压入式销市场报告、绩效及预测(2021-2032年)