|

市场调查报告书

商品编码

2019047

音讯和视讯解决方案市场机会、成长要素、产业趋势分析及2026-2035年预测Audio Video Solution Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

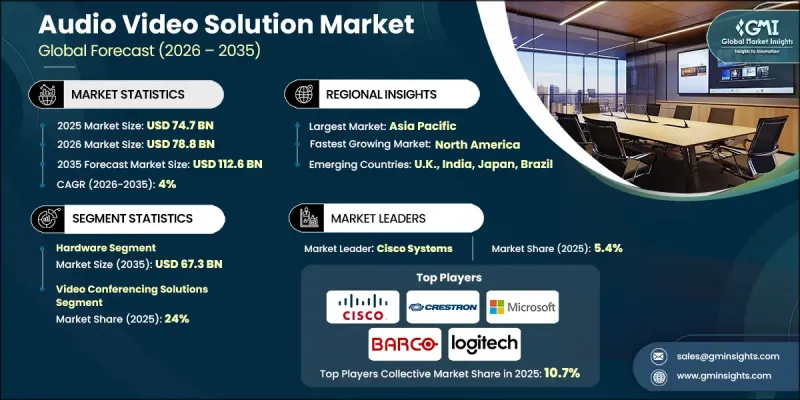

预计到 2025 年,全球音讯和视讯解决方案市场价值将达到 747 亿美元,并预计以 4% 的复合年增长率成长,到 2035 年达到 1126 亿美元。

随着组织和个人越来越依赖整合通讯技术来实现高效的沟通和内容传送,音讯视讯解决方案产业正经历着稳定成长。分散式环境中对无缝协作日益增长的需求,正在加速企业、教育和公共部门生态系统对整合通讯技术的采用。基于云端的通讯平台正在改变用户连接的方式,实现即时互动和跨不同环境的可扩展部署。政府主导的数位转型 (DX)倡议透过促进机构内部先进通讯基础设施的集成,进一步推动了整合通讯技术的普及。混合办公环境的广泛普及也推动了对支援虚拟协作和远端参与的灵活、扩充性的音讯视讯系统的需求。连接性、使用者介面设计和系统互通性的不断进步正在提升整体用户体验,而数位基础设施的持续投入也将继续巩固全球市场的长期成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 747亿美元 |

| 预测金额 | 1126亿美元 |

| 复合年增长率 | 4% |

预计到2025年,硬体领域市场规模将达到455亿美元,到2035年将达到673亿美元,持续维持其在影音解决方案市场的强劲地位。硬体组件对于确保影音系统的高品质效能和可靠性至关重要。负责采集、传输和显示音讯和影像内容的设备构成了这些解决方案的基础,支援跨多个环境的稳定通讯。该领域持续受益于设备技术的进步、耐用性的提升以及输出品质的增强。随着各组织机构将通讯和内容传送的可靠基础设施置于优先地位,专业环境中对高性能係统日益增长的需求正在推动该领域的进一步增长。硬体设计和整合能力的持续创新正在提升该领域在更广泛的音视频生态系统中的重要性。

预计到2025年,视讯会议解决方案市占率将达到24%,成为主要应用类别之一。随着企业越来越依赖数位通讯工具来连接不同地点的团队,该细分市场持续成长。随着混合办公和远距办公模式的日益普及,视讯会议已成为各行各业日常营运的重要组成部分。平台功能的增强,包括智慧功能的改进和易用性的提升,正在推动用户参与度和效率的提高。此外,随着企业将视讯通讯融入其营运架构,机构用户对视讯会议的采用率不断提高,也为此细分市场的发展提供了支持。平台的持续演进和使用者体验的不断提升,正在推动市场需求的持续成长,并巩固其市场主导地位。

预计到2025年,美国影音解决方案市占率将达到79.6%,展现出强大的区域领先地位。美国市场成长的主要驱动力是先进职场技术的快速普及和智慧通讯系统的广泛部署。各组织机构正投资建置现代化数位环境,以提升协作效率、生产力和营运效率。商业和公共部门数位基础设施的扩展进一步推动了对先进影音系统的需求。此外,对身临其境型使用者体验和内容传送解决方案的日益重视也促进了更高采用率的提升。凭藉强大的技术实力、持续的创新和投资,美国在整体市场发展中扮演着至关重要的角色。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 技术进步

- 消费者支出增加

- 可支配所得增加

- 产业潜在风险与挑战

- 激烈的竞争与市场饱和

- 消费者偏好的变化

- 机会

- 混合协作和智慧工作空间整合快速成长

- 拓展零售、饭店和公共空间的数位体验基础设施。

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 组件和创新趋势

- 当前技术趋势

- 新兴技术

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- 针对特定领域的生成式人工智慧应用案例和实施蓝图

- 风险、限制和监管考量

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL 分析

- 消费行为分析

- 购买模式

- 偏好分析

- 不同地区的消费行为差异

- 电子商务对购买决策的影响

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依组件划分,2022-2035年

- 硬体

- 显示器和投影仪

- 音响设备

- 影像设备

- 控制面板和介面

- 布线和连接基础设施

- 软体

- 控制和管理软体

- 基于IP的影音平台

- 协作软体

- 会议室预约软体

- 远端诊断和监控工具

- 服务

- 咨询和设计服务

- 安装和设定服务

- 培训和支援服务

- 託管服务和维护

- 系统升级和迁移服务

第六章 市场估算与预测:依解类型划分,2022-2035年

- 整合通讯与协作 (UC)

- 整合统一通讯平台

- 独立协作工具

- 视讯会议解决方案

- 会议室系统

- 个人视讯会议终端

- 混合会议解决方案

- 数位电子看板

- 室内数位电子看板

- 户外数位电子看板

- 互动数位电子看板

- 示范系统

- 投影类型系统

- 基于显示器的系统

- 无线演示解决方案

- 控制和自动化系统

- 集中控制平台

- 触控面板介面

- 会议室自动化解决方案

- 通报系统/紧急联繫

- 校园范围通知系统

- 楼宇紧急警报系统

- 综合危机管理平台

- 其他的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 公司

- 教育

- 政府/国防

- 卫生保健

- 零售和酒店

- 体育娱乐

- 运输

- 其他的

第八章 市场估算与预测:依最终使用者划分,2022-2035年

- 大公司

- 中小企业

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- Barco

- Biamp Systems

- Cisco Systems

- Crestron Electronics

- Extron Electronics

- Logitech

- Microsoft

- Panasonic

- Poly

- QSC Audio Products

- Samsung

- Shure Incorporated

- Sony Professional Solutions

- Zoom Video Communications

The Global Audio Video Solution Market was valued at USD 74.7 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 112.6 billion by 2035.

The audio video solutions industry is witnessing steady expansion as organizations and individuals increasingly rely on integrated communication technologies to enable efficient interaction and content delivery. The growing need for seamless collaboration across distributed environments is accelerating adoption across corporate, education, and public sector ecosystems. Cloud-based communication platforms are transforming how users connect, enabling real-time interaction and scalable deployment across various environments. Government-backed digital transformation initiatives are further supporting adoption by encouraging the integration of advanced communication infrastructure in institutional settings. The widespread shift toward hybrid work environments is also driving demand for flexible and scalable AV systems that support virtual collaboration and remote engagement. Continuous advancements in connectivity, user interface design, and system interoperability are enhancing overall user experience, while increasing investments in digital infrastructure continue to strengthen long-term market growth across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $74.7 Billion |

| Forecast Value | $112.6 Billion |

| CAGR | 4% |

The hardware segment generated USD 45.5 billion in 2025 and is expected to reach USD 67.3 billion by 2035, maintaining a strong position within the audio video solution market. Hardware components remain essential to ensuring high-quality performance and reliability across AV systems. Devices responsible for capturing, transmitting, and displaying audio and visual content form the backbone of these solutions, supporting consistent communication across multiple environments. The segment continues to benefit from advancements in device engineering, improved durability, and enhanced output quality. Increasing demand for high-performance systems in professional environments is further supporting growth, as organizations prioritize dependable infrastructure for communication and content delivery. Continuous innovation in hardware design and integration capabilities is reinforcing the segment's importance within the broader AV ecosystem.

The video conferencing solutions segment accounted for 24% share in 2025, making it the leading application category. This segment continues to expand as organizations increasingly depend on digital communication tools to connect teams across multiple locations. The growing adoption of hybrid and remote working models has made video conferencing an essential component of daily operations across industries. Enhanced platform capabilities, including intelligent features and improved usability, are driving higher engagement and efficiency. The segment is also supported by increasing institutional adoption, as organizations integrate video communication into their operational frameworks. Continuous platform evolution and improved user experience are contributing to sustained demand, reinforcing its dominant position within the market.

United States Audio Video Solution Market accounted for 79.6% share in 2025, demonstrating strong regional leadership. Market growth in the country is driven by the rapid adoption of advanced workplace technologies and increased deployment of intelligent communication systems. Organizations are investing in modern digital environments to improve collaboration, productivity, and operational efficiency. The expansion of digital infrastructure across commercial and institutional sectors is further accelerating demand for advanced AV systems. Additionally, increased focus on immersive user experiences and content delivery solutions is contributing to higher adoption rates. Strong technological capabilities, combined with continuous innovation and investment, position the United States as a key contributor to overall market development.

Key players operating in the Global Audio Video Solution Market include Cisco Systems, Microsoft, Google, Samsung, Sony Professional Solutions, Panasonic, Logitech, Zoom Video Communications, Barco, Crestron Electronics, Extron Electronics, Biamp Systems, Poly, QSC Audio Products, and Shure Incorporated. Companies in the Audio Video Solution Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. They are investing in advanced technologies to enhance system performance, improve integration capabilities, and deliver seamless user experiences. Organizations are focusing on developing scalable and flexible solutions that cater to evolving workplace and communication needs. Strategic partnerships and collaborations are being leveraged to expand product offerings and improve market reach. Companies are also emphasizing research and development to introduce next-generation solutions with improved efficiency and functionality. Additionally, efforts to enhance customer support services and optimize distribution channels are helping companies build long-term relationships and strengthen their market presence in an increasingly competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.3.1 Source consistency protocol

- 1.4 Research Trail & Confidence Scoring

- 1.4.1 Research Trail Components

- 1.4.2 Scoring Components

- 1.5 Data Collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.7 Paid sources

- 1.7.1 Sources, by region

- 1.8 Base estimates and calculations

- 1.8.1 Base year calculation for any one approach

- 1.9 Forecast model

- 1.9.1 Quantified market impact analysis

- 1.9.1.1 Mathematical impact of growth parameters on forecast

- 1.9.1 Quantified market impact analysis

- 1.10 Research transparency addendum

- 1.10.1 Source attribution framework

- 1.10.2 Quality assurance metrics

- 1.10.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Solution Type

- 2.2.4 Application

- 2.2.5 End User

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Increasing consumer spendings

- 3.2.1.3 Rising disposable income

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competition and market saturation

- 3.2.2.2 Changing consumer preferences

- 3.2.3 Opportunities

- 3.2.3.1 Rapid growth of hybrid collaboration & smart workspace integrations

- 3.2.3.2 Expansion of digital experience infrastructure across retail, hospitality & public spaces

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Component and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Impact of AI & generative AI on the market

- 3.6.1 AI-driven disruption of existing business models

- 3.6.2 Gen AI use cases & adoption roadmap by segment

- 3.6.3 Risks, limitations & regulatory considerations

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behaviour analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behaviour

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Component, 2022-2035 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Displays & projectors

- 5.2.2 Audio equipment

- 5.2.3 Video equipment

- 5.2.4 Control panels & interfaces

- 5.2.5 Cabling & connectivity infrastructure

- 5.3 Software

- 5.3.1 Control & management software

- 5.3.2 AV-over-IP platforms

- 5.3.3 Collaboration software

- 5.3.4 Room scheduling & booking software

- 5.3.5 Remote diagnostics & monitoring tools

- 5.4 Services

- 5.4.1 Consulting & design services

- 5.4.2 Installation & deployment services

- 5.4.3 Training & support services

- 5.4.4 Managed services & maintenance

- 5.4.5 System upgrade & migration services

Chapter 6 Market Estimates & Forecast, By Solution Type, 2022-2035 (USD Billion)

- 6.1 Key trends

- 6.2 Unified communications & collaboration (uc)

- 6.2.1 Integrated uc platforms

- 6.2.2 Standalone collaboration tools

- 6.3 Video conferencing solutions

- 6.3.1 Room-based systems

- 6.3.2 Personal video conferencing devices

- 6.3.3 Hybrid meeting solutions

- 6.4 Digital signage

- 6.4.1 Indoor digital signage

- 6.4.2 Outdoor digital signage

- 6.4.3 Interactive digital signage

- 6.5 Presentation systems

- 6.5.1 Projection-based systems

- 6.5.2 Display-based systems

- 6.5.3 Wireless presentation solutions

- 6.6 Control & automation systems

- 6.6.1 Centralized control platforms

- 6.6.2 Touch panel interfaces

- 6.6.3 Room automation solutions

- 6.7 Mass notification & emergency communication

- 6.7.1 Campus-wide notification systems

- 6.7.2 Building emergency alert systems

- 6.7.3 Integrated crisis management platforms

- 6.8 Other

Chapter 7 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion)

- 7.1 Key trends

- 7.2 Corporate

- 7.3 Education

- 7.4 Government & Defense

- 7.5 Healthcare

- 7.6 Retail & Hospitality

- 7.7 Sports & Entertainment

- 7.8 Transportation

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion)

- 8.1 Key trends

- 8.2 Large Enterprises

- 8.3 Small & Medium Businesses (SMBs)

Chapter 9 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Barco

- 10.2 Biamp Systems

- 10.3 Cisco Systems

- 10.4 Crestron Electronics

- 10.5 Extron Electronics

- 10.6 Google

- 10.7 Logitech

- 10.8 Microsoft

- 10.9 Panasonic

- 10.10 Poly

- 10.11 QSC Audio Products

- 10.12 Samsung

- 10.13 Shure Incorporated

- 10.14 Sony Professional Solutions

- 10.15 Zoom Video Communications

音讯设备市场:按产品类型、技术、价格范围、分销管道和最终用户划分 - 全球市场预测(2026-2032 年)

音讯设备市场:按产品类型、技术、价格范围、分销管道和最终用户划分 - 全球市场预测(2026-2032 年) 数位媒体适配器 (DMA) 市场报告:按类型、内容、分发管道、应用和地区划分 (2026–2034)声学寻呼设备市场:全球市场按产品类型、技术、应用、销售管道和最终用户分類的预测——2026-2032年音频频率变压器市场:2026-2032年全球市场预测(以相数、铁芯类型、额定功率、绕组材料、冷却方式、最终用户和销售管道)

数位媒体适配器 (DMA) 市场报告:按类型、内容、分发管道、应用和地区划分 (2026–2034)声学寻呼设备市场:全球市场按产品类型、技术、应用、销售管道和最终用户分類的预测——2026-2032年音频频率变压器市场:2026-2032年全球市场预测(以相数、铁芯类型、额定功率、绕组材料、冷却方式、最终用户和销售管道) 重低音市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、设备、最终用户及安装类型划分音讯混音主机市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、功能、安装类型及解决方案划分录音室混音主机市场:2026-2032年全球预测(依主机类型、主机尺寸、技术、应用程式、最终用户和通路划分)磁性拾取器市场(按拾取器类型、磁铁类型、驱动类型、应用和销售管道),全球预测,2026-2032年紧凑型混音主机市场按产品类型、分销管道和最终用户划分 - 全球预测 2026-2032

重低音市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、设备、最终用户及安装类型划分音讯混音主机市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、功能、安装类型及解决方案划分录音室混音主机市场:2026-2032年全球预测(依主机类型、主机尺寸、技术、应用程式、最终用户和通路划分)磁性拾取器市场(按拾取器类型、磁铁类型、驱动类型、应用和销售管道),全球预测,2026-2032年紧凑型混音主机市场按产品类型、分销管道和最终用户划分 - 全球预测 2026-2032 混音器市场 - 全球产业规模、份额、趋势、机会和预测(按类型、应用、规模、地区和竞争格局划分,2020-2030 年预测)

混音器市场 - 全球产业规模、份额、趋势、机会和预测(按类型、应用、规模、地区和竞争格局划分,2020-2030 年预测)